This article first appeared in The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

But this is not just your grandfather’s cyclical economic uncertainty Trump has triggered. This is the uncertainty that cuts to the bone, the uncertainty that comes from seeing a world you knew for 80 years being unravelled by the most powerful player — who doesn’t know what he is doing and is surrounded by bobbleheads.

The world has enjoyed an extraordinary period of economic growth and absence of great-power wars since 1945. Of course, it was not perfect, and there have been many troubled years and countries that lagged. But in the broad sweep of world history, these 80 years have been remarkably peaceful and prosperous for a lot of people, in a lot of places.

And the No 1 reason that the world was the way it was, was because America was the way it was.

That America was summed up by two lines in John F Kennedy’s Inaugural Address on Jan 20, 1961: ‘Let every nation know, whether it wishes us well or ill, that we shall pay any price, bear any burden, meet any hardship, support any friend, oppose any foe to assure the survival and the success of liberty.’

I would call Trump’s foreign policy philosophy not ‘containment’ or ‘engagement’, but ‘smash and grab’. Trump aspires to be a geopolitical shoplifter. He wants to stuff his pockets with Greenland, Panama, Canada and the Gaza Strip — just grab them off the shelves, without paying — and then run back to his American safe house. Our post-war allies have never seen this America before.

If Trump wants to take America on a 180-degree turn, he owes it to the country to have a coherent plan, based on sound economics and a team that represents the best and the brightest, not the most sycophantic and right-wing woke. And he owes us an explanation of exactly how purging professional staff from key bureaucracies that keep the nation running from administration to administration, whether at the Justice Department or the IRS, and appointing fringe ideologues to key positions is good for the country and not just him.”

The above excerpt is from an opinion piece by Thomas L Friedman, titled “A Great Unraveling is Underway”, in The New York Times of March 11, 2025.

Thomas Loren Friedman is an American political commentator and a three-time Pulitzer Prize winner who writes a weekly column for the US daily newspaper. He has also authored many books, including The World is Flat: A Brief History of the Twenty-first Century.

We think he has brilliantly articulated US President Donald Trump and his policies and intentions (perhaps not the why), and the impact it will have on both the US and the world — reflecting the views of most people. We have also quoted the above because it is an excellent introduction to this article, our Part 2

on Trumpianomics. We think Friedman is both right and wrong, and why we think so will become apparent as you read on.

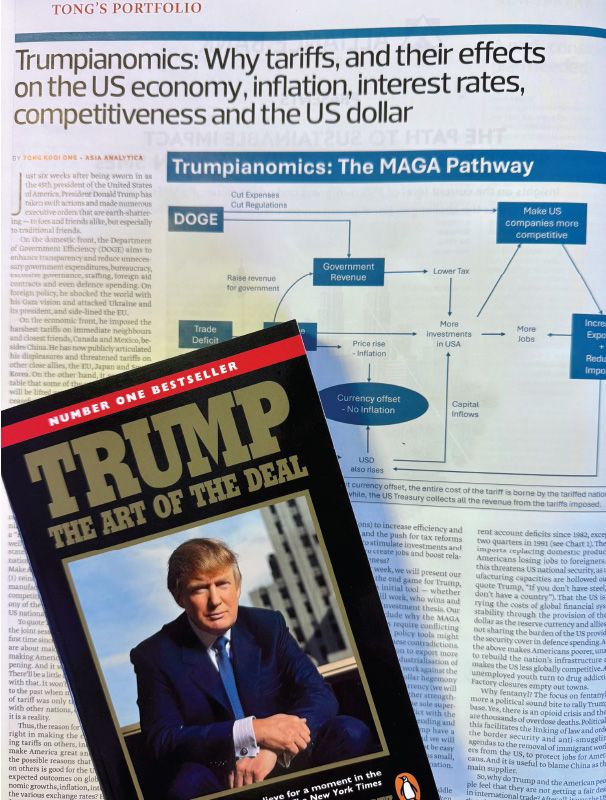

Last week, we argued that contrary to others (including Friedman), we believe that the apparent disparate actions on the domestic, foreign and economic fronts by Trump are in fact a well-conceived, connected and comprehensive plan to fulfil his “Make America Great Again” (MAGA) objectives. We described it as “The MAGA Pathway”. We even drew a flow diagram for ease of understanding (scan the QR code to re-read the article).

What is President Trump’s endgame?

In a nutshell, continued supremacy of the US in a unipolar world for a long time to come. This requires the US to protect its national security interests, the ability to project its military and financial powers, reshaping its defence shield and redefining its allies and foes, to reverse and recreate a new global trade and economic order — one that the US can dictate terms to and for the benefit of the US.

To protect its national security interests and the livelihoods of Americans, it must reindustrialise and revitalise the manufacturing sector (including onshoring and expanding its domestic supply chain), and rebuild its crumbling infrastructure. It must increase its relative competitiveness to export more and import less. This requires higher domestic and foreign investments into the US; more research and development; more innovation; and a better and more competitive education system, especially in the critical areas of AI, data analytics and computing.

