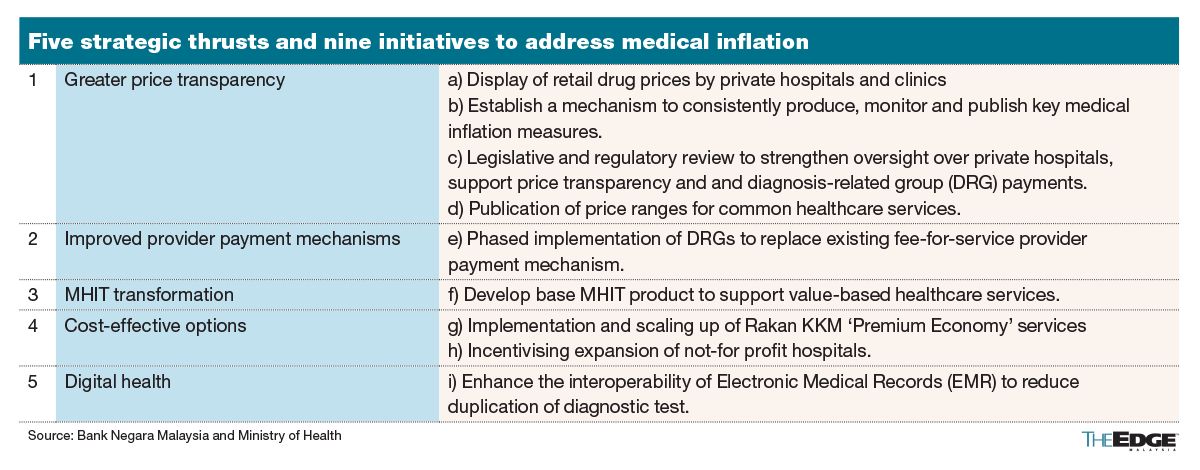

KUALA LUMPUR (March 24): The Ministry of Health (MOH) will review the regulatory oversight of private hospitals as part of efforts to promote greater price transparency and curb medical inflation, according to Bank Negara Malaysia (BNM).

This initiative is one of nine under five strategic thrusts aimed at controlling medical inflation, which is projected to reach 15% in 2025, significantly higher than the global and Asia-Pacific averages, according to BNM’s Annual Report 2024.

Between 2021-2023, the total cost of medical health insurance and takaful (MHIT) claims increased by 73%, far surpassing the 21% growth in MHIT premiums collected.

According to BNM’s report, medical inflation is driven by higher treatment costs and increased usage of medical services, among others, as reflected in the rise in claims frequency.

In 2018, there were 11 claims per 100 people, but by 2023, this more than doubled to 25 claims.

The issue is worsened by the high and unregulated costs of hospital supplies and services (HSS), such as drugs, lab fees, and consumables like gloves. These costs, which make up 59% to 70% of private hospital bills, significantly impact overall claims expenses.

Efforts to promote greater price transparency outline three other initiatives, which include the display of retail drug prices and the publication of cost ranges for common healthcare services.

This will enable policyholders, and insurance and takaful operators (ITOs) to compare prices across medical providers, while fostering competition, according to the central bank.

Additionally, a mechanism to consistently produce, monitor and publish key medical inflation measures will be developed, to better align the methodology with how general inflation is calculated.

The second strategic thrust aims to address the disparity in total treatment costs for similar medical conditions between policyholders using cashless facilities, where ITOs issue guarantee letters and pay medical providers directly, and those who pay out-of-pocket upfront and later seek reimbursement from ITOs.

BNM said an improved provider payment mechanism will be introduced in the form of diagnosis-related groups (DRG) to replace the current fee-for-service model at hospitals.

Under DRG, patients are categorised based on their diagnoses and medical needs, with severity and co-morbidities factored in. Each group is then assigned a predetermined payment amount, encouraging efficiency, better health outcomes, and price predictability, the central bank said.

DRG pricing was one of the many recommendations presented by the Life Insurance Association of Malaysia (LIAM), the Malaysian Takaful Association (MTA), and the General Insurance Association of Malaysia (PIAM) during a session with the Public Accounts Committee (PAC) in Parliament on Feb 26, 2025.

PAC held its first public hearing last month, acknowledging rising public concerns over increasing private hospital charges, surging insurance premiums, and their broader impact on the healthcare system.

In its report, BNM said another strategy focuses on restructuring MHIT offerings by introducing a base product to ensure sustainable premiums through larger risk pooling and cost containment. The base product will include measures such as DRG implementation, prioritisation of a cost-effective benefits package, and strategic purchasing of healthcare services.

BNM and the key stakeholders also aim to increase the supply of affordable mid-tier hospital beds through the expansion of the Rakan KKM initiative by MOH, which can also serve as a price benchmark, and by incentivising the growth of not-for-profit hospitals.

This initiative will provide more cost-effective options for policyholders.

Lastly, enhancing the interoperability of electronic medical records (EMR) across hospitals will improve accessibility and continuity of care by addressing fragmented health records. Better data portability will help minimise duplicate tests and procedures, boosting operational efficiency and reducing costs over time, the central bank added.

According to BNM’s Annual Report 2024, 61% of affected policies experienced less than 20% premium increase, while about 9% of affected policies experienced more than a 40% premium increase.

In December last year, BNM introduced interim measures to support policyholders affected by the premium repricing.

They include spreading out premium/contribution increases over three years (until 2026), capping annual hikes below 10% for around 80% of policyholders/certificate holders, and offering a one-year premium freeze for policyholders/certificate holders aged 60 and above on minimum MHIT plans.

Additionally, policyholders/certificate holders whose policies/certificates lapsed in 2024 due to repricing can reinstate coverage without new underwriting, while ITOs will introduce alternative, more affordable MHIT products by 2025.

BNM in its annual report emphasised that interim measures cannot continue if high medical inflation persists. Therefore, it is crucial for key stakeholders to implement comprehensive and effective health reforms to tackle medical inflation.

- UOB Kay Hian appoints Anne Leh as new CEO

- Gas Malaysia declares final dividend of 10.28 sen per share

- Kenneth Vun now MD at both Symphony Life and XOX

- Change of guard at Ekuinas — sources

- LSH Capital, Matrix Concepts, Symphony Life, Gamuda, Gas Malaysia, Kim Loong, United Malacca, MyNews, Marine & General, Dayang, Nestcon, Solarvest, Rohas Tecnic, Bintai Kinden

- Xpeng may add EV output in Europe, Latin America in growth push

- Xi tests US allies in Indo-Pacific as Trump looks elsewhere

- Trump says he could cut China tariffs to secure TikTok deal

- Trump weighs imposing copper import tariffs in weeks, not months

- Trump to hit auto imports with 25% tariff in trade fight