This article first appeared in Capital, The Edge Malaysia Weekly on March 31, 2025 - April 6, 2025

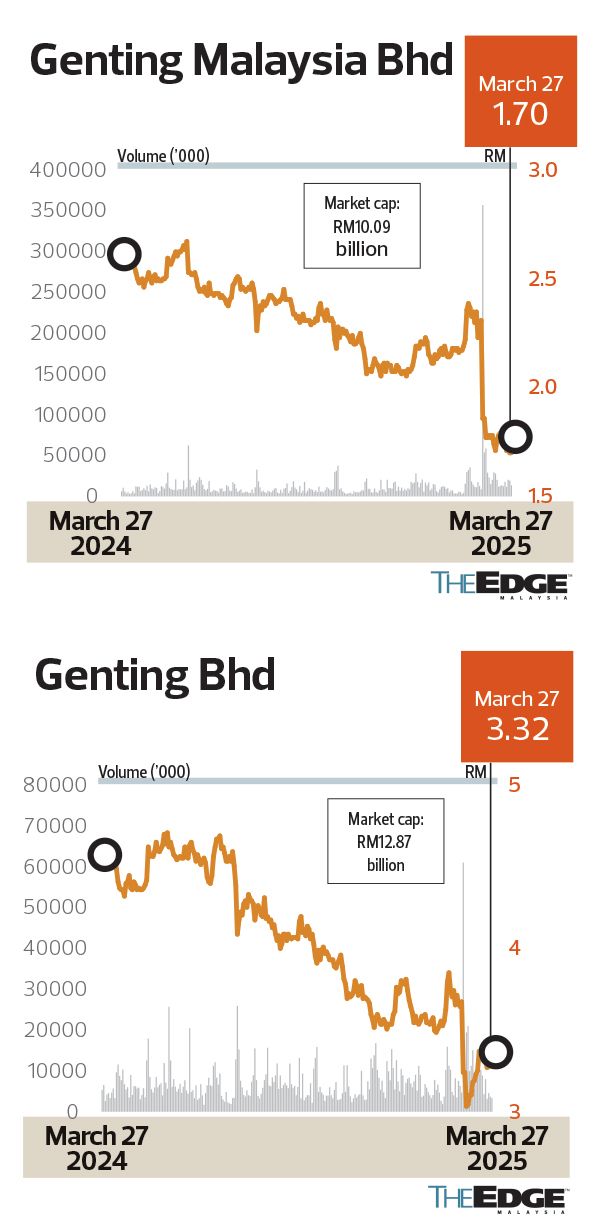

ONCE a darling of the Malaysian stock market, investors appear to be cashing out of Genting Malaysia Bhd (KL:GENM), following disappointing earnings, rising debt and lack of convincing prospects, pushing shares of the casino and resort operator to their lowest in five years.

Genting Malaysia stock has fallen 34.71% over the past one year to close at RM1.70 on Thursday, a level last seen in November 2020 during the Covid-19 pandemic. Its parent company Genting Bhd (KL:GENTING) has not fared much better, sliding 27.55% over the past year to RM3.32. Over in Singapore, sister company Genting Singapore Ltd has been hit less than half as much, having lost 11.09% to settle at 75.5 Singapore cents.

Analysts, once bullish on the group, have turned cautious, with some slashing their earnings projections. At least six have downgraded their recommendation for Genting Malaysia, following weaker-than-expected FY2024 results — in stark contrast to the start of last year. At the time, the street was optimistic, forecasting a doubling of profit in FY2024, and projecting the casino operator would be one of the strongest performers among the benchmark KLCI constituents.

Instead, both Genting and Genting Malaysia were removed from the FBM KLCI at the end of last year, signalling a loss of prominence, as funds tracking the key index were forced to sell their holdings. This put further pressure on the share prices of both companies.

Earnings miss, downgrades follow

Genting Malaysia posted a net profit of RM251.28 million for the financial year ended Dec 31, 2024 (FY2024), down 42.5% year on year from RM436.79 million. The results fell far short of consensus expectations, prompting several brokerages to adjust their ratings and trim target prices.

The stock currently has five “buy” calls, nine “hold” ratings and three “sell” calls. Even so, the consensus 12-month target price of RM2.48 implies a potential upside of 45% from its current level.

