This article first appeared in The Edge Malaysia Weekly on April 7, 2025 - April 13, 2025

THE dreaded next test to a country’s fiscal and monetary space post-pandemic may well be looming as US President Donald Trump’s sweeping “Rose Garden” tariffs stoke up fears of a global recession happening to as high as 60%.

“The Asean economies we cover were hard hit by tariffs, as we had expected, but the magnitude of the hit is much larger than we saw. This is partly based on the US computation of the tariffs imposed on it by trading nations, resulting in hefty tariff rates and subsequently discounted differential tariffs. Both are dramatic in their magnitude. These will have implications for growth, inflation, fiscal and monetary policies,” OCBC Bank head of research and strategy Selena Ling told clients on April 3, trimming gross domestic product (GDP) forecasts for Asean-6 economies by as much as 1.2 percentage points (ppt) to 5% for Vietnam, but only by 0.2ppt to 4.5% for Malaysia.

That seasoned economists are not waiting two weeks for first-quarter advance gross GDP release before trimming their economic growth forecast to 4% and near it — below Malaysia’s official range of 4.5% to 5.5% for 2025 — attests to the potential carnage from the US trade deficit-based reciprocal tariffs on economic growth for export-centric economies, including Malaysia.

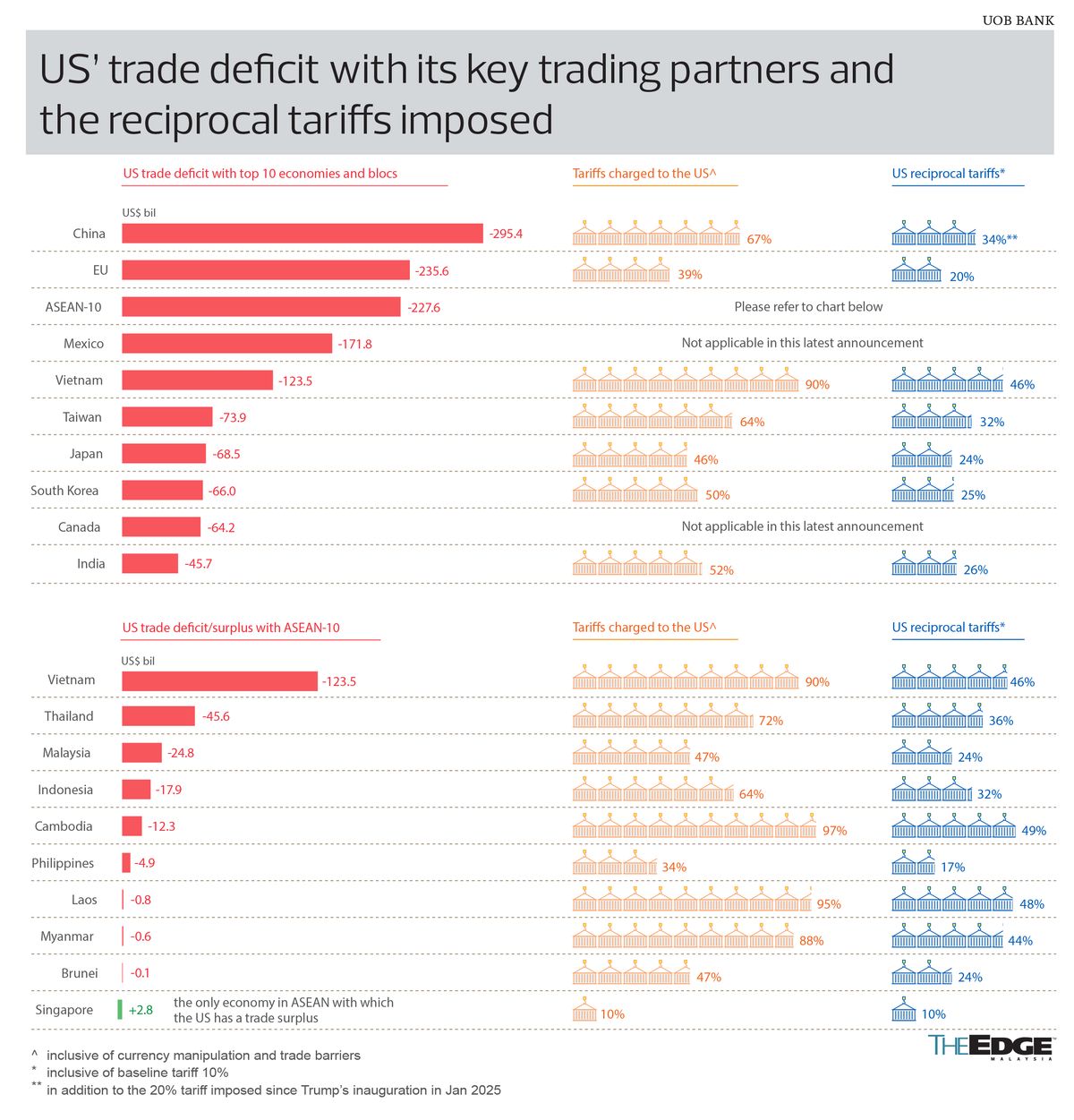

