This article first appeared in The Edge Malaysia Weekly on January 27, 2025 - February 2, 2025

WHEN the acquisition of a 16% stake in Sunway Bhd’s (KL:SUNWAY) healthcare arm by Singapore’s GIC Pte Ltd was announced in June 2021, the valuations ascribed to the healthcare group were considered mighty lofty.

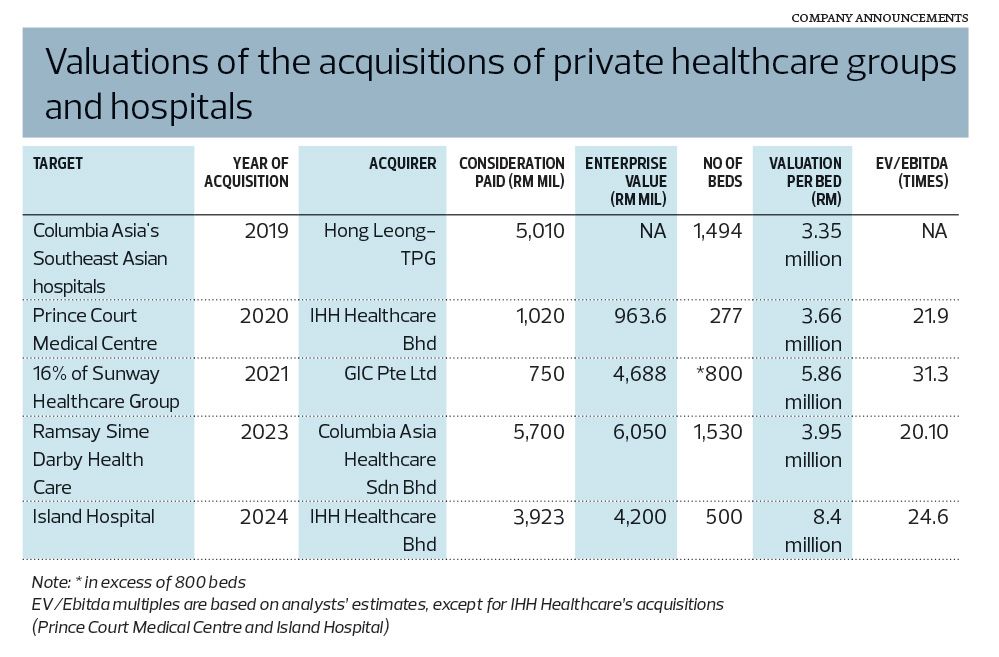

At RM750 million for 16%, Sunway Healthcare was valued at around RM4.7 billion with an implied enterprise value-to-earnings before interest, taxes, depreciation and amortisation (EV/Ebitda) of 31.3 times, based on the group’s then Ebitda of RM130 million.

That was not the only deal involving a major private hospital or healthcare group in Malaysia over the last six years. Except for 2022, there has been at least one major healthcare deal a year since 2019.

These transactions were largely concluded at EV/Ebitda multiples that were higher than those ascribed by the market to the only two pure-play private healthcare groups listed on Bursa Malaysia — IHH Healthcare Bhd (KL:IHH) and KPJ Healthcare Bhd (KL:KPJ).

Lofty valuations could lead to higher medical costs and inflation, an environment that Malaysia is all too familiar with. Having paid top dollar for these facilities, investors expect good returns from their investments.

“I think this would be inevitable. As it is, private healthcare is inaccessible to a large majority of Malaysians. And if there is to be a further increase in the price and subsequently the price of health insurance, it will drive people back to the public health system, which is already under immense pressure,” says Prof Datuk Dr Adeeba Kamarulzaman, CEO of Monash University Malaysia and pro vice-chancellor and president (Malaysia) of Monash University Australia. “Ultimately, healthcare needs to be looked at as a public health good and not purely commercialised for the interest of a few stakeholders.”

Prior to her appointments at Monash University, Adeeba was the dean of Universiti Malaya’s Faculty of Medicine. She is also chair of the Malaysian AIDS Foundation, as well as commissioner for the Global Commission on Drug Policy and the Global Commission on Inequality, AIDS and Pandemics.

While Adeeba recommends that healthcare be considered a public interest, private investors of healthcare groups may view it otherwise. For instance, under the agreement with GIC, Sunway “promised” the Singapore government’s investment firm an internal rate of return (IRR) of 12.5%, in ringgit terms, inclusive of a 3% preferred dividend.

The agreement comes with an obligation for Sunway to list its healthcare business by Jan 31, 2028. If it defaults on its obligation, GIC will have the right to exercise a put option that enables it to achieve a minimum IRR of 18.5%, in US dollar terms.

According to RHB Research in a June 24, 2021, note on the deal, based on an IRR of 12.5%, the equity value of Sunway Healthcare is estimated to be worth around RM10.7 billion.

“Assuming RM1 billion debt and, hence, EV of RM11.7 billion — based on an EV/Ebitda of 20 times — Sunway Healthcare would need to achieve at least RM600 million in Ebitda,” RHB Research said in the note.