Reducing inflation is also critical, via supply-side deregulation, cutting the red tape and bureaucracy, excessive regulatory oversight and lower energy prices. That includes de-emphasising diversity, equality and inclusivity — “better to be unequal but richer” — creating jobs and increasing wages. Critically, the US must improve its trade balance, move aggregate demand from other countries to the US, increase the share of the US in global trade and its share of the global wealth.

To maintain its military supremacy, especially in the ability to project its might and capabilities everywhere, to provide a defence shield to its allies, the US wants others to help pay for it (cost-sharing). This defence burden becomes increasingly unbearable as the share of US to the global economy shrinks. Trump believes its allies have taken advantage of the US, and it is time for friends and allies to pay up.

The hegemony of the mighty US dollar, as the world’s only reserve currency, is equally important for Trump. Why? As the only reserve currency, it enjoys price inelasticity of demand. In layman’s terms, the US can borrow more without incurring higher interest costs. As the sole reserve currency, the US can also secure its national security goals without going into a physical war by exerting control over trade and financial transactions, freezing assets, cutting banks off SWIFT, and cutting access to the US banking and financial system that is necessary for global businesses (yes, US dollar weaponisation).

But as the reserve currency, it faces the Triffin Dilemma as we described in Part 1. The overvalued US dollar makes US-produced goods uncompetitive in exports and domestically, leading to import substitution — creating a twin deficit (current and fiscal account) that is not sustainable for the US. Eventually, there is a tipping point where the US dollar runs into credit risk, threatening the US dollar itself as the reserve currency. And before that, imports replacing locally-produced goods means business closure and jobs lost for Americans. In other words, this financial power has a cost, less export competitive due to an overvalued currency.

Given these dilemmas or paradoxes, how then can Trump achieve his ultimate MAGA goals? According to Triffin World, owning the reserve currency, which gives a nation supremacy over trade and finance, eventually leads to a collapse of that reserve currency. Having military supremacy at excessive cost leads to reduced resources to invest and strengthen the nation’s economic competitiveness, which results in its shrinking share of global gross domestic product or GDP. Eventually, the burden becomes unbearable.

The next section explores how Trump might be attempting to overcome these paradoxes — by linking up what has been articulated by those perceived to reflect his views, including Scott Bessent (Treasury Secretary) and Stephen Miran (chair of the Council of Economic Advisers).

How countries will be forced to share the exorbitant burden of US supremacy

The excerpt below is taken from remarks made by Bessent on March 6, 2025 at the Economic Club of New York. He has made similar articulations even before his confirmation as the US Treasury Secretary.

“The international trading system consists of a web of relationships — military, economic, political. One cannot take a single aspect in isolation. This is how President Trump sees the world, not as a zero-sum game, but as inter-linkages that can be reordered to advance the interest of the American people.

This is contrary to the last several decades, when other countries acted to advance their own interest, while our policymakers largely forgot about the trade-offs of unconstrained trade misalignment. The result was the United States provided a source of massive demand, acted as arbiter of global peace, but did not receive adequate compensation. For example, today the United States finds itself subsidising the rest of the world’s under-spending in defence.

This is not just a security issue. The United States also provides reserve assets, serves as a consumer of first and last resort, and absorbs excess supply in the face of insufficient demand in other countries’ domestic models. This system is not sustainable.

Access to cheap goods is not the essence of the American Dream. The American Dream is rooted in the concept that any citizen can achieve prosperity, upward mobility, and economic security. For too long, the designers of multilateral trade deals have lost sight of this. International economic relations that do not work for the American people must be re-examined.

This is what tariffs are designed to address — levelling the playing field such that the international trading system begins to reward ingenuity, security, rule of law and stability; not wage suppression, currency manipulation, intellectual property theft, non-tariff barriers and draconian regulations. To the extent that another country’s practices harm our own economy and people the United States will respond. This is the America First Trade Policy.

These are not the only metrics in which our global trading partners should be scored. That is increased burden sharing on security is critical amongst friendly nations. No longer should American tax dollars, American military equipment, and in some cases, American lives, be the sole bearers of upholding friendly trade and mutual security. Burden sharing is not a matter of offloading risk, but a matter of all benefiting parties having interest in the system. The shared interest ultimately strengthens the international system as the cost of disruption outweigh any benefits of dissolution.

… economic security is national security. … President Trump expressed his view that overuse sanctions could affect the US dollar’s supremacy. … not unlike the overuse of antibiotics, the target becomes immune and mutates.”

We quoted extensively because the articulation is self-explanatory. They are consistent with the public outburst of Trump that other nations (especially allies) have taken advantage of the generosity of the US. To Trump and his supporters, the US enabled global prosperity — global stability and security from the US defence spending on its military, and global trade, demand for goods, financial intermediation and stability, global investments and capital flows from the US dollar as the reserve currency. While Americans pay the price, others reap the benefits. It is time to pay back to America.

