This article first appeared in Capital, The Edge Malaysia Weekly on February 3, 2025 - February 9, 2025

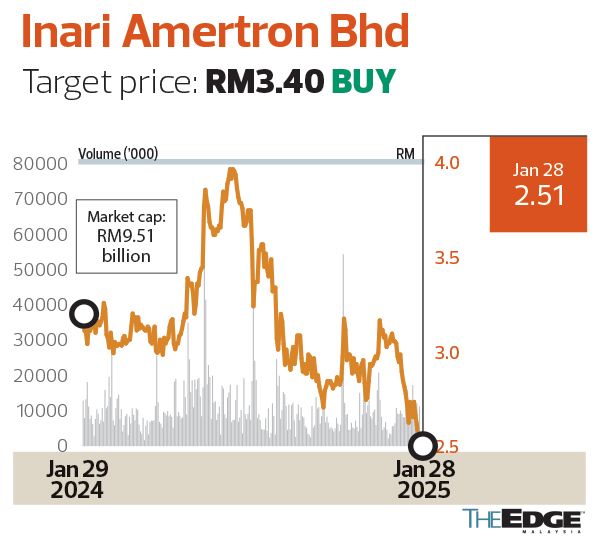

Inari Amertron Bhd

Target price: RM3.40 BUY

UOB Kay Hian Research (Jan 23): We recently visited Inari Amertron Bhd’s (KL:INARI) P13 plant in Penang and gained insights into its advanced packaging roadmap. While its 2025 growth will remain largely driven by its flagship radio frequency (RF) business (anchored on System-in-Package technology using flip-chip), the group has begun venturing into advanced packaging platforms such as flip-chip chip-scale packages, flip-chip ball grid arrays and 2.5D/3D stacked packaging.

These technologies offer ultra-high performance, high memory bandwidth and heterogeneous integration capabilities to cater to the increasing demand for cutting-edge semiconductor solutions in artificial intelligence (AI), server, networking, smart devices and industrial applications.

Venturing into advanced packaging is a game-changing move that demands state-of-the-art technical expertise, significant capital investments, a supportive ecosystem and strong customer commitment. While this combination of factors establishes a formidable barrier to entry, the advanced packaging market presents a highly lucrative opportunity on an expected compound annual growth rate of 11% from 2023 to 2029 (according to market analysis group Yole). To drive its success roadmap, we gather that Inari is in close collaboration with its key technology partners and is poised to commercialise its new product pipelines in the coming quarters. Meanwhile, this strategic initiative is also bolstered by its strong foundation of existing capabilities, a well-established customer portfolio and the backing of Malaysia’s progressive policies.

Inari’s advanced packaging strategy is well-aligned with Malaysia’s National Semiconductor Strategy, introduced in 2024 to foster high-value semiconductor manufacturing. With RM25 billion in fiscal support and RM3 billion specifically allocated for capital grants, R&D and modernisation, the National Semiconductor Strategy provides a significant boost for industry leaders such as Inari. Leveraging its position as a key outsourced semiconductor assembly and test player, Inari is poised to benefit from this policy rollout through cost optimisation and enhanced competitiveness. As the semiconductor landscape experiences dynamic growth and transformation, Inari’s alignment with national initiatives and its forward-thinking roadmap solidify its role as a key contributor to Malaysia’s semiconductor ambitions.

Maintain “buy” with an unchanged target price of RM3.40, still based on 35 times 2025 forward price earnings (PE) (+1 standard deviation (SD) above five-year mean forward). At 24.8 times ex-cash 2025 forward PE (close to -1SD below its five-year forward mean) with negative de-ratings (cyclical bottom) being priced in, we see a balanced risk-reward ratio for a favourable entry point.

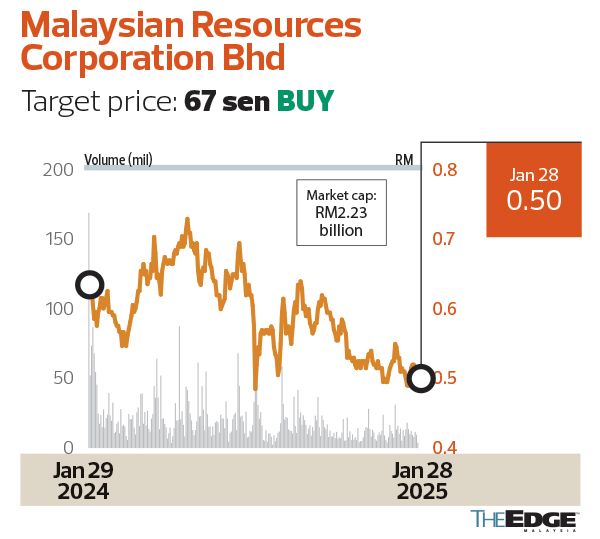

Malaysian Resources Corporation Bhd

Target price: 67 sen BUY

MIDF Research (Jan 27): We are maintaining our earnings estimates as the recently announced joint venture for Hospital Putra in Melaka and the Ipoh Sentral transit-oriented development (TOD) project are within expectations and aligned with Malaysian Resources Corporation Bhd’s (KL:MRCB) replenishment strategy. The projects are not expected to materially impact MRCB’s net assets or earnings for FY24/25. Earnings recognition for Hospital Putra is expected to commence progressively as the project reaches significant milestones, while Ipoh Sentral’s phased development timeline points to earnings contributions starting from FY26 and spanning up to 20 years.

