Wong : We remain constructive on the outlook for gold amid ongoing global trade friction and uncertainty

This article first appeared in Capital, The Edge Malaysia Weekly on April 7, 2025 - April 13, 2025

SAFE-haven investments are expected to stoke demand for gold and extend its run amid trade tensions, a weaker US dollar, increasing central bank purchases and a renewed emphasis on ballooning US debt, experts say.

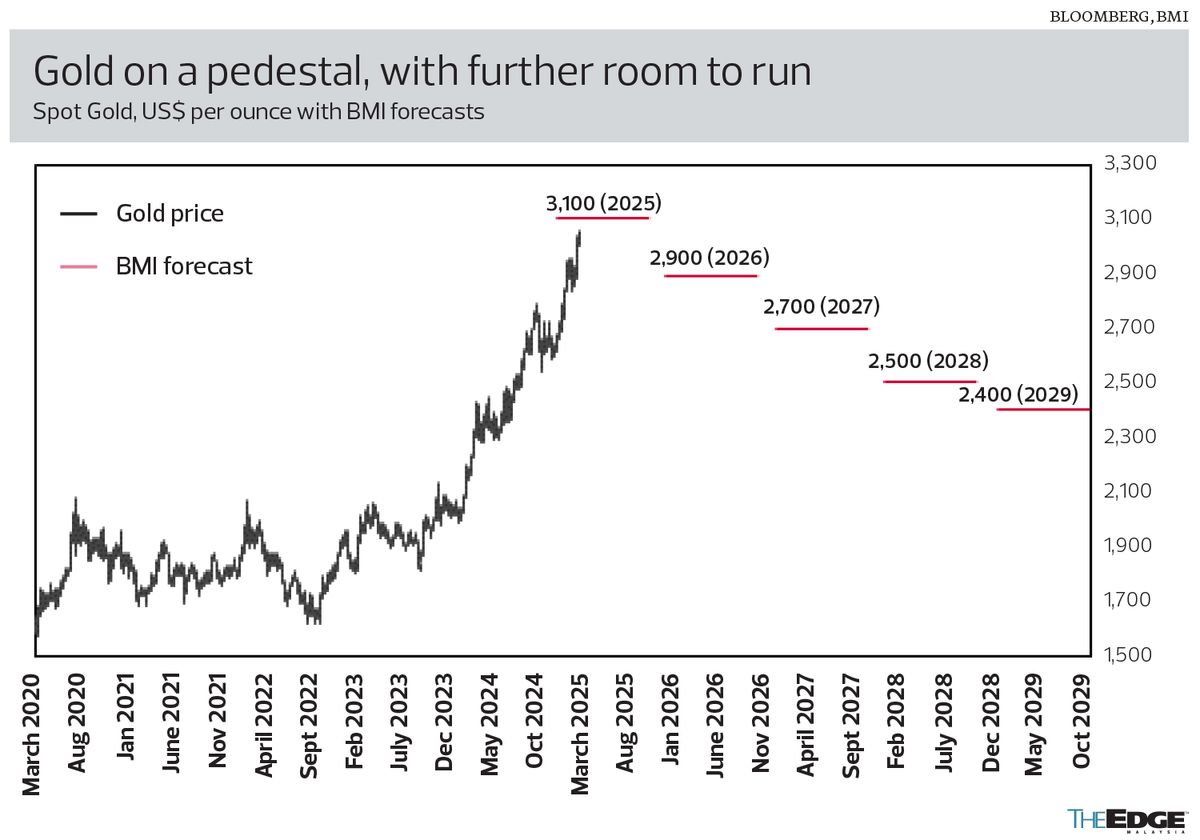

Gold prices have risen more than 50% since January 2024.

However, some fund managers and experts in the precious metal think that the current rally may lose some momentum as investors’ risk appetite increases in the longer term. Gold prices are expected to remain above pre-Covid-19 levels of US$1,393 per ounce.

The price of gold breached the US$3,000 an ounce mark in mid-March and hit a new record of US$3,134.70 on April 2, according to Bloomberg data. That day, US President Donald Trump announced reciprocal tariffs. Spot gold stood at the US$3,087 level last Thursday.