This means that between 2019 and 2028, Sunway Healthcare’s Ebitda would have to grow by a compound annual growth rate (CAGR) of 18.5%. As at end-September 2024, Sunway’s healthcare segment made a profit before tax (PBT) of RM150.44 million.

The valuations of private hospitals and healthcare groups over the last six years have shown that investors are willing to pay upwards of 20 times EV/Ebitda for the assets. For example, IHH acquired Island Hospital in Penang at an EV/Ebitda valuation of 24.6 times, considerably more than the 21.9 times it paid for Prince Court Medical Centre.

In another transaction in 2023, Columbia Asia Healthcare Sdn Bhd acquired Ramsay Sime Darby Health Care Sdn Bhd at an EV/Ebitda of 20.1 times. Following the acquisition, Columbia Asia Healthcare was renamed Asia OneHealthcare Sdn Bhd (A1Health).

A streamlining of all healthcare assets under A1Health, as well as TE Asia Healthcare Partners, is apparently in the works, which would fetch a valuation of around RM15 billion. Assuming an EV of RM15 billion and an EV/Ebitda of 20 times, A1Health’s Ebitda would come to about RM750 million.

With all these investments that have poured into healthcare assets, it would not be too farfetched to say the respective hospitals would have to increase their charges and fees to ensure higher returns.

Maybank Investment Bank Bhd analyst Samuel Yin Shao Yang opines that IHH’s average bill size is expected to go up following the group’s acquisition of Island Hospital in November 2024, as more serious and complex cases such as cancer are brought in.

But will the acquisition of Island Hospital lead to expectations of increased profit for IHH on a per share basis? “Not yet because the RM3.9 billion acquisition was entirely financed by debt. Earnings will be moderated by higher interest expense until FY2026,” Yin explains.

Maybank IB forecasts IHH to record a three-year forward revenue and Ebitda CAGR of 13%, led by robust growth at its Indian and Malaysian operations, with the latter driven by bed expansion plans and the acquisition of Island Hospital.

Oong Chun Sung, an analyst at RHB Research, estimates that Island Hospital would make up 20% of IHH’s Malaysia Ebitda in 2025. Earnings from Island Hospital will only start to be consolidated in the fourth quarter of 2024.

For the nine months ended Sept 30, 2024 (9MFY2024), IHH’s Malaysia operation made RM776 million in Ebitda, which was 6.9% higher than in the previous corresponding period. In FY2023, the Malaysian operation contributed RM937.25 million in Ebitda to the group.

It is worth noting that while IHH has been acquiring hospitals at more than 20 times EV/Ebitda, the group is currently valued at around 12.6 times. According to Oong, this is 0.3 standard deviation (SD) below its historical average of 13.8 times.

Maybank IB resumed its coverage on IHH in December 2024, with a target price of RM7.97 and a “buy” call. RHB Research is more bullish with a TP of RM9.10, implying an FY2025 forecast EV/Ebitda of 16 times, which is 0.4 SD above its five-year historical average.

Could the market be undervaluing IHH because of the uncertainty over the implementation of the diagnosis-related group (DRG) pricing mechanism that was announced recently?

“Our view on IHH remains unchanged at this juncture as we believe the implementation of DRG still requires extensive study and engagement with various stakeholders, given the complexity of each medical procedure and their underlying costs,” says RHB Research’s Oong.

Maybank IB is of the view that IHH’s valuation is ripe for a rerating in 2025 with the potential listings of Sunway Healthcare and A1Health.

IHH’s main domestic competitor, KPJ, has seen its shares trade above its historical EV/Ebitda average of 12 times since the start of the year. Even so, this is still lower than the floor of 20 times that private healthcare operators have been acquired for in recent years.

At RM2.27 apiece, KPJ shares are trading at an EV/Ebitda of 14.14 times, with an EV of RM12.84 billion.

“While its current valuation may seem steep, we believe it is fair,” RHB Research said in its Nov 26, 2024, note, pointing to investors’ enhanced appetite for high-quality healthcare assets. “Our new TP also implies 2025F EV/Ebitda of 19 times, against its five-year historical average of 12 times. KPJ’s valuation deserves a premium due to its solid turnaround story [there is room for margins to widen from hospitals under gestation].

“Meanwhile, investors’ growing appetite for the healthcare sector should lead to a valuation rerating for healthcare players — in tandem with Sunway Healthcare Group’s possible listing in the medium term.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Thirteen stocks see short-selling suspension amid market sell-off

- Market plunge drags FBM KLCI down over 5%, as East Asian markets sink on trade war concerns

- Are investors cutting losses on Genting Malaysia?

- China has already trade-war-proofed its economy

- Stocks plunge on tariff turmoil, markets bet on rapid US rate cuts

- Philippines mulls cutting tariffs on US products, says trade chief

- China holds military drills at newly expanded Cambodian naval base

- Gas Malaysia says more areas to face gas supply disruption after Putra Heights blaze

- FBM KLCI down 4.01% to 1,443.80 on April 7, 2025

- Marine & General to buy petroleum product tanker for RM55m from Muhibbah Engineering unit