(Photo by Zahid Izzani/The Edge)

This article first appeared in The Edge Malaysia Weekly on December 9, 2024 - December 15, 2024

UEM Group Bhd, the wholly-owned infrastructure arm of Khazanah Nasional Bhd, has been silent for a long time.

Some in the diversified group say the last time it gave an interview to the media was when Datuk Mohd Izzaddin Idris was at the helm. He left in October 2018, after holding the reins for nine years.

The long silence should not be mistaken for inactivity though. “In a way we’ve been like, for lack of a better term, a sleeping giant,” says managing director Datuk Amran Hafiz Affifudin.

“But it’s not as if nothing was happening [at UEM Group]. A lot of things were happening behind the scenes. It was more of preparing the ground. I think the board and management of UEM Group were focusing on improving efficiency. The philosophy was what they called ‘S&O’ — strategy and oversight. Now we’ve moved away from that.”

This is his first interview since being appointed to the top position at the group slightly more than four months ago. “It’s been only 119 days, to be exact, since I was appointed managing director of UEM Group,” says a jovial Amran Hafiz, former executive director and head of asset development at Khazanah. He was overseeing the sovereign wealth fund’s domestic investments.

Changes in the pipeline

While he comes across as light-hearted and has a pleasant personality, it becomes clear that the responsibilities that Amran Hafiz has been tasked with are enormous.

“UEM Group is one of the nation’s builders. The group literally built the nation. This is not something metaphorical or something that is just nice to say, but we literally built the highways, bridges, buildings. So, it’s very important that we preserve the good legacy and enhance it,” he says.

For starters, some of the more prominent companies under the UEM Group banner are cement manufacturer Cement Industries Malaysia Bhd (CIMA), construction company UEM Builders Bhd, highway operator PLUS Malaysia Bhd, renewable energy and waste management outfit UEM Lestra Bhd, 69.56%-owned property developer UEM Sunrise Bhd (KL:UEMS) and 69.14%-owned UEM Edgenta Bhd (KL:EDGENTA), which is in healthcare support services and property and facility solutions.