Similarly, forecasters did not wait even two days to trim growth expectations for Vietnam, for which advance 1Q GDP data is out on Sunday (April 6) and which was also looking at 8% GDP growth but had been slapped with 46% reciprocal tariffs — nearly twice as high as the 24% for Malaysia. Both countries were seen to be among leading beneficiaries of the China+1 strategy of multinational corporations (MNCs) diversifying their manufacturing base outside China to the neutral Asean region amid escalating US-China tensions.

“The China+1 story is not dead, but the reciprocal tariffs will likely disrupt and slow the reconfiguration of supply chains to Asean. The Asean-China tariff gap remains wide but has narrowed with the reciprocal tariffs, especially for Vietnam and Thailand. China will face an effective US tariff rate of 66%, by our estimates, with the reciprocal tariff rate of 34% added to the recent 20% additional [alleged fentanyl] tariff and 12% tariffs under Trump’s 1.0 trade war. MNCs may pause on fresh FDI [foreign direct investments], given the uncertainty over trade policies, broader trade war and excess capacity displaced by the US tariff wall,” says Chua Hak Bin, regional thematic macroeconomist at Maybank Investment Banking Group in Singapore.

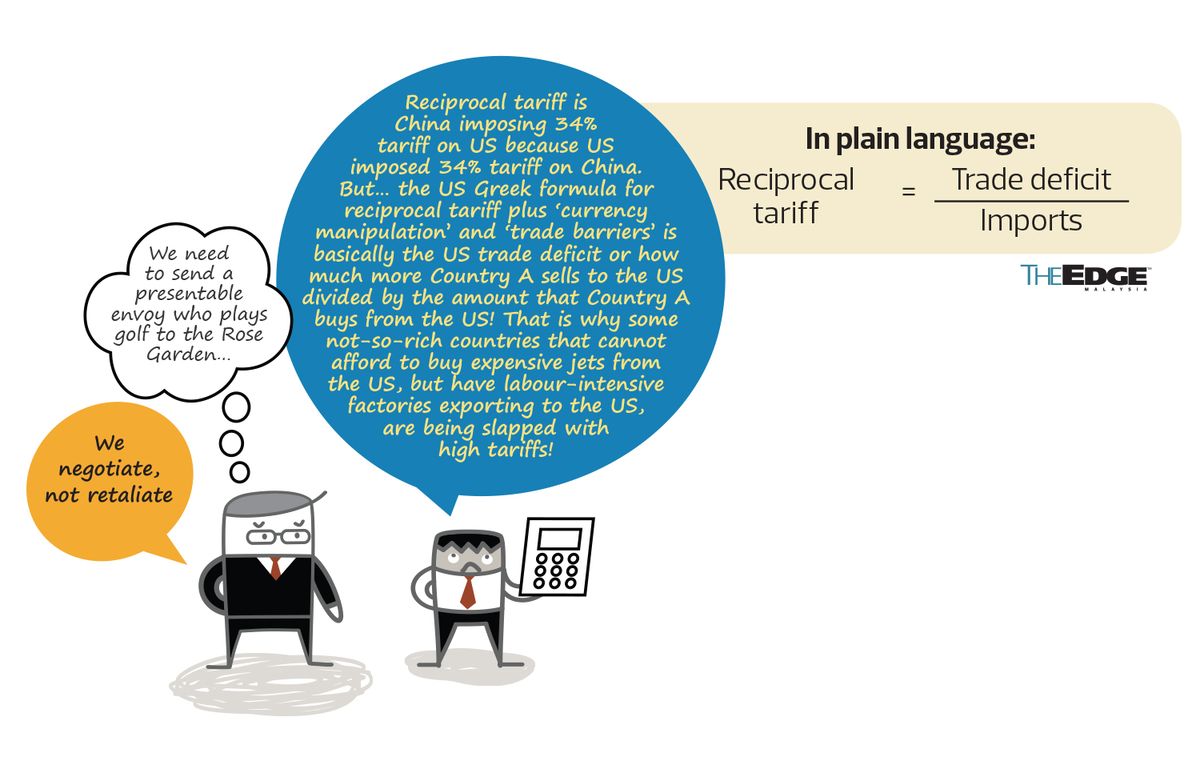

While noting Malaysia’s “negotiate not retaliate” stance should prevent an escalation with the US, Maybank shaved its GDP growth forecast for Malaysia by 60 basis points (bps) to 4.3% from 4.9% for 2025 but revised 2026 GDP forecasts higher to 4.6% from 4%. Malaysia, it reckons, should have “some buffers” by incentivising investments into energy transition, economic complexity in technology sectors and the Johor-Singapore Special Economic Zone (JS-SEZ).