Contrast this with the 1961 speech by President John F Kennedy. Either the Americans’ attitude to the rest of the world has changed, or that America alone can no longer afford the burden, the price to pay for global leadership of the free world.

What is critical to understand is that the Trump administration intends to link its provision of international security and stability (US defence shield) to terms of trade (tariffs), investments and the international financial system (US dollar as the reserve currency). In other words, security, trade and finance are a package deal. If you benefit from one, you must pay with the other. And since the US is the provider of all these enablers, it demands to be paid, whether from friend or foe.

Tariff is only a means to an end

Trump and his associates see tariffs on imports as the solution to gain revenue and for import substitution — to shift manufacturing back to the US, to reindustrialise and create jobs for Americans. The tax revenue collected from tariffs would be directed towards lower corporate taxes to stimulate domestic investments and infrastructure building. The Department of Government Efficiency’s (DOGE) plan to reduce government expenditure, purge wastages, and deregulate the economy and reduce red tape and bureaucracy will enable more investments, enhance efficiencies, and improve US competitiveness, thereby raising exports.

But tariff is NOT the endgame. It is only a means to an end! This is where other commentators, economists and analysts are getting it all wrong on President Trump.

First, tariffs cause domestic prices to rise and this hurts Americans. Higher inflation also means higher interest rates — bad for the economy, for investments, for the equity and bond markets and terrible for the housing sector. Trump was a developer — he understands this impact.

We wrote last week that the US domestic price impact of tariffs can be mitigated by a stronger US dollar (currency offset). This happened in 2018-19. We think it will happen again — at least in the short term. Also, in the short term, exporters in foreign countries can be pressured into assuming part of the cost of the tariff. These foreign producers will do so if only to ensure cost competitiveness by maximising their capacity utilisation at the factories. The short-term goal of these manufacturers is to cover their marginal cost of production.

Now, this timing is important. If Trump believes currency offset and foreign exporters will reduce their price (but only in the short term to maximise profit or minimise losses) because of the newly imposed tariff to sell to the US market, then the new tariff on imports will cause minimal to no US domestic inflation. In the short term at least. Meanwhile, revenue to the US will increase, giving Trump the ability to cut taxes to stimulate investments and consumption and strengthen the US dollar. Thus, Trump can use tariff as an immediate and short-term tool effectively.

However, tariff is not a permanent tool.

We explained the paradox of the MAGA Pathway last week. To negate the inflationary effect of tariff, the US dollar will have to rise. But the higher the dollar, the more uncompetitive US exports will be. Imports become cheaper, making the trade deficit even worse. Furthermore, for foreign exporters to the US, the products they sell must cover both the fixed and variable costs (not just the marginal cost of production) to be sustainable. Therefore, tariff alone is only a short-term tool.

Another limitation of tariff is that any gains from imposing tariff disappears when the tariffed nations retaliate by imposing their own tariff on US exports. The breakdown of global trade will lead to a lose-lose outcome for both the US and the world. Arguably, since Americans enjoy a higher standard of living than most other citizens, the “marginal pain” of a global economic contraction arising from a trade war could hurt the American consumer more than others. We think Trump needs quick wins, not long dragged-out trade wars. This explains his aggression and urgency now.

