KUALA LUMPUR (March 24): Bank Negara Malaysia (BNM) says the interim measure of spreading medical premium adjustments over three years is expected to negatively impact the net underwriting income of life insurers and family takaful operators.

According to the central bank’s Financial Stability Review — Second Half 2024 released on Monday, medical payouts by life insurers and family takaful operators rose to RM6.2 billion in the second half of 2024 (2H2024), from RM5.3 billion in both 1H2024, and 2H2023.

This increase in medical payouts was due to a rise in overall average cost and utilisation of medical treatments, particularly for chronic and acute cases, according to BNM, “which led to premiums for medical and health insurance/takaful (MHIT) policies/certificates being adjusted upwards to ensure the sustainability of long-term coverage”.

But the interim measure — of staggering premium hikes over at least three years — combined with increased payouts from medical claims and the ongoing decline of participating life insurance businesses, could further strain the net underwriting income of life insurers and family takaful operators, said BNM.

“In this regard, structural reforms addressing the root cause of rising medical costs are crucial in ensuring the sustainability of the MHIT business,” BNM added.

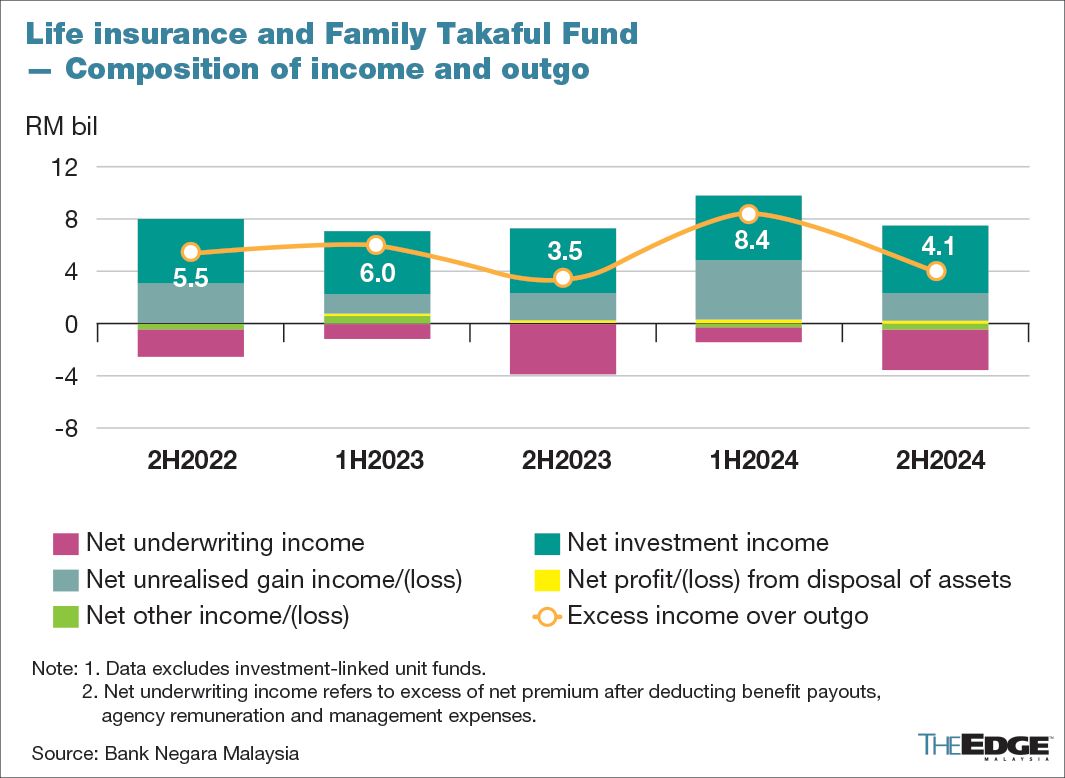

Profit dropped in 2H2024 on lower paper gains

The overall profitability of life insurance and family takaful funds, measured by excess income over outgo or expenditures (EIOO), slowed to RM4.1 billion in 2H2024 from RM8.4 billion in 1H2024. This decline was primarily because of lower net unrealised gains from investments, following weaker equity performance and higher bond yields.

