The office sector sentiment is being shaped by economic conditions, the appeal of prime locations for regional hubs, rental rates, accessibility to public transportation and increasing awareness of ESG (Photo by Patrick Goh/The Edge)

This article first appeared in City & Country, The Edge Malaysia Weekly on April 7, 2025 - April 13, 2025

Following Malaysia’s improved real estate market amid economic growth in 2024, Knight Frank Malaysia expects to enter this year with a cautiously optimistic outlook. The commercial sector, in particular, is predicted to have positive market sentiment underpinned by favourable foreign direct investment (FDI) flows into the country and the resilient economic landscape.

This was discussed in the company’s Malaysia Commercial Real Estate Investment Sentiment Survey 2025. Respondents included representatives of senior management across the Malaysian commercial property industry, namely developers (53%), fund or real estate investment trust managers (38%) and commercial lenders (9%). More than half of the respondents’ commercial real estate projects are located in the Klang Valley (51%), followed by Johor (12%), Penang (10%) and Melaka (9%).

These respondents expressed interest in either exploring or expanding their investments in selected commercial asset classes, including retail outlets, data centres, logistics facilities, serviced suites, hotel or boutique hotels, mixed-use developments, transit-oriented developments, healthcare facilities, senior living, workers’ accommodation, students’ accommodation and school or university campuses.

Non-favourable asset classes include theme parks; meetings, incentives, conferences and exhibitions (MICE); as well as sports facilities or stadiums.

In terms of location, the survey found that the preferred regions for investment or development of financial services were the Klang Valley (37%); Johor (21%); Selangor (14%); Putrajaya and Penang (6% each); Kedah, Melaka, Perak and Sarawak (4% each); Labuan and Sabah (3%); and Pahang (1%).

“The Klang Valley continued to be the leading preference, given its status and role as the national central business district and key economic hub. For Johor, the Johor-Singapore Special Economic Zone and data centre developments are expected to be the key areas of focus, as evidenced by the proliferation of land acquisition activities for data centre developments observed in the state in 2024,” the report adds.

The Malaysian property market experienced steady growth in 2024, registering 311,211 transactions worth RM163 billion, a 6.2% rise in transaction volume and a 14.4% increase in transaction value compared to 2023. The commercial real estate subsector also witnessed positive growth, recording a transaction volume of 33,820 valued at RM36.2 billion, which translates into a 16.6% growth in volume and a 32.7% rise in value.

Predictions on market performance

A large majority of the respondents think the most resilient commercial property types this year will be data centres (24%), followed by industrial or logistics facilities (20%) as well as retail subsectors (12%). Others include mixed-use developments, transit-oriented developments, offices and healthcare facilities.