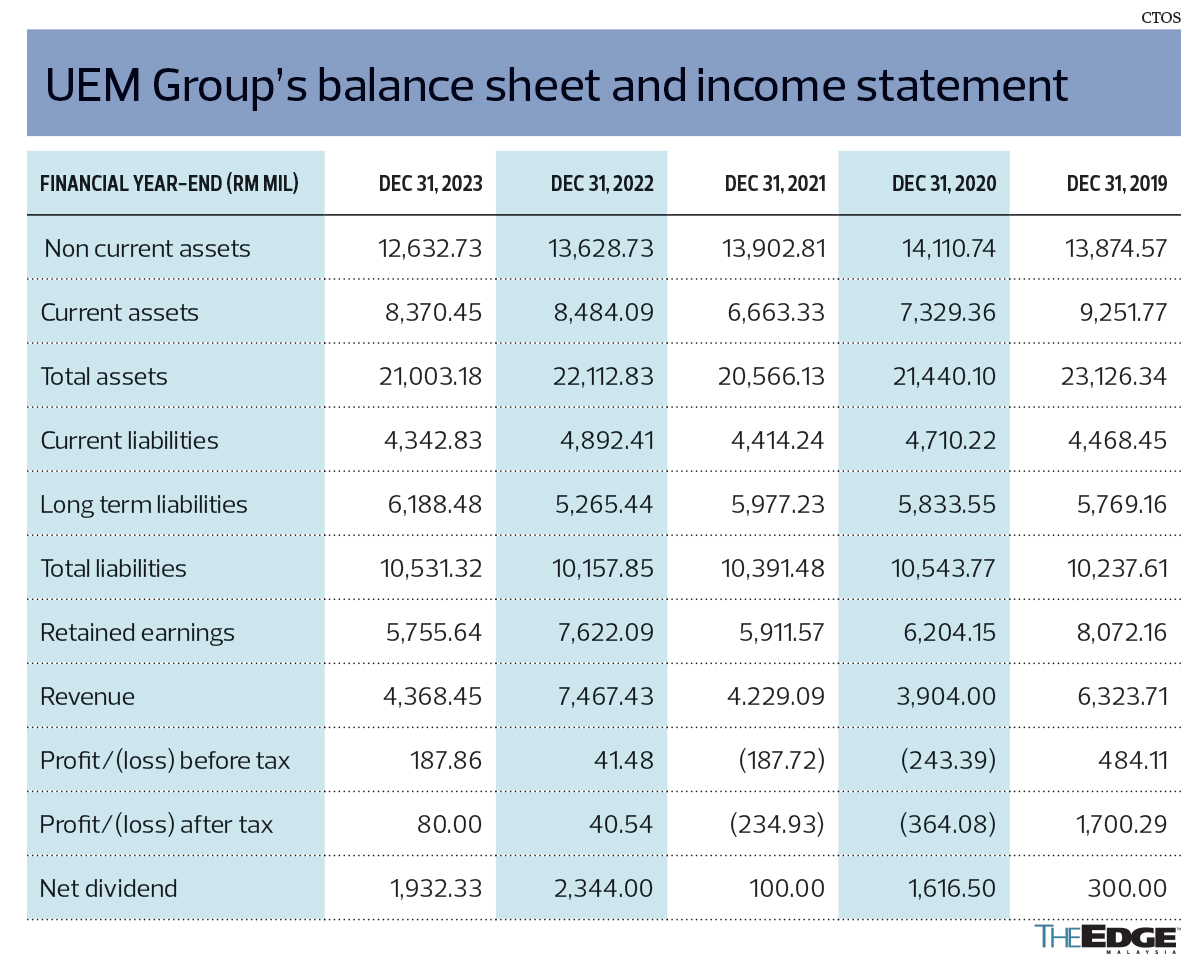

To put things in perspective, for its financial year ended Dec 31, 2023, UEM Group chalked up an after-tax profit of RM80 million on revenue of RM4.37 billion. In FY2022, it mustered an after-tax profit of RM40.5 million from RM7.47 billion in revenue.

As at end-2023, it had total assets of RM21 billion and total liabilities of RM10.53 billion, while its retained earnings stood at RM5.75 billion.

There are aggressive plans being put in place for UEM Group to morph into a larger entity. Amran Hafiz paints a picture of where he sees the group in five years.

“For the companies like CIMA, [we are looking at] improvement in terms of returns, valuations, how they service the people. For UEM Lestra, we’re going to be a serious energy player in the country. [Now,] we are like a small mosquito. We’re not even comparable to Malakoff [Corp Bhd] (KL:MALAKOF) right now, but it’s okay. We start small, but we are very confident that we can get to a better level in five years,” he says.

“Overall, for UEM Group, we hope to double our NAV (net asset value) and triple our revenue in five years. We also hope to have an average ROE (return on equity) of more than 5% … It’s not an easy job, but we didn’t sign on to do an easy job. That’s the challenge. It’s not like we have teh tarik at 4pm [and take things easy].

“Our [annual] revenue is about RM4 billion. So, we are going to do RM12 billion to RM14 billion, and this is excluding Malaysia Airports [Holdings Bhd] (KL:AIRPORT), which is an associate company. Our NAV is about RM5 billion. We hope to get about RM11 billion in five years.”

These huge improvements will come from new verticals, or businesses, probably in sustainable industries, as well as the company’s existing businesses. “We have to align ourselves with what the country wants, to help the government in pushing the green agenda, and also possible corporate movements within our current portfolio,” says Amran Hafiz.

Much of these new verticals and improvements will come as a result of UEM Group’s capital expenditure (capex) for the next five years, pegged at a whopping RM7 billion — RM1.5 billion of which has been earmarked for UEM Lestra.

The funds for the capex are already in place. In July last year, UEM Group issued a RM7 billion sukuk wakalah programme through wholly-owned vehicle UEM Olive Capital Bhd.