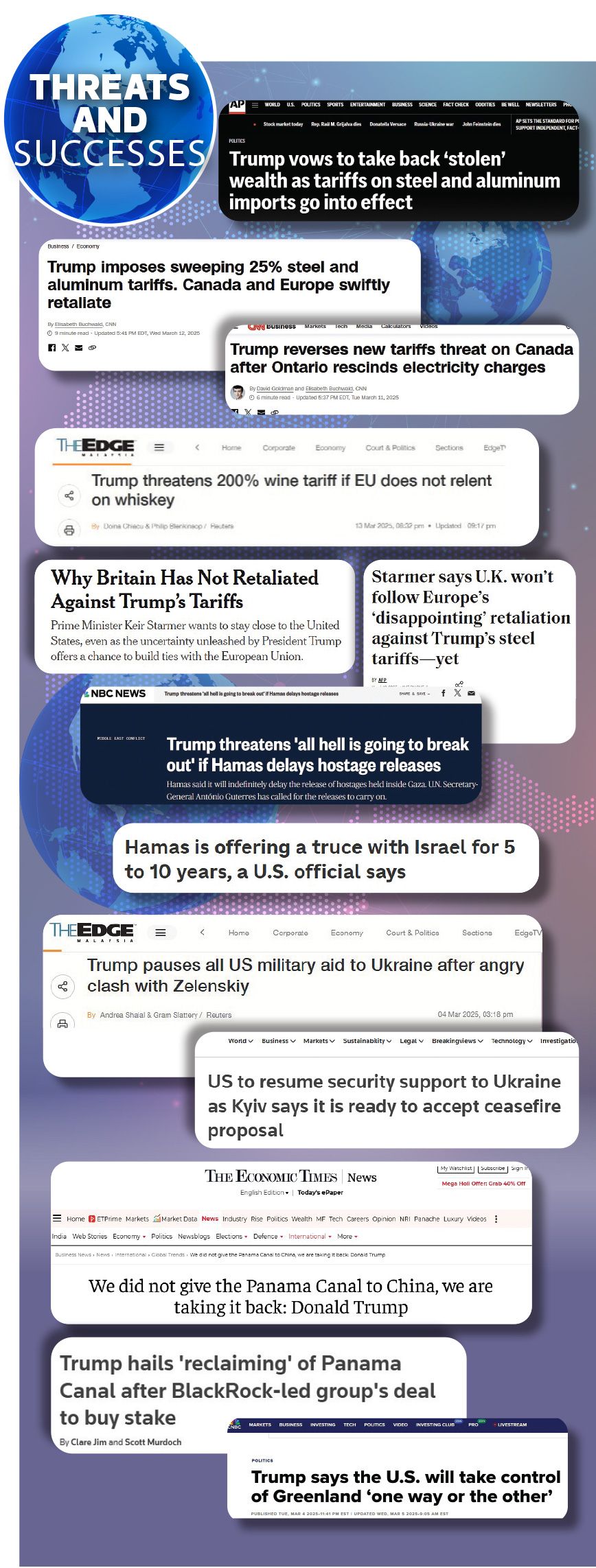

Trump’s method: The art of the deal

We go to Trump to understand how he thinks — as he relates about himself in his memoir, his business advice book, Trump: The Art of the Deal. We asked ChatGPT (an American AI LLM tool) for a summary.

In the book, Trump frequently emphasises an aggressive, high-pressure approach to negotiation, often pushing opponents into corners to secure the best possible outcome for himself. He advocates tactics such as exaggeration, bluffing and strategic deception — what he calls “truthful hyperbole” — to build perception and gain leverage. Trump leverages fear, uncertainty and urgency to pressure others into making concessions. He describes a “hit first” mentality, striking before the other party can gain an advantage. He also believes in creating a sense of inevitability around his deals — presenting himself as the only viable option, leaving the other side with little room to manoeuvre.

The book illustrates coercion in various forms — legal battles, media manipulation or exploiting bureaucratic loopholes. Overall, The Art of the Deal presents business as a high-stakes game where power, intimidation and psychological manipulation are key tools for success.

We add: as president of the US and as the world’s most powerful person, Trump is now playing a high-stakes game to Make America Great Again! Can he succeed? Through fear and coercion, can he gain the concessions he needs? Will it be win-win through growth or a zero-sum gain? Who must pay, who loses if the US were to gain?

The collage of news articles presented here depicts what Trump has done in just seven weeks since his second inauguration as president of the US. How he had shocked the world, hit first, hit hard aggressively, from tariffs to freeing the hostages in Gaza, to Ukraine, and the threat to annex Canada, Greenland and Panama. How he has used the same approach articulated in The Art of the Deal to force Ukraine to accept ceasefire talk and hand over mineral rights, forcing an ethnic Chinese-owned private entity to sell the ports in Panama, forcing the Hamas-Israeli ceasefire, forcing Ontario to rescind higher electricity charges on Americans by threatening even more tariffs, frightening the UK from imposing retaliatory tariffs.

