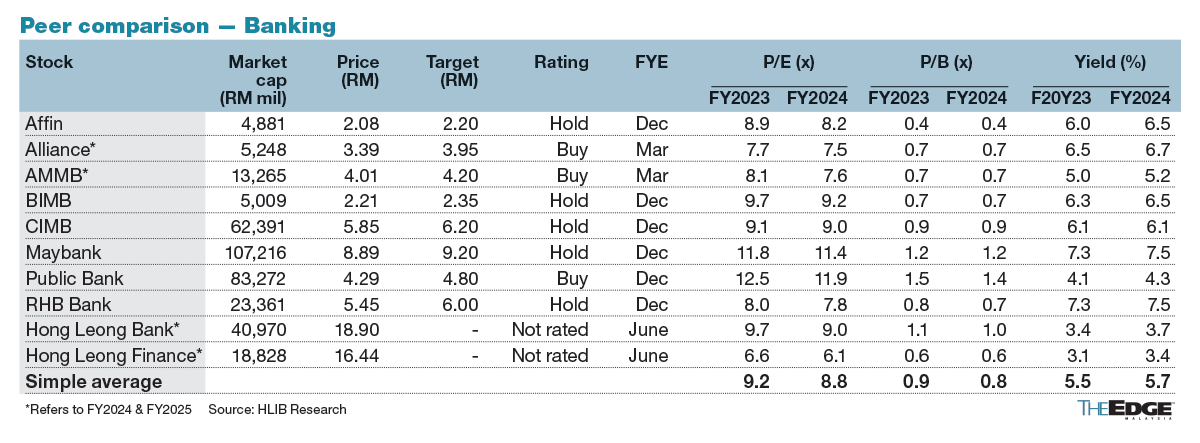

Public Bank is endorsed by Hong Leong Investment Bank due to its defensive qualities and multi-year low in foreign shareholding.

KUALA LUMPUR (Jan 2): Investment analysts have shared mixed views on the Malaysian banking sector's valuations and outlook, while naming Public Bank Bhd, CIMB Group Holdings Bhd, AMMB Holdings Bhd and Alliance Bank Malaysia Bhd as their top picks.

Hong Leong Investment Bank (HLIB) Bhd expects the banking sector profit to grow at a slower rate of 5%/4% in FY2024/FY2025 compared to estimates of 14% in FY2023, no thanks to the limited recovery in the net interest margin (NIM), a slowdown in non-interest income growth, and the absence of non-credit cost (NCC) write-backs.

This puts the sector at a relative lag behind the broader market, where the FBM KLCI is anticipated to surge by a swifter 8% throughout the year.

At Tuesday’s closing bell, the Bursa Malaysia Financial Services Index was 16.31 points or 0.10% lower at 16,286.73. The FBM KLCI, meanwhile, slipped 0.11% or 1.56 points to 1,453.10.

“In our view, the risk-reward now is more balanced as there are no new positive catalysts to spur share prices significantly higher,” said the research house, which maintained its ‘neutral’ rating for the sector.

“Valuations are not excessive and hence, we feel it is too premature to turn full-on bearish,” it said in a note on Tuesday.

HLIB named Public Bank Bhd, AMMB Holdings Bhd and Alliance Bank Malaysia Bhd as its top picks, all receiving "buy" recommendations and target prices (TPs) of RM4.80, RM4.20, and RM3.95, respectively.

Public Bank is endorsed by HLIB due to its defensive qualities and multi-year low in foreign shareholding. It favoured AMMB for its dividend payout bandwidth in the near future and Alliance Bank due to its inexpensive valuation.

In contrast, MIDF Investment Bank Bhd said valuations in the sector remain attractive and it advises investors to be more selective in their choices as not all banks have optimal outlooks.

The research house reiterated its "positive" call for the banking sector due to strong valuations and dividend outlook. “We feel that upside rerating drivers should provide a boost to sector valuations, especially since the worst seems over for now”.

“Further asset quality and NCC improvement expected — with high writeback possibility. Post-CNY [Chinese New Year] FD [fixed deposit] rate testing by banks — there is a possibility for further normalisation in rates, and subsequently upside to NIMs [and] Industry dividend outlook is still excellent,” said MIDF which favoured CIMB Group Holdings Bhd (buy, TP: RM6.62) and AMMB (buy,TP: RM4.23).

Meanwhile, Kenanga Investment Bank Bhd expressed a more bullish stance on the sector, by maintaining its “overweight" rating as the research house expects loan growth of 4.5-5% in CY2024, slightly higher than its CY2023 assumption of 4-4.5%, premised upon a greener economic landscape.

It said the banking sector’s resilience will continue to be relevant to investors, especially with more prominent recessionary concerns seen in key regional markets.

“Domestically, we see asset quality controls to remain tight, governed by BNM’s [Bank Negara Malaysia] strict requirements and prudent management by the banks which most still maintain some level of management overlays. Meanwhile, liquidity is expected to be sufficient as the focus on building their respective loans book and deposits book appear to be equal,” said Kenanga which kept its "overweight" rating.

“At current price points, banking dividend yields still lead with 6-7% possibly being offered. For top picks, we opted to focus on high growth merit names which could see both near-term and long-term interest for investors, being CIMB, AMMB and Alliance Bank,” it added.

Shares of Public Bank dropped one sen or 0.23% to RM4.28, giving it a market capitalisation of RM83.08 billion. CIMB was down one sen or 0.17% to RM5.84, valuing the group at RM62.28 billion.

AMMB rose 0.50% or two sen to RM4.03, with a market value of RM13.36 billion, while Alliance Bank slipped 0.59% or two sen to RM3.37, translating into a market capitalisation of RM5.22 billion.

- Tariff shock awaits China after trade surplus hits US$103 bil

- Malaysian semiconductor stocks fall amid US probes, software firms steady

- HRD Corp's chief executive Shahul Hameed steps down, confirming The Edge report

- Maybank customers can now make QR payments through MAE app in Cambodia

- Autopart distributor MSB Global slips 15% on ACE Market debut

- Farewell, Pak Lah

- Malaysia to bear brunt of weaker exports to US, Macquarie flags

- Malaysia can still navigate tariff shocks with investment momentum — Amro

- My Say: PGU still key to powering industrial growth despite gas explosion at Putra Heights

- Xi’s visit may unlock new investment opportunities beyond trade, says CGS International