Among the Asean-6 countries, Chua says GDP growth downgrades are more modest for Thailand (-0.3%ppt to 2.3%), Indonesia (-0.3%ppt to 4.7%) and the Philippines (-0.2%ppt to 5.8%) but larger for Vietnam (-1%ppt to 5.9%), Malaysia (-0.6%ppt to 4.3%) and Singapore (-0.5%ppt to 2.1%), “given their heavier reliance on trade and the higher reciprocal tariffs on Vietnam”.

“Risks remain to the downside if the global trade war broadens and intensifies, as some countries (EU, China) are planning retaliatory tariffs. The US has not finalised a decision on a potential 25% tariff on semiconductors — which could impact Malaysia and Singapore — and on pharmaceuticals — which could impact Singapore,” Chua wrote in a note dated April 3, trimming the inflation forecast for Asean-6 to 2.1% in 2025 (from 2.4%) and 2.1% in 2026 (from 2.5%) as price pressures ease on the back of slowing global growth and displacement of excess capacity, particularly from China.

The US Federal Reserve rate cuts, pencilled in at 50bps in 2025, and lower Asean inflation “will open the door for more Asean central banks to ease, including Indonesia (-50bps), Philippines (-50bps), Thailand (-50bps), Vietnam (-25bps) and Singapore [which uses currency strength against inflation] in 2025”, writes Chua.

OCBC’s Ling also expects regional central banks “to become more supportive of growth, particularly in the second half of 2025”.

“We are adding rate cuts to our Vietnam, Thailand, Indonesia and India forecasts. We expect the State Bank of Vietnam and Bank of Thailand to cut by an additional 50bps in 2H25, while Bank Indonesia and Reserve Bank of India will likely cut by an additional 25bps on top of our current forecast of 25bps. This implies an additional 50bps in rate cuts by end-2025. Although the growth impact is limited for Bangko Sentral ng Pilipinas (BSP), we expect it will take the opportunity to lower rates further to mitigate downside risks. We, therefore, expect a cumulative 50bps in rate cuts in 2025,” Ling wrote in a note dated April 3, which kept forecast for Malaysia’s overnight policy rate (OPR) at 3% in 2025 but noted “rising risk of a rate cut in 2H2025”.

Cut or preserve monetary space

Will Bank Negara Malaysia also trim its OPR from the current 3%? Not necessarily, but economists are seeing greater odds of this happening.

“We tweaked our forecast from the outlook of OPR remaining stable at 3% to a forecast range of 2.75% to 3% for both end-2025 and end-2026. This outlook takes note of the challenge facing Bank Negara’s monetary policy to strike a balance between its dual mandates of sustainable growth and price stability amid the downside bias to economic growth largely due to external factors — namely the potential fallout from US trade and tariff policies under Trump 2.0 — and the upside risk to inflation mainly due to the aforementioned domestic policy factors,” said Maybank economists, led by group chief economist Suhaimi Ilias, in a separate note dated April 4, which noted that the US’ estimate of the tariff charged by Malaysia on the US of 47% “happens to be equal to the ratio of US trade deficit value with Malaysia (2024: US$24.8 billion) to US value of total imports from Malaysia (2024: US$52.5 billion)”.

Meanwhile, UOB Bank Malaysia’s senior economist Julia Goh, who trimmed her 2025 GDP forecast for Malaysia to 4% from 4.7%, still sees Bank Negara “maintaining the OPR at 3% for now”.

“We think Bank Negara will still wait for details on fuel subsidies and also watch the impact of tariffs and outcome of negotiations. At this point, Malaysia has some leverages — domestic demand, diversion of flows, fiscal support, national master plans, a diversified economy and export base [even though] there is caution on how tariffs affect key trading partners, which will have spillover effects on Malaysia,” Goh tells The Edge, expecting exports to slow to 3.8% in 2025, down from 4.5% previously.

Asked about the potential of a 25bps OPR cut in 2025, Goh sees “increasing odds” for an interest rate cut in 2H2025 should global risks intensify.