Last week, RAM Ratings affirmed an AA1(s)/Stable rating for the bonds, on expectations that UEM Group would “continue to enjoy a ‘high’ likelihood of extraordinary support from its parent, Khazanah”, taking into consideration the group’s designated role as Khazanah’s infrastructure and green investment arm.

The rating agency added: “UEM Group’s standalone credit profile remains anchored by its diversified business profile and leading market positions of its operating entities in the property, cement, asset and facility management, and airport operation sectors.

“Its adjusted consolidated operating cash-flow debt coverage (excluding concession-related debts) was largely unchanged at 0.1 times last year (FY2022: 0.11 times). The ratio is expected to strengthen on the back of better earnings prospects for the group’s property, cement and asset and facility management operations.”

With the funds in place, UEM Group’s corporate moves should be worth watching. Some of its forays point to the direction in which it is looking to expand its business empire.

In January, the group inked a deal with Itramas Corp Sdn Bhd and Hexa Renewables Malaysia Sdn Bhd for a 1gw hybrid solar photovoltaic energy transition project. The development includes a 500mw hybrid solar plant in Johor.

Meanwhile, UEM Lestra inked an agreement with Hexa Renewables to form 51:49 joint venture Lestra Hexa JV Sdn Bhd. Hexa Renewables has secured a technical partnership agreement with Itramas for the latter to provide technical services. Itramas is Malaysia’s largest vertically integrated solar plant developer and service provider; and Hexa Renewables, a portfolio company of US-based I Squared Capital, is involved in the solar and wind project development space.

The signing of the agreements came after sovereign wealth fund Khazanah — named the champion of a large-scale integrated Renewable Energy Zone under the National Energy Transition Roadmap (NETR) — identified UEM as its green investment vehicle.

Eyebrows were raised, however, when UEM Group was given the opportunity to build a 500mw solar farm.

Asked why he thinks the group should be selected for the 1gw project, Amran Hafiz says: “I guess [UEM Group] is perceived to be rather new to renewable energy, even the energy industry. But why [should UEM Group not get the job]? It’s still within infrastructure.

“The new vertical is decarbonisation and renewable — it is within Khazanah’s portfolio. So, it’s not new to us; we have synergy. We are currently [partnering with Itramas] in the solar business. It is the largest biogas company in the country. So, it’s not as if we are starting from zero.

“The talent and the experience are there, maybe not in solar, and not on the scale of 1gw, but that’s why we work with partners. So, we can’t understand why people say, ‘Why UEM?’”

Corporate exercises to look out for

Several corporate exercises involving some of the company’s subsidiaries have been lined up, but UEM Builders will not be in the thick of action.

There have been murmurs that UEM Group is mulling over a privatisation of UEM Edgenta, but Amran Hafiz neither confirms nor denies the plan (see “Depressed valuation sparks speculation about UEM Edgenta”).

Asked for a response, he offers: “We don’t rule out anything, but I cannot comment on specific transactions.”

In November last year, UEM Group undertook a process to divest CIMA and went as far as shortlisting seven candidates, according to news reports, but the sale was called off in March this year.

The market scuttlebutt now has it that UEM Group is looking to sell a strategic stake but retain control of the company.

Amran Hafiz says, “We did try to dispose of CIMA but we decided to keep it for now. Right now, CIMA is an important part of our portfolio. It’s doing very well financially and operationally.”

On whether there is a stake sale in the pipeline, he merely says, “We are open [to it], to be honest.” Asked whether talks were ongoing, he says, “I cannot say for sure, but we are always open to looking at strategic partners. One thing I have to say is that CIMA will always remain under the control of the UEM Group.

“If you’re talking about a partial sale, a potential collaboration or even acquisition, they’re all open. That’s not just for CIMA but all our companies.”

UEM Group’s largest asset is its 51% stake in PLUS, which was the subject of much corporate wrangling in 2019. The government decided to leave it with UEM Group and the Employees Provident Fund, which holds the remaining 49% equity interest. It remains to be seen whether there will be any developments in the highway operator, as Amran Hafiz says things are challenging (see “PLUS’ concession not as lucrative as perceived, says UEM Group MD” on Page 60).