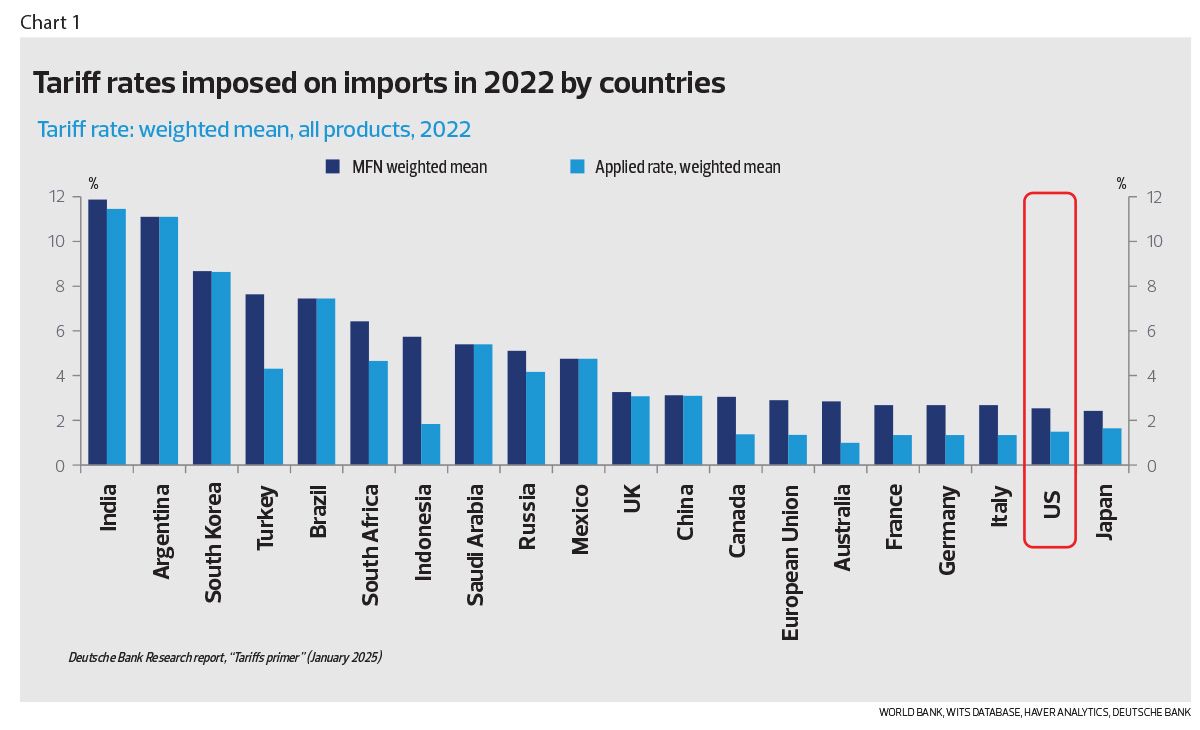

Table 1 shows the countries with the largest trade surpluses with the US. It is no surprise that the first three Trump aggressively levied tariffs on are China, Mexico and Canada. Europe came next, and Trump has already sounded warnings to Japan and South Korea. Surely Vietnam is next in sight, and likely other Asean countries and India. In the case of Mexico and Canada, the US has asked that they too impose tariffs on Chinese goods, so that those goods do not avoid the US tariffs through trade rerouting (whether as finished goods or part of the supply chain). The same will be demanded of other countries. This is why we said in one of our past articles, “Goodbye ‘China+1’ strategy”.

Chart 1 shows the weighted mean tariff rates imposed on imports by countries. Surely, one would expect Trump to target those countries that impose high tariffs on their imports. This is what the term “reciprocal tariffs” means. India, South Korea, Turkey, Brazil, South Africa and Indonesia will be hit.

President Trump is using the imposition of tariffs (not just the threats) to do deals for America. He wants other nations to know he is serious. He wants to inflict fear, pain, uncertainties, urgency and inevitability around his deals.

Tariffs will be used as a tool to leverage upon when negotiating burden sharing. Graduated tariff scales on other nations will be based on their agreement to share the burden of the US dollar as reserve asset and the US providing defence and security arrangements. The more a nation shares the US burden, the lighter the tariff. This is what Bessent meant when he said “partners should be scored”.

The fact is almost all nations will make concessions to the US, whether friend or foe. It is realpolitik. Extracting non-retaliatory measures or only partial retaliation in tariffs will be a start. The US gains revenue, more investments and jobs, more exports and an expanding share of the global economy. This is inevitable for the near term. Many will feel aggrieved by such coercion. To Trump, economic security is national security.

But remember, tariff either causes inflation or appreciating currency. And a higher US dollar makes imports cheaper, worsening the US deficit (the paradox). In the longer term, it is not in the interest of the US for the dollar to be overvalued. But as long as it is the reserve currency, it will be overvalued (Triffin World). The US dollar is used for trade or business transactions, for financial investments and for foreign exchange reserves by central banks around the world. And the US dollar in circulation will keep growing for as long as there is global economic growth for the above use.

How to drive down the US dollar so that it is not overvalued? Make central banks around the world sell their US dollar reserves gradually. In return, these countries buy their own currencies, thus driving them up, making US goods cheaper and reducing their trade surplus with the US. And, making them sell the US dollar in their foreign currency reserves for perpetual US Treasury securities, or UST (terming out the US debts — interestingly, in accounting, perpetual debts are classified as equities, not debts). It means that risk on the US economy now is shared with these foreign nations — or to quote Bessent, “shared interest ultimately strengthens the international system”.

Table 2 shows the countries with the largest total reserves, including the US dollar. Will these nations be willing or be forced to share the burden of the US dollar as the reserve currency? And what are the economic and financial implications to these countries if they do? It is no surprise that China’s gold reserves have risen consistently.

Will Trumpianomics succeed?

For a start, we have already seen many global companies and funds committing to invest in the US — to create jobs and improve US productivity and competitiveness in exchange for favours. The recent announcement by Germany to expand its defence spending is another win for Trump. In the last two months, he has clearly succeeded in extracting many concessions.

It also depends on whether the rest of the world believes the narrative that the US is the victim, that it has made great sacrifices for the benefit of the world and now must be repaid. The burden of the cost of providing both defence umbrella and the reserve currency to facilitate global trade and investments must be shared — and this includes accepting tariffs from the US without retaliation and long-tenured or perpetual UST, which may never be repaid. Or will the world perceive it as a bully, an aggressor to make the world pay up the debts of the past and future from its own excessive and extravagant spending? (Read the accompanying article,“Is the US the victim [Trumpianomics] or the aggressor [conventional economics]?” for a more detailed discussion on this.)