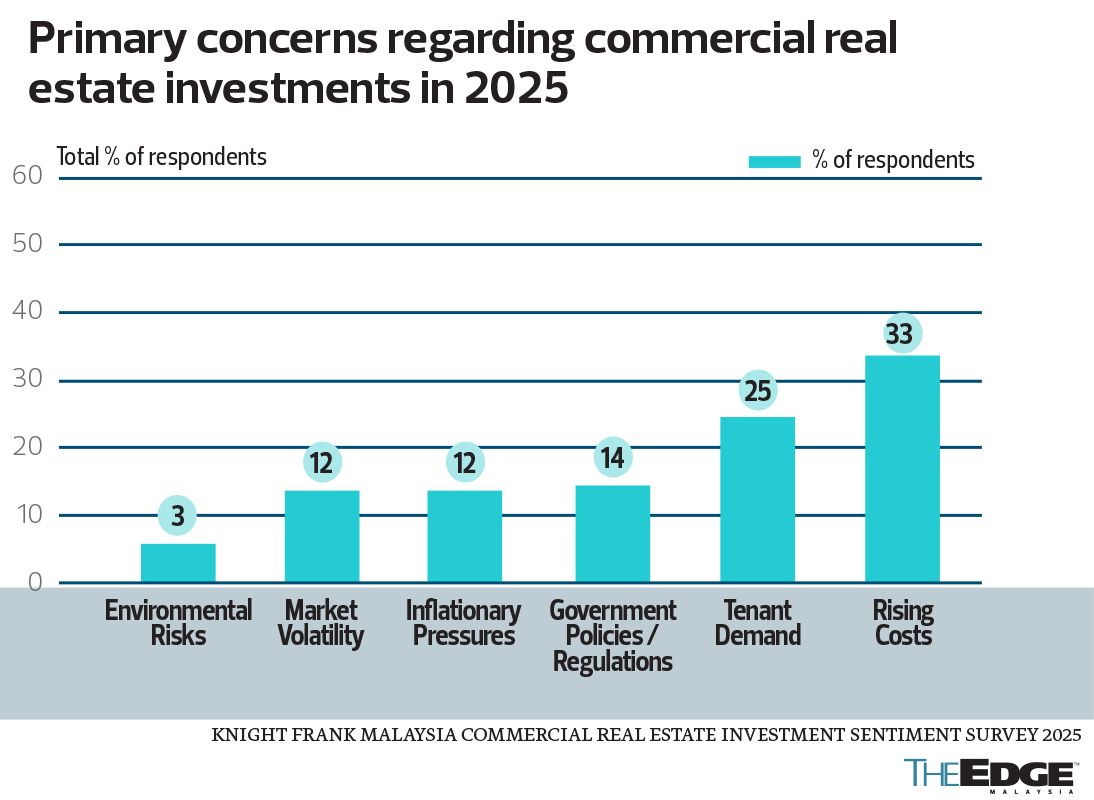

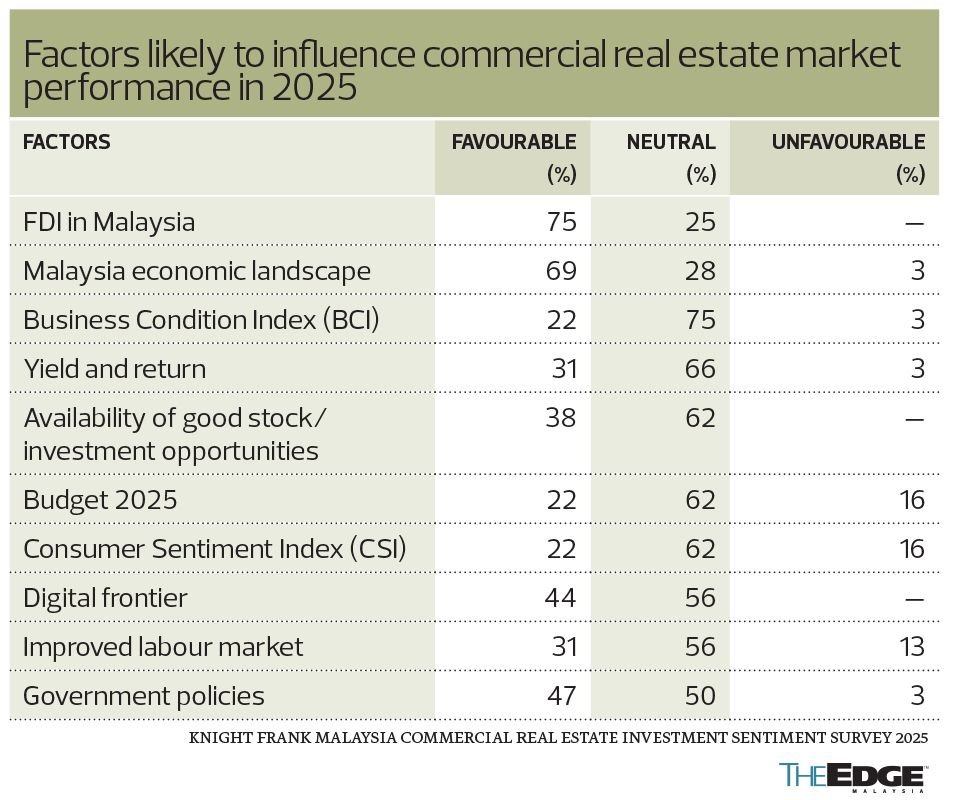

As for factors that are most likely to influence the market this year, the respondents’ top picks were an increase in FDIs and the country’s improving economic landscape.