UEM Group is now looking at winding down UEM Builders’ operations. The last significant construction job that it undertook was the building of the mega skyscraper Merdeka 118, which at 679m is the world’s second-tallest building. Construction of the skyscraper started in 2014 and is largely completed.

Amran Hafiz says, “In 2014, the board of UEM Group already decided we no longer wanted to be in the construction business. But it’s not as if we’re exiting [completely]. We are still in the value chain of construction. Opus [Group Bhd, wholly-owned by UEM Edgenta] is still there. We do design, engineering, PMC (project management consultancy). It is where the legacy of our involvement in the construction sector remains now … But in terms of actual construction, Merdeka 118 will be the last one.”

Explaining the exit, he says: “It’s not a very attractive industry. We looked at the return on capital, and I think the judgement was made that based on this and other factors, we decided it was probably not an industry that we wanted to continue to be in.”

Another often-talked-about asset of UEM Group is developer UEM Sunrise.

Jumping on the industrial park bandwagon

Now and then, whenever Johor — the southernmost state in Malaysia — gains traction (whether for the Shenzhen-Hong Kong comparison, developments in the Iskandar Malaysia region, or the current data centre enthusiasm), developer UEM Sunrise is usually touted as a likely beneficiary.

Other than the sale of some parcels of land and sporadic projects, however, the developer has yet to monetise the jewel in its crown — some 8,000 acres in Johor, largely in Iskandar Puteri, Desaru and Kulai.

Amran Hafiz says, “In Johor, we are one of the largest landowners. So, the challenges there are like, what are we going to do about it?

“UEM Sunrise, which is huge, used to trade at roughly 80% discount to NAV. Right now, it’s better, but it’s always trading at a discount. So, again, we decided, ‘Okay, what can we do to enhance the price?’ We’re looking at focusing on industrial parks.”

To this end, UEM Sunrise, Itramas and China Machinery Engineering Corp formed a strategic partnership in May to develop a Renewable Energy Industrial Park on a 40-acre parcel in Gerbang Nusajaya in Iskandar Puteri, Johor.

Despite the potential of its Johor land bank, UEM Sunrise’s share price remains depressed. Last Friday, the stock ended trading at 97.5 sen, translating into a market capitalisation of RM4.98 billion.

For the nine months ended Sept 30, UEM Sunrise posted a net profit of RM50.01 million on the back of RM799.51 million in revenue. For the corresponding period a year ago, it made a net profit of RM48.39 million from RM917.09 million in revenue. At end-September, the company’s net assets per share was pegged at RM1.34, which means its shares are trading at a 26% discount to its net assets per share.

Amran Hafiz says, “UEM Sunrise and UEM Group have always wanted to monetise the Johor land bank, but it [also] depends on external factors, [such as] the market. We believe that this time around, with the focus on Johor and the [Johor-Singapore Special Economic Zone], a key factor that … is a needle mover, a game changer is the RTS (Rapid Transit System), which is going to come in 2027.

“Right now, the cost of doing business and the cost of living in Singapore have increased tremendously. That’s an ingredient for Johor to be more attractive, especially in this kind of business, because of its location.”

Only time will tell whether UEM Sunrise and the larger UEM Group finally make hay while the sun shines and monetise the land bank in Johor.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Global funds hit pause on Indonesia after Prabowo policy changes

- Embattled billionaire Ong Beng Seng to step down from Hotel Properties

- Trump warns tariffs coming for electronics after reprieve

- Jentayu signs 40-year power purchase agreement for RM2.8b 162MW Sabah hydropower project

- Singapore eases monetary policy as expected, sees weaker growth in 2025

- Goldman Sachs warns oil faces ‘large surpluses’ through 2026

- China’s stock rescue in full swing as ETF inflows hit record

- Knight Frank survey indicates optimism for Malaysia’s commercial sector this year

- The State of the Nation: US’ trade deficit-based ‘reciprocal’ tariffs set to test fiscal and monetary policy space

- Thailand finalises US trade strategy ahead of talks next week