As we said, in the short term, almost all nations will yield some sort of concession to the US — this is inevitable. But what are the costs and consequences in the longer term to the US? And to the world?

Challenges to implementingTrumpianomics

1. While the US dollar must initially appreciate with the implementation of new tariffs against a nation (currency offset) to ensure minimal inflationary impact on the US economy, it must gradually fall over time. This ensures the US dollar is not overvalued to reduce the trade deficits. However, to achieve any multilateral agreement with central banks around the world to manage a gradual decline in the US dollar will be extremely difficult.

2. Additionally, the private sector also holds US dollars. Although central banks around the world hold an aggregate of some US$7 trillion of the US dollar, the average daily trading volume of the US dollar was $6.6 trillion in 2022. And financial markets, even more so currency markets, are very efficient to discount forward. It would be surprising if such a gradual movement in the price of a major financial asset can be executed without sharp and quick price adjustments.

3. The US could apply a unilateral currency

approach to drive up the value of the currencies of its trading partners. This includes imposing a user fee on those using the US dollar for foreign exchange reserves. Or using the Federal Reserve to buy foreign assets or currencies. But if foreigners suddenly decide to hold less US dollars, US interest rates will spike with adverse consequences to the capital markets.

4. There is also the question of time. The concessions that Trump wants from each of these nations are huge with long-term impact. Given that he has only a single term of four years as president, would most nations not procrastinate and pay the short-term price?

5. The entire plan itself is audacious and will change the entire global economic and financial order for decades to come. Many parts of the execution will be sequential and contingent on another event or decision. It will take a lot more than time. And China, in particular, will not be willing to ever suffer another “Century of Humiliation”. World War III seems more likely than for China to be again subjugated.

Conclusion

Trump believes that the present economic order, trade arrangements and financial system no longer serve the interests of the US. He wants to recreate a new world order for the benefit of the US.

The obvious target is China, the country Trump — and the most recent former US presidents — see as the primary challenge to US supremacy. The difference is that Trump articulates this openly. And critically, unlike in the past when the US built a “coalition of the willing” to achieve its objectives, Trump believes the US can go it alone. Or more likely, he can do a deal with China. Hence, he is also inclined to extract as many concessions as he can from US allies.

Trump thinks that the US has been taken advantage of — it is the victim, bearing the burden for the world, while other nations prosper. The US alone pays the price in providing global peace and security, facilitating global trade, banking and finance, ensuring countries have US dollar reserves to support trade and investments, leading to an overvalued US dollar, and persistent trade deficits. The use of coercion to address a deficit in fair trade reminds us of the Opium Wars (read also our sidebar article).

This is his “truth”, which is the narrative that underpins Trumpianomics. Of course, many others think the US is the unreasonable aggressor and bully, trying to force other weaker nations to pay for its past excessiveness and extravagance.

Which argument is more convincing? As we have shown, economic arguments can be made for both cases. It depends on what one takes as the “prime mover”, what is the main variable that creates the chain reaction. Depending on the starting point of one’s analysis, there will be a different cause and effect.

In reality, both views have some elements of truth. In fact, Trump has used this game plan to exaggerate; to bluff, as he conveyed in his memoir. He calls it “truthful hyperbole”. And ultimately, does it matter which story or narrative one believes in? Whether Trump’s truth is the “real or whole truth” or otherwise is largely irrelevant. It is what he believes in, his truth. Trump will say what he means and do what he says. Trumpianomics will be implemented. Can he cut the deals that are needed for Trumpianomics to work? There is a plan, a small window, but one that will be extremely difficult to execute. Thomas Friedman is right; a Great Unravelling is Underway.

Our investment thesis for 2025/26

Regardless of the success or failure of Trumpianomics, these are the likely effects and implications for investments:

1. The world will get even more polarised. Nations will be defined by the US as either friend or foe. Friends get security protection but must share more of the US’ burden of debts and give it a greater share of the revenue (whether via tariffs, business concessions or redirecting investments into the US). Friends will also be asked to impose similar tariffs on nations considered non-friends. Meanwhile, non-friends will face high tariffs and other costs.

2. Smaller nations may find themselves with little room to manoeuvre, with higher costs imposed in the face of smaller potential global markets. A mercantilist US will be more difficult for smaller nations to make gains in terms of trade.

3. More efforts will be made to find alternative reserve currencies.

4. We will see much more volatile currency and capital markets. We suspect the exorbitant price the US demands and the elevated risks (economics, political and military) are NOT yet well understood and discounted. Also, analysts and fund managers need an excuse to change their story, their past bullish narratives — and they have found that in Trump.