The report says several factors are expected to influence Malaysia’s commercial real estate market in 2025.

About 60% of respondents anticipate capital appreciation in the industrial and logistics sector in 2025, while 57% share the same outlook for the hospitality sector. In contrast, 71% expect office property values to remain stable, alongside 52% who foresee stability in the retail sector.

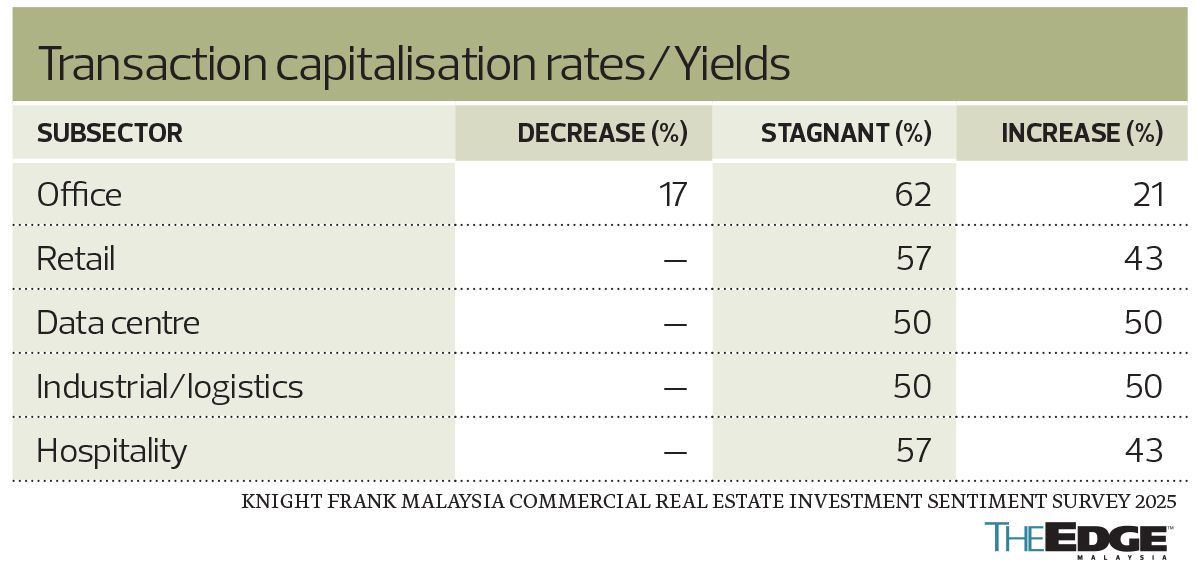

The report also highlights that more than half of the respondents expect capital appreciation rates and yields to remain stable across all selected subsectors in 2025. In the office sector, however, 17% anticipate yield compression due to the oversupply of existing and incoming spaces, which could affect asset performance.