Nevertheless, for the full 2024, EIOO rose to RM12.4 billion from RM9.4 billion in 2023, supported by the equity market’s stronger year-on-year performance.

New business premium for life insurers and family takaful operators grew 6.4% in 2H2024 — a slight dip from 6.8% in 2H2023. Growth in 2H2024 was primarily driven by growth in new business premiums for investment-linked products.

“The participating life insurance segment continued its decline amid shifts in consumers’ preference for broader coverage against life uncertainties, such as medical and health coverages, which are not typically covered by participating life insurance policies.

“Investment-linked products, perceived to be more flexible, are expected to remain a key driver of overall new business premium growth,” BNM said.

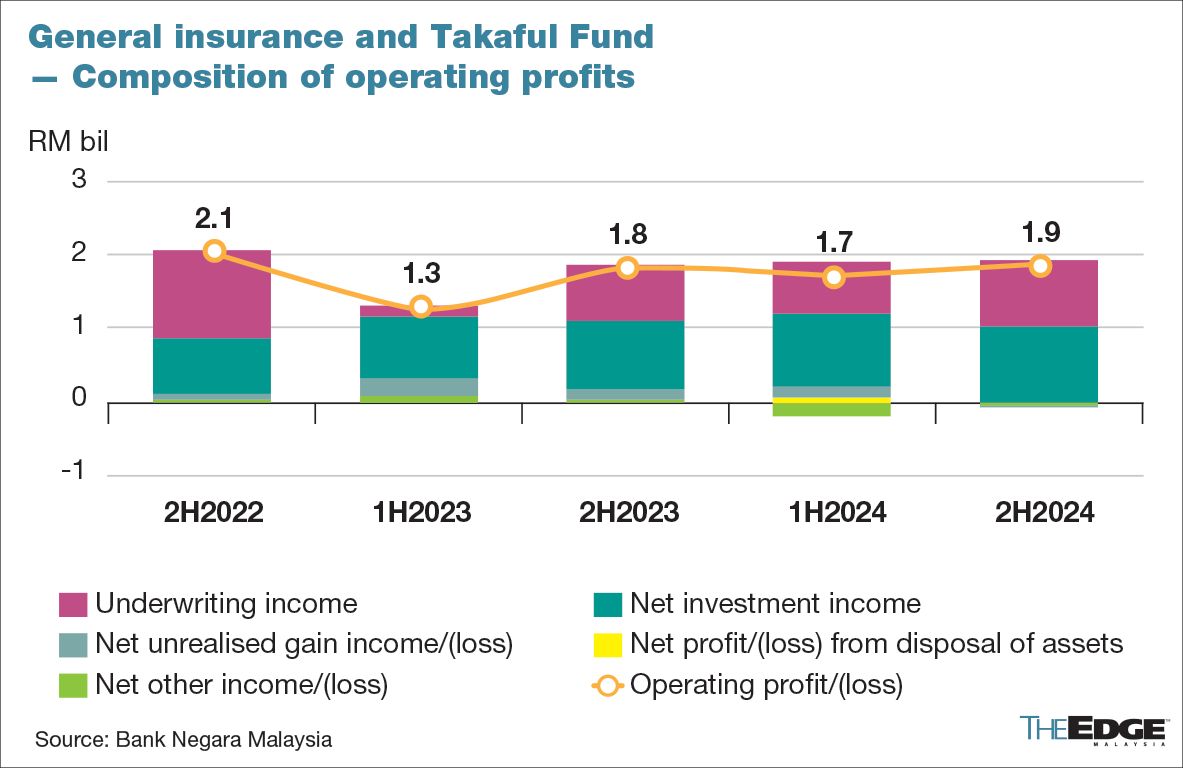

For general insurance and takaful funds, operating profits rose to RM1.9 billion in 2H2024, from RM1.7 billion in 1H2024 and RM1.8 billion in 2H2023, supported by underwriting profits that were boosted by growth in the motor segment, reflecting stronger demand for motor vehicles, and by lower claims from fire events.