The announcement of a reduced dividend per share of 10 sen for the year, down from 15 sen in FY2023, surprised many. Analysts suggest this move is part of a strategy to conserve cash for potential expansion projects.

“We understand that dividends were cut to prepare to expand but fear that investors will not take it kindly,” Maybank Investment Bank Bhd wrote in a Feb 28 note, following the results announcement.

Among the projects on the table is the expansion of Resorts World New York City, which could require an investment of US$5 billion (RM22.32 billion) should Genting Malaysia secure a downstate casino licence. At the same time, a potential move into Thailand’s gaming market could demand another US$3 billion in capital expenditure.

“While we acknowledge the group’s need to preserve capital and manage gearing, we assess that this [dividend cut] may hurt capital returns and sentiment, particularly for yield-oriented investors, thus resulting in share price retracement,” UOB Kay Hian Securities (M) Sdn Bhd concurs.

Parent company Genting has also faced headwinds. It posted a net loss of RM169.38 million for the fourth quarter ended Dec 31, 2024 (4QFY2024) — its first quarterly loss in two years — compared to a net profit of RM150.99 million a year ago.

For the full year, Genting’s net profit dropped 4.98% to RM882.95 million despite a marginal 2.21% increase in revenue to RM27.72 billion.

Despite these setbacks, analysts remain relatively upbeat about Genting’s long-term prospects, particularly as global tourism recovers. Of the 15 analysts covering the stock, 12 maintained “buy” calls, while three have “hold” ratings and no “sell” calls. The consensus target price is RM4.78, implying a 45% upside potential from current levels.

Debt weighs on expansion hopes

While Genting Singapore stands out with its cash-rich position of S$3.6 billion (RM11.9 billion) and virtually no debt, its Malaysian counterpart is heavily leveraged.

Genting Malaysia’s total borrowings amounted to RM12.22 billion as at Dec 31, 2024, more than 60% of which are denominated in US dollars. The company spent US$4.3 billion in 2021 to develop Resorts World Las Vegas, making it the most expensive integrated resort built on The Strip.

High debt levels mean Genting Malaysia is more vulnerable to interest rate and foreign exchange fluctuations, and its ability to fund large-scale projects could be constrained if earnings do not improve.

Investors, already wary of its recent earnings shortfall, may remain on the sidelines until there is greater clarity on the company’s expansion plans.

Despite its inexpensive valuation, Phillip Capital Research says Genting Malaysia risks remaining a value trap — a seemingly undervalued stock that appears cheap based on valuation metrics but lacks strong growth prospects — unless a major catalyst emerges.

The research firm says that without any major catalyst — such as securing a New York City downstate casino licence — margin pressure, associate losses and rising depreciation charges are likely to cap earnings upside. “Key downside risks include lower-than-expected win rates, potential hikes in gaming taxes and drag from key associates. Upside risks include favourable luck factors, as well as improved visitor spending and gaming appetite,” it adds.

In a rare move, Genting executive chairman Tan Sri Lim Kok Thay and his family stepped in to purchase battered Genting shares for the first time in nearly four years.

Over the past month, they have acquired more than 27.66 million shares, with Lim’s private investment arm, Kien Huat Realty Sdn Bhd, purchasing more than 26.4 million shares. Separately, his son, Keong Hui, bought 1.26 million shares. As at March 24, Lim’s deemed interest in Genting stood at 44.7%.

Analysts view the purchases as a strong show of confidence in Genting’s long-term prospects, especially following the stock’s steep decline.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- All Malaysia-based carriers failed to meet international punctuality target in January — Mavcom

- EU races to expand €2 tril trade network as US links sour

- What Samsung and Vietnam stand to lose in Trump's tariff war

- Trump's trade team chases 90 deals in 90 days. Experts say good luck with that

- US tariffs risk straining Malaysia-China ties, Anwar warns

- Aaron-Wooi Yik trounce defending champions, edge closer to first BAC title

- Amanah confident in helping to secure 5 voting districts in Ayer Kuning state by-election

- Russia's Lavrov praises Trump's understanding of Ukraine conflict

- Trump exempts phones, computers, chips from ‘reciprocal’ tariffs

- Fed’s deepest tariff fear is a price shock that won’t fade away