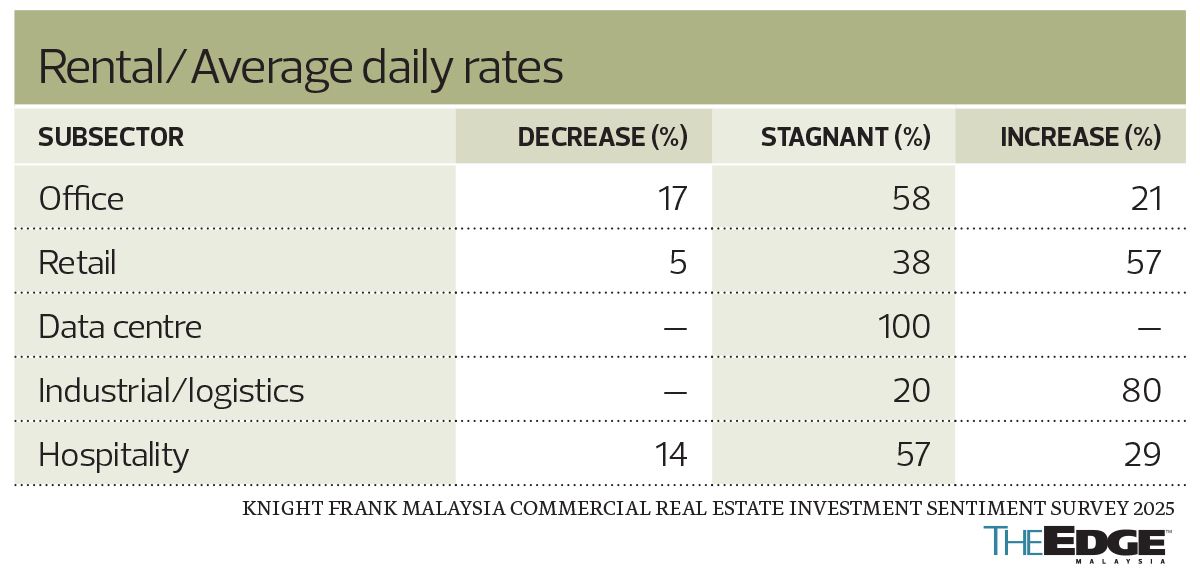

For rental rates, the report says about 80% of respondents are confident that rental rates in the industrial and logistics sector will continue to climb in 2025, driven by strong market activity and rising demand for modern industrial spaces. Similarly, 57% anticipate an increase in retail rental rates, supported by higher consumer spending and a rebound in tourism. In contrast, rental rates for the office and data centre sectors, along with average daily rates in the hospitality sector, are expected to remain stable.

Occupancy rates are also expected to fare better this year, the report points out. About 70% of the respondents say there will be an increase in the industrial and logistics sector, while 57% are anticipating growth in retail occupancy rates. In contrast, occupancy rates for offices (58%) and data centres (100%) are expected to remain stable despite an abundance of existing and incoming supply.

The hospitality sector, on the other hand, presents a mixed outlook, the report says.

“While the rise in tourism activities is expected to positively impact the asset class, the variety of supply options may limit its upward growth, thus [restricting] occupancy rates,” it adds.

Predictions on market sentiment

Besides providing insights for this year’s property market performance, the respondents also have a sense of how market sentiment is going to be for the rest of the year.

In the office sector, overall sentiment is being shaped by Malaysia’s economic conditions, the appeal of prime locations for regional hubs, rental rates, accessibility to public transportation, and increasing awareness of environment, social and governance (ESG) principles.

The report notes, however, that challenges such as workforce availability, oversupply of office spaces, the rise of co-working spaces and continued adoption of hybrid work models pose uncertainties. There seem to be mixed views on shifting workspace preferences and corporate cost-saving strategies, which could lead to office space optimisation and rightsizing trends.

For the data centre sector, strong market sentiment is being driven by Malaysia’s economic outlook, government policies, workforce availability, investment capital and the explosive growth of e-commerce. While infrastructure readiness remains a primary challenge, opportunities lie in the expansion of digital services, increasing land availability and heightened ESG compliance initiatives, the report suggests.

Meanwhile, the outlook on the retail sector, according to the report, is being influenced by economic conditions, government subsidies, employment rates, household income trends and factors such as rental rates, public transport accessibility, tourism activity and evolving consumer shopping preferences.