But, for now, Goh reckons it may be “better to preserve that policy space if your economy is still expanding at above 4%, even if it is not as high as before”.

“The implication [of US tariffs] on Malaysia’s consumer price inflation is expected to be minor with supply-driven factors and potential excess supply dumping activities neutralising the effects,” she says.

Foreign exchange experts at Maybank maintain their forecast of “near-term softness” in the ringgit against the US dollar at 4.60 for end-2Q 2025 but see the ringgit ending firmer against the greenback at 4.35 by year-end and 4.20 in 2026.

Forex experts at UOB Bank see the Chinese yuan leading “the anticipated weakening of Asia FX and we forecast USDCNY rising to 7.80 by 3Q2025”. Concurrently, against the US dollar, UOB sees the Singapore dollar easing to 1.39, the ringgit to 4.70, Indonesia’s rupiah to 17,200, Thai baht to 26 and the Vietnamese dong to 27,200 by September.

Flexibility on fiscal stimulus

In reference to the Asean-6 fiscal and monetary policy flexibility, Maybank’s Chua reckons that fiscal stimulus “may be more limited given the higher public debt and deficit positions, with the exception of Singapore”.

As the impact of US tariffs reverberates across Asia, HSBC chief Asia economist and co-head of Global Research Asia Frederic Neumann is watching closely for policy action across the region.

“The US tariff announcements have made clear the necessity for greater internal resilience and policy support. In the near term, the chances of significant policy easing have gone up, with central banks likely prioritising growth over other considerations, such as inflation and even exchange rates. More important, however, will be fiscal stimulus, with swift, additional disbursement needed to cushion demand, not least because a loosening in monetary policy may not trigger an immediate capex or spending rebound as business and household confidence is subdued,” says Neumann, who sees US tariffs affecting up to 5% of Vietnam’s GDP given its exposure to the US market although actual impact “is bound to be considerably lower” as the door for negotiations “remains so slightly ajar”.

The potential impact of US tariffs is estimated at just under 1% of GDP for Malaysia, according to data appended in HSBC’s note dated April 3, noting that regional leaders will now need to decide whether they want to retaliate against US tariffs or negotiate with Washington.

Indeed, on April 4, China’s official Xinhua News Agency reported that Beijing will impose a 34% tariff on all imports from the US starting April 10, right after the US’ reciprocal tariffs kick in on April 9 (baseline 10% tariff starts April 5).

Citing the reprieve to Mexico following trade negotiations, HSBC’s Asean economist Yun Liu is watching out for the outcome of Malaysia’s engagement efforts with the US.

“While semiconductors are exempted from today’s tariff announcements, uncertainty is set to persist. After all, Malaysia’s semiconductor exports to the US are the largest magnitude in Asean, accounting for around 4% of Malaysia’s GDP,” she says.

Harnessing Asean’s collective might

Professor Ong Kian Ming, pro vice-chancellor for external engagement at Taylor’s University and former deputy minister of international trade and industry, expects global FDI flows to “ramp down significantly in 2025 as companies update their investment strategies” and calls for the harnessing of Asean’s collective strength.

“Rather than try to negotiate as individual countries with the US, and getting in queue together with many other countries, it would be better for Asean to negotiate with the US as a bloc so that we can put different things on the table to get across the board concessions for the entire region. For example, we can offer critical minerals access and semiconductor supply chain resilience as part of a package to reduce tariffs for all Asean countries. Whether or not this will work is a separate question but it is an option that Asean should be seriously considering, with Malaysia taking the lead as Asean chair,” Ong adds.

UOB’s Goh reckons that stronger regionalisation may help Asean better cope with any trade fallout.

See also "After tariff tantrum, watch out for currency wars" on page 45 and Special Report On Trump Tariffs on page 54

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia’s richest just got wealthier thanks to stronger ringgit — Forbes

- Vista buys Petronas oil stake in US$1.5 bil Argentina deal

- Malaysia Aviation Group posts RM54m earnings for FY2024, its second straight annual profit

- Syed Saddiq trial: Mere receipts insufficient to show funds were young MP's personal monies

- TRX to begin construction of new office tower with PwC Malaysia as anchor tenant, says CEO

- Trump says US Fed chair Powell’s termination can’t come fast enough

- Ancom Nylex sees new production 'very soon' after 3Q drag, proposes dividend in specie

- Sarawak premier dismisses talk of purported interest in AmBank stake, Affin merger

- DBKL given four months to regularise unlicensed traders, says Zaliha

- Former Evergrande CEO says asset disclosure puts him in danger