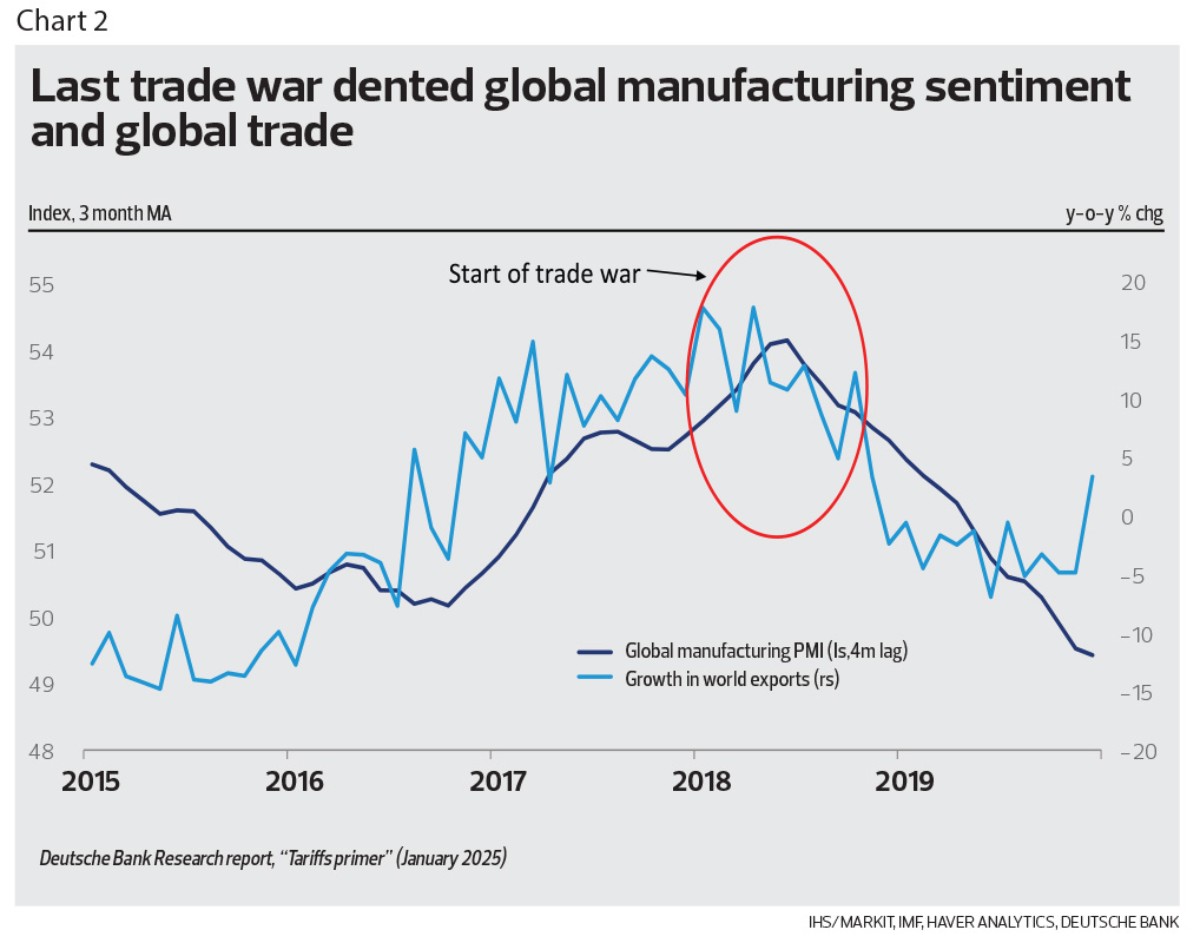

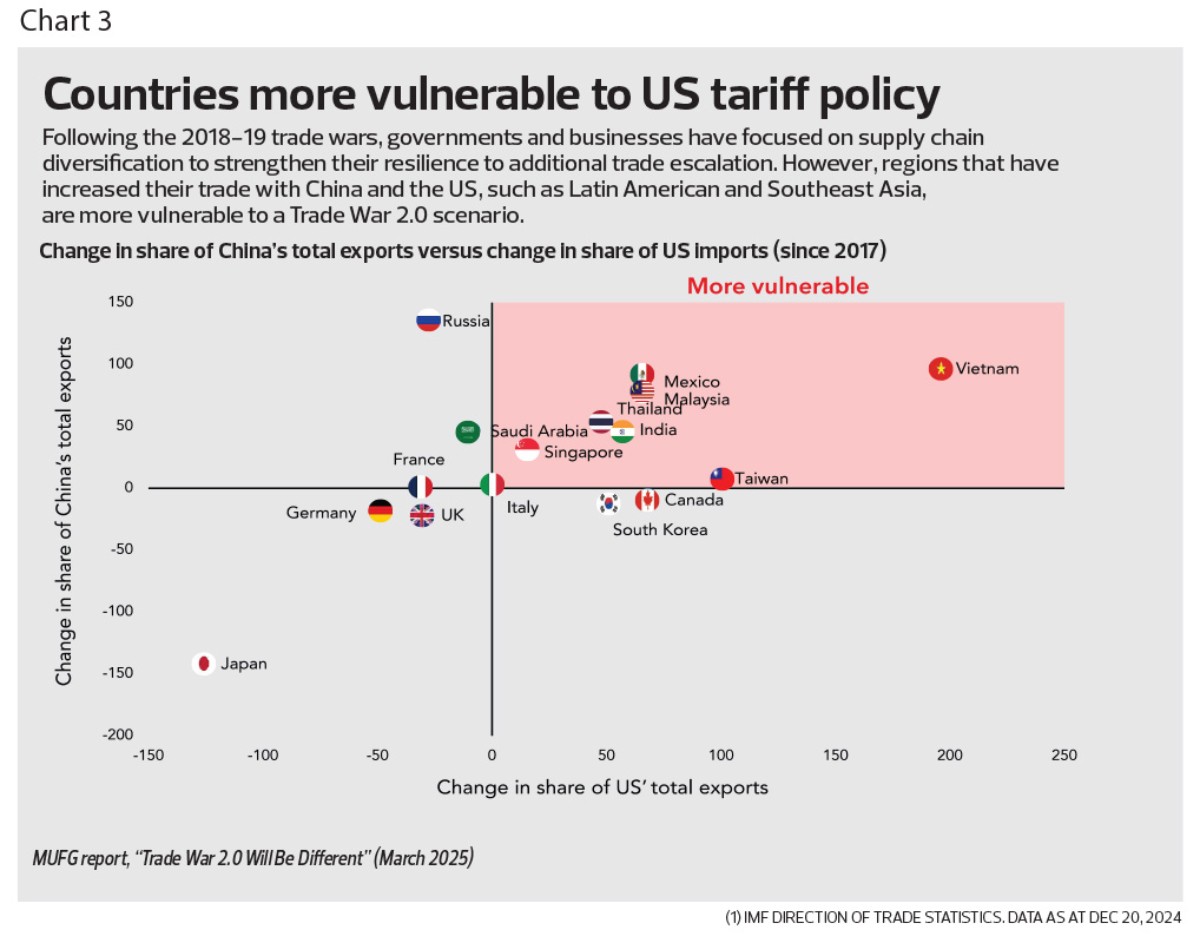

Near term, we like the US dollar. We believe US equities will outperform (banks, infra-related stocks) — with tariffs on imports, deregulation and lower taxes being the main catalysts. We also like gold, given the likely increasing intensity to find an alternative to the US dollar as reserve asset. We will also begin to gradually switch from equities to bonds over time, as economic growth will inevitably slow (see Chart 2) — and because we believe the markets have not yet factored in the elevated risks and exorbitant “transfers” the US will demand. Chart 3 presents the countries more vulnerable to US tariff policy. The imposition of new tariffs is inevitable. If we could, we would certainly be shorting Vietnam and India now.

The Malaysian Portfolio recouped some lost ground, gaining 2.2% for the week ended March 19. The top gainers were Insas Bhd — Warrants C (+9.1%), Kumpulan Kitacon (+5.0%) and Kim Loong Resources (+2.7%) while Harbour-Link Group was the sole losing stock in our portfolio. Given the escalating risks, we decided to reduce our stock holdings — disposing of all our shares in IOI Properties Group, Gamuda and KSL Holdings — and raising cash to 54.5% of total portfolio value. Total portfolio returns now stand at 184.8% since inception. This portfolio is outperforming the benchmark index, which is down 17.1% over the same period, by a long, long way.