While consumer sentiment remains a key factor, challenges include the supply of new retail malls, the availability of existing shopping spaces and maintaining occupancy rates. ESG awareness and sustainability initiatives also play an increasing role in shaping retail investment strategies.

The outlook for the industrial and logistics sector this year is being influenced by key factors such as Malaysia’s economic conditions, global commodity prices and government policies playing a pivotal role. The availability of industrial land, labour and FDI will continue to shape the sector’s growth, alongside the expansion of import and export activities.

The report adds that the rise of e-commerce, growth of the electrical and electronics (E&E) and electric vehicle (EV) industries as well as advancements in healthcare and medical technology are expected to drive demand for industrial properties. In addition, warehouse and distribution facility expansions, global supply chain shifts and the impact of the China+1 strategy will further influence the sector.

Challenges such as tariff barriers, funding accessibility, fluctuations in the Industrial Production Index (IPI) and increasing ESG compliance requirements may, however, present hurdles for investors and developers, the report cautions.

Similarly, the hospitality sector’s performance in 2025 will be shaped by Malaysia’s economic conditions, government incentives and promotional efforts such as travel fairs and exhibitions.

The report says the supply of new hotels, occupancy rates, average daily rates and length of stay will be key indicators of market health. Growth in international and domestic tourism, as well as increased business travel, will further support the sector’s recovery.

The availability of existing hotels, rising operational expenses and competition from alternative accommodations such as Airbnb and other shared services would, however, pose challenges for this sector.

ESG still a priority

The report also discussed several key ESG priorities for businesses. These priorities are centred on environmental sustainability, with energy efficiency emerging as the most critical focus, as prioritised by 27% of respondents. This is followed by green building certification (25%).

Other important ESG elements include the use of sustainable building materials (16%) and considerations for location and connectivity (11%). In addition, social impact (10%) and governance and transparency (9%) are recognised as essential components of corporate ESG strategies.

Indoor air quality (1%) and disabled-friendly facilities (1%) ranked lower in priority.

Asked about the importance of ESG in each company’s investment decision-making, 91% of respondents said it was very and somewhat important. Among them, 34% reported that their organisations had fully integrated ESG principles, while the remaining 66% had incorporated selective ESG elements into their decision-making and reporting processes.

According to the respondents, the top three prioritised green initiatives focus on environmental sustainability, aligning with the net zero carbon goals set by the Paris Agreement in 2015, which aims to reduce carbon emissions by 45% by 2030 and achieve net zero by 2050.

In line with this goal, the report says the UK became the first major economy to legislate a net zero emissions law in 2019, while the European Union introduced the Carbon Border Adjustment Mechanism (CBAM), a tariff designed to curb emissions and promote cleaner industrial production.

Reflecting these global efforts, the report highlights that Malaysia is set to introduce its own carbon tax, as outlined in Budget 2025. Expected to take effect in 2026, the tax will initially target the iron, steel and energy industries, encouraging the adoption of low-carbon technologies.

“Revenue from the tax would be used to fund green research and technology programmes. This manifests the country’s commitment and effort in reaching the net zero carbon goal,” the report says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia’s richest just got wealthier thanks to stronger ringgit — Forbes

- Vista buys Petronas oil stake in US$1.5 bil Argentina deal

- TRX to begin construction of new office tower with PwC Malaysia as anchor tenant, says CEO

- Malaysia Aviation Group posts RM54m earnings for FY2024, its second straight annual profit

- Syed Saddiq trial: Mere receipts insufficient to show funds were young MP's personal monies

- Meta Bright to install solar PV systems at Best Fresh Mart outlets

- Renault chairman Senard to step down from Nissan's board

- Urusharta Jamaah ceases to be substantial shareholder in NEXG

- Jointly funded cross-border bridge expected to be completed in 2028, says Nanta in Thailand

- Chinese tea chain Chagee raises US$411m in US IPO