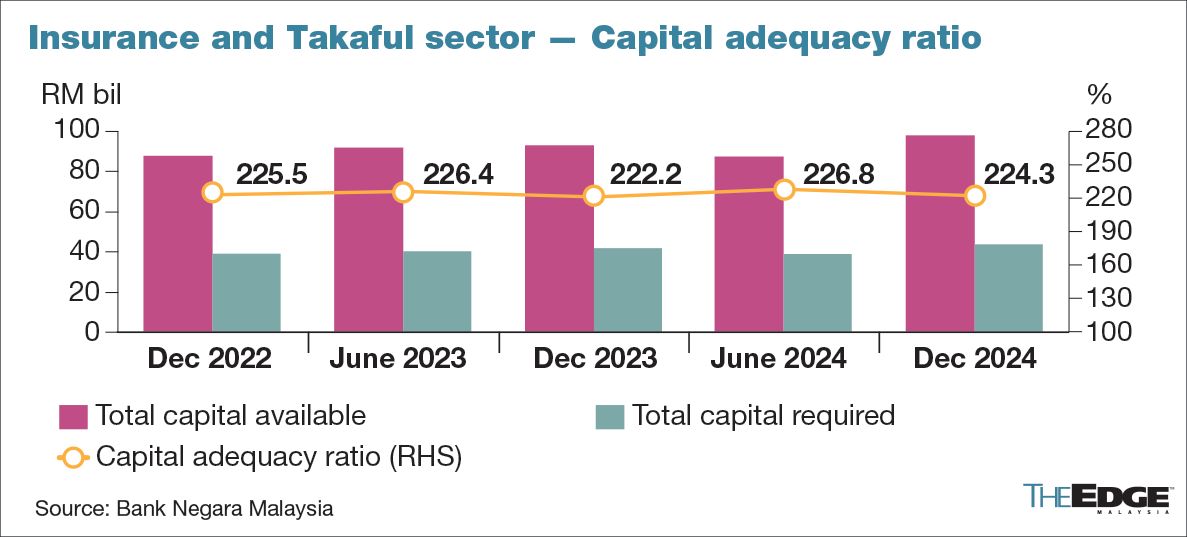

Overall, the industry’s aggregate capital adequacy ratio remained healthy at 224% as of end-December 2024, above the regulatory minimum of 130%, albeit lower than 227% at end-June 2024.

Capital buffers, exceeding regulatory requirements, remained ample at RM41.1 billion, compared to RM37.4 billion at end-June 2024.

Looking ahead, BNM said the investment performance of insurers and takaful operators remains vulnerable to financial market conditions, given their substantial investment holdings in bonds and equities, as well as climate-related risks.

“Insurers and takaful operators could also face constraints in growing new MHIT businesses due to concerns about medical cost pressures, which make current pricing structures unsustainable.

“The measures taken by insurers and takaful operators to provide short-term relief to policyholders/participants from the repricing of MHIT premiums are also expected to weigh on the financial performance of the industry,” BNM said.

“Despite these potential headwinds, insurers and takaful operators are expected to remain solvent, with capital buffers above the regulatory minimum,” the central bank concluded.

- Gamuda says to sign several 'imminent' large contracts, as 2Q profit grows 4.8%

- UOB Kay Hian appoints Anne Leh as new CEO

- KLIA Master Plan under review, brick-and-mortar expansion on hold — MAHB

- Gas Malaysia declares final dividend of 10.28 sen per share

- Malaysia’s trade at risk amid US semiconductor tariffs, research group says

- Cops probing video, organisation suspected of promoting communist ideology

- Atlantic releases full Signal text chain on Houthi attacks

- Used cooking oil now main commodity in production of sustainable aviation fuel

- 14,000 pigs culled so far in Selangor to curb ASF outbreak, says Veterinary Services Dept

- Bursa Malaysia, subsidiaries to close for Hari Raya Aidilfitri