Trump slapped a 10% tariff on most goods imported into the US, and higher duties on dozens of countries, including Malaysia. He also confirmed a 25% tariff on auto imports, which will come into force on April 3. The reciprocal tariffs do not apply to certain goods such as bullion and gold.

Global shares and US futures tumbled in the aftermath of the reciprocal tariff announcement as US recession fears spooked markets. In Malaysia, the FBM KLCI fell 7.61 points to close at 1,518.91, dragged down by technology stocks. Vietnam’s benchmark stock index sank 6.68% to an over two-month low of 1,229.84 points as the dong hit a record low. Nasdaq futures skidded over 3%, with the S&P 500, FTSE and European futures also sliding. Brent crude declined by 6% to US$70.46 a barrel at the time of writing.

“We have upgraded our gold forecast, expecting US$3,160 by end-2025 and US$3,250 by end-2026. Gold’s appeal as a safe haven and inflation hedge has further strengthened in light of geopolitical concerns and tariff uncertainty,” OCBC FX strategist Christopher Wong tells The Edge.

“We remain constructive on the outlook for gold amid ongoing global trade friction and uncertainty.”

Wong says softer US data, such as retail sales and the Producer Price Index, suggests that the US Federal Reserve’s interest rate cut cycle has yet to conclude. OCBC FX predicts the Fed will cut rates three times this year.

This, along with other central banks’ easing monetary policies, is contributing to higher gold prices.

Additionally, factors such as central bank purchases (including China’s), and ongoing geopolitical concerns that include the Russia-Ukraine and Israel-Palestine conflicts, are also driving up gold prices.

UBS AG Global Wealth Management chief investment officer Mark Haefele says in an April 3 report that gold will continue to serve as a hedge against geopolitical and inflation risks. “We target US$3,200 an ounce by year end in our base case but note that the metal could trade even higher in the event of tariffs staying in place longer than expected.”

Similarly, BMI, a unit of Fitch Solutions, revised upwards its annual average gold price forecast for 2025 to US$3,100 per ounce, as it forecasts gold will outperform again within the wider metals complex, a scenario that “would be put in limbo only if the Fed proceeds to raise interest rates instead”.

“In the longer term, beyond 2025, we expect gold prices to ease. The main driver of easing gold prices in the longer term will be greater risk-on sentiment as the global economy recovers in the later part of the decade. Despite our outlook for gold prices to weaken, we do not see a return to pre-Covid levels. Gold prices will average US$2,720 per ounce during 2025 to 2029, compared with US$1,393 per ounce in 2019,” BMI says.

“There is likely to be a period of negotiations and retaliatory responses going on at the same time between tariffed countries and the US. So it may take a while before we see the final tariff outcome. But in the interim, we should continue to see divergent US dollar at play: with US dollar weaker versus G3 majors (euro, yen and pound sterling) but the US dollar maintaining a bid tone vs Asia ex-Japan FX. Safe-haven proxies such as gold, yen and Swiss francs continue to stay supported,” Wong says.

Central bank demand, ballooning debt in US

According to the World Gold Council (WGC), central banks reported 18 trillion tonnes of net purchases in January, with emerging market central banks remaining at the forefront of net buying.

Uzbekistan, China and Kazakhstan were the top three buyers with gold holdings totalling 391 trillion tonnes, or 82% of its total reserves, 2,285 trillion tonnes or 6% of total reserves, and 288 trillion tonnes or 55% of total reserves, respectively, at the end of January.

Poland and India have also been accumulating gold reserves this year, adding three trillion tonnes to their respective reserves in January, the council noted.

Notably, net inflows to gold exchange-traded funds (ETFs) in India reached a record INR37.5 billion in January and INR19.8 billion as bullion peaked while local equities fell, according to the Association of Mutual Funds in India.

Although India’s gold ETF holdings are just 2% of the global total, the country is the world’s second largest investor in the commodity after China, according to the WGC.