We maintain our target price at 67 sen pegged to a +1SD historical forward price-to-book ratio of 0.64 times on the group’s estimated FY25F book value per share of RM1.04. These wins strengthen MRCB’s project pipeline and reinforce confidence in its ability to deliver sustainable long-term growth.

On Jan 24, MRCB Land Sdn Bhd (MLSB), a wholly-owned subsidiary of MRCB, entered into a joint venture (JV) and shareholders’ agreement with PM Multilink Sdn Bhd (PMM), a subsidiary of Melaka Corporation. The JV, through Majestic Quest Sdn Bhd, is structured as 70% MLSB and 30% PMM, to develop Hospital Putra in Melaka Tengah. The gross development cost for Phase 1 is estimated at RM520 million.

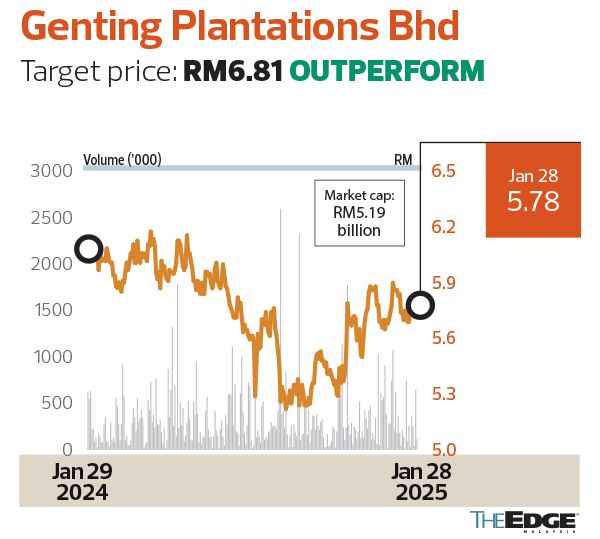

Genting Plantations Bhd

Target price: RM6.81 OUTPERFORM

PublicInvest Research (Jan 27): Genting Plantations Bhd (KL:GENP) has proposed to dispose of three parcels of agricultural land with a total land size of 528 acres in Melaka Tengah for a total cash consideration of RM333.8 million or RM14.50 psf to a subsidiary company under Scientex Bhd (KL:SCIENTX). The proposed land sale is expected to contribute a lucrative one-off gain of about RM284.9 million or additional earnings per share (EPS) of 32 sen to the FY25 performance. Pending the completion of the land sale, we make no changes to our earnings forecast.

According to the announcement, the subject land was acquired in 1981 at an original cost of investment of RM2.1 million or based on 9 sen psf, giving the group a lucrative one-off gain of about RM284.9 million (after tax and related expenses). It is worth noting that the subject land has a net book value of only RM4.42 million as at FY23. The land sale gain of RM284.9 million or 32 sen per share is expected to be recognised in the second half of 2025. Apart from that, the group could also save the replanting cost estimated at RM6 million as the oil palm trees of the subject land are approaching the old-age category, which is deemed for replanting soon.

Axis REIT Bhd

Target price: RM2.08 BUY

RHB Research (Jan 24): Axis REIT Bhd’s (KL:AXREIT) FY24 results were in line with expectations, with double-digit earnings growth driven by the commencement of new leases following a record year in acquisitions. The REIT should see another year of strong earnings growth in FY25 from the full-year contributions of its completed acquisitions as well as its redeveloped property, Axis Mega Distribution Centre 2 (AMDC2).

Core profit of RM42.4 million (+3% q-o-q, flat y-o-y) for the fourth quarter of the financial year ended 2024 brought FY24 earnings to RM163 million (+11% y-o-y). This was in line with estimates at 100% of our and street’s forecasts. Quarter-on-quarter revenue grew 9% mainly due to the contribution of newly acquired properties, new tenancies from AMDC2 and positive rental reversions, while non-property expenses grew 13% due to additional borrowing costs incurred for the acquisitions.

FY24 revenue grew 12%, driven by the full-year contribution from Bukit Raja Distribution Centre 2 (completed in August 2023), positive rental reversions, and the completion of seven new acquisitions worth RM719 million.

As results were in line, we maintain our earnings forecasts, and introduce our FY27 earnings forecast of RM214 million.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Fire incident in Putra Heights not related to Gas Malaysia facilities, company says

- Massive gas pipeline fire in Puchong — Fire Dept

- Petronas confirms fire incident at Petronas Gas main pipeline near Puchong

- Gas pipeline blaze: 25 receiving initial medical treatment as of 10.35am

- Gas pipeline blaze victims recount earthquake-like tremors

- Directors cannot be automatically retired without an AGM, Court of Appeal rules

- LSH unit assumes management of KL Tower for 20 years until end-March 2045

- SpaceX eyes Starlink hub with multiple ground stations in Vietnam — Reuters

- Teleport to raise a maximum of US$100 mil for capacity expansion

- Gas pipeline blaze: 82, including 12 injured rescued — Selangor MB