The Absolute Returns Portfolio also traded higher last week, ending up 2.8% and lifting total returns since inception to 23.8%. All stocks closed higher save for CRH, which was down 1.1%. The biggest gainers were Berkshire Hathaway (+5.5%), Grab Holdings

(+5.5%) and CrowdStrike (+5.2%). We disposed of all our holdings in Talen Energy,pocketing a return of 12.4% for our five-month investment.

Disclaimer: This is a personal portfolio for information purposes only and does not constitute a recommendation or solicitation or expression of views to influence readers to buy/sell stocks. Our shareholders, directors and employees may have positions in or may be materially interested in any of the stocks. We may also have or have had dealings with or may provide or have provided content services to the companies mentioned in the reports.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Appellate court upholds RM3.2m forfeiture of valuables from ex-Johor exco, real estate agent

- Gamuda says to sign several 'imminent' large contracts, as 2Q profit grows 4.8%

- CCC-ECRL recognises excellence of 18 local vendors for outstanding contributions to ECRL project

- UOB Kay Hian appoints Anne Leh as new CEO

- KLIA Master Plan under review, brick-and-mortar expansion on hold — MAHB

- Cops probing video, organisation suspected of promoting communist ideology

- Atlantic releases full Signal text chain on Houthi attacks

- Used cooking oil now main commodity in production of sustainable aviation fuel

- 14,000 pigs culled so far in Selangor to curb ASF outbreak, says Veterinary Services Dept

- Bursa Malaysia, subsidiaries to close for Hari Raya Aidilfitri