In its 2024 Gold Demand Trends report, the council notes that central banks continue to play a pivotal role in global gold demand, with their purchasing patterns influenced by both economic and geopolitical shifts. “The shift from armed conflict to broader economic tensions has reinforced their net buying trend, especially apparent since 2022. Many central banks appear to have strategically leveraged temporary price pullbacks as buying opportunities, while sales have remained limited and largely tactical during price rallies.”

Meanwhile, OCBC’s Wong draws attention to the fact that US national debt is at more than US$36 trillion (RM160 trillion), and overnight, the Congressional Budget Office released its long-term budget outlook, highlighting that US debt will rise to 156% of gross domestic product in 30 years, from 100% of GDP.

“Interest as a share of GDP will also increase to 5.4%, from a record 3.2% this year. CBO also projects that the trust fund for Social Security retirement benefits will be exhausted in 2033 and the theoretically combined Social Security retirement and disability insurance trust fund will be exhausted in 2034.”

Against this backdrop, tariff uncertainties have continued to stoke growth and inflation concerns, stepping up demand for gold, the safe-haven proxy.

Ray Dalio, founder of the world’s biggest hedge fund firm Bridgewater Associates, reportedly said “a prudent amount of gold making up 10% to 15% of investment portfolios” can help as a diversification measure for portfolios in the current economic environment.

Dalio warned about the economic dangers that come with soaring US debt and he told US lawmakers that the budget deficit needs to be brought down to about 3% of GDP, from a projected level of 7.2%.

“More importantly, US protectionism measures may continue to see structural changes in the geoeconomic landscape amid shifting global supply chains while national security concerns are shaping economic policies and redefining rules. These big shifts or transition to a new world order will see heightened uncertainties. Gold may still offer a safe harbour in times of uncertainty,” OCBC’s Wong says.

He adds that US protectionism measures, fading US exceptionalism and ballooning US debt are some catalysts that may challenge the US dollar’s status as a reserve currency. Reserve diversification may also add to gold strength over time, he predicts.

US dollar in limbo

Meanwhile, the US dollar slid broadly last Thursday, with the US Dollar Index, which gauges the greenback’s value against six major currencies, nosediving to near 102.00, the lowest level seen in almost six months.

OCBC’s Wong says further ballooning in US debt should intensify the de-dollarisation narrative, adding to demand for gold.

He predicts a mixed outlook for the US dollar.

Wong says the US dollar is expected to rise slightly against Asian currencies (excluding Japan) due to risks from Trump’s tariffs on China and global growth concerns. However, the US dollar may weaken against major currencies such as the euro, pound and yen. In Europe, increased defence spending could boost growth, while in China, advances in artificial intelligence and technology are helping to stabilise the economy.

Wong notes that if global growth outpaces the US, the greenback may weaken overall.

UBS’ Haefele believes investors can benefit from currency volatility by trading the range in euro/USD, USD/Swiss franc and pound/USD.

“In isolation, tariffs are dollar-positive, and the US dollar has also traditionally rallied during risk-off periods. However, we believe this effect is likely to be offset by potentially sharper downgrades to US growth and rate expectations than in other regions, as well potential increases in diversification flows away from dollar assets because of the political uncertainty.

“We note that longer-term weakness in the US dollar could arise if downside risks to the growth outlook are accompanied by sharper-than-expected Fed rate cuts,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia’s richest just got wealthier thanks to stronger ringgit — Forbes

- TRX to begin construction of new office tower with PwC Malaysia as anchor tenant, says CEO

- Syed Saddiq trial: Mere receipts insufficient to show funds were young MP's personal monies

- Malaysia Aviation Group posts RM54m earnings for FY2024, its second straight annual profit

- Malaysia delays LNG shipments due to outage at export plant, Bloomberg reports

- DBS CEO tells businesses to 'buckle up' for tariff uncertainty

- Moldovan parliament votes to hold elections on Sept 28

- Worldpay’s US$24.3b sale breaks Wall Street’s M&A logjam

- Mission to set up field hospital in Myanmar put on hold, says Mohamad Hasan

- Sin Chew editors detained over Jalur Gemilang gaffe, says IGP