This article first appeared in The Edge Malaysia Weekly on January 10, 2022 - January 16, 2022

EFFECTIVE Jan 1, Bursa Malaysia became the sole approving authority for IPOs on the ACE Market, the second-largest listing platform of the stock exchange and home to 141 public listed companies (PLCs).

Under the new regulatory regime, Bursa is now a one-stop centre for all ACE Market IPO approvals, including the registration of abridged prospectuses for the purpose of secondary fundraising activities via rights issues by corporations listed on the ACE Market.

“The streamlining of the listing process and regulatory framework for the ACE Market is part of the Securities Commission Malaysia’s (SC) initiatives under the five-year Capital Market Masterplan 3 to enhance fundraising efficiency for Malaysian corporations at various stages of growth,” SC chairman Datuk Syed Zaid Albar said in a joint statement with Bursa on Dec 20 last year.

Bursa Malaysia CEO Datuk Muhamad Umar Swift also notes that these new IPO rules will “improve the efficiency and efficacy of the ACE Market IPO process, providing a more facilitative regime for companies that are seeking to list on the exchange”.

So, what do the industry players think about the new regulatory framework? Do they expect more new listings on the sponsor-driven ACE Market?

And given that some LEAP Market-listed companies have been seeking to migrate to the ACE Market, what does the revision of the IPO rules for the latter mean to the former, which are adviser-driven?

Astramina Advisory Sdn Bhd founder and managing director Datin Wong Muh Rong is of the view that the regulators’ latest move is positive and in line with what is already happening regionally.

“In Singapore and Hong Kong, the exchanges are already the one-off agencies for listing and approval processes. Bursa and the SC are probably just catching up with the general processes that are already taking place across the region. This should be the way — both to expedite the process and increase efficiency for our market,” she tells The Edge.

Tradeview Capital Sdn Bhd CEO Ng Zhu Hann points out two schools of thoughts — depending whether one is pro-development for the capital markets or prefers a more conservative stance.

“Personally, I believe that to grow the market and increase its vibrancy, it is necessary to liberalise our capital markets. I welcome this new regulatory change as it helps companies with the intent of listing but are intimidated by the process and regulatory hurdles to have easier access to the capital markets,” he tells The Edge.

“Of course, the flip side would be the concern on potentially lax regulation of new listings without the SC as the gatekeeper. This is a balance that needs to be maintained by Bursa not only as the sole operator of our country’s stock exchange but also as a regulator in its own right,” Ng warns.

Vision Group managing director Chua Zhu Lian opines that the new regulatory framework is a positive initiative to encourage more businesses to go for listing — especially starting on the ACE Market — to increase the vibrancy of the country’s capital markets.

“With better diversity in the market, I believe this will be positive to the trading volume in our stock market, especially among the retailers. In the medium to long run, this will make it easier for Malaysian businesses and entrepreneurs to raise capital at more competitive rates. From an investor standpoint, we can also expect an increase in fee income to Bursa that will be positive for its profitability,” he tells The Edge.

ACE Market gaining traction

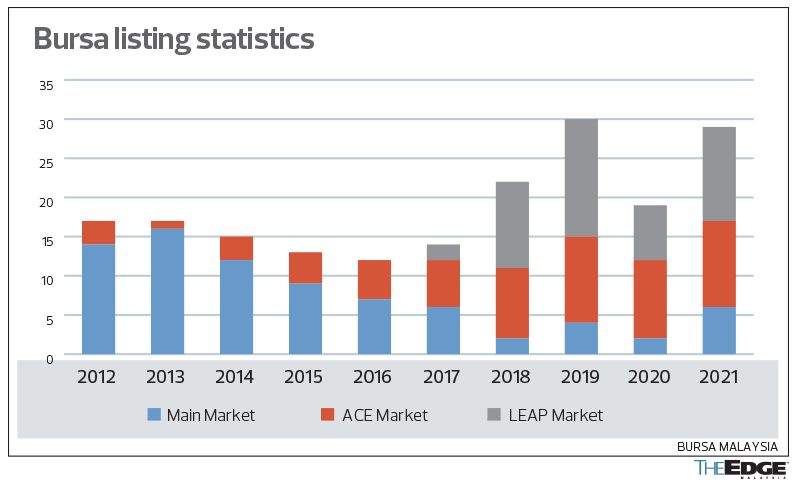

Based on Bursa’s listing statistics, between 2018 and 2021, the number of new listings per year on the ACE Market has been significantly higher than the Main Market (see bar chart). This is in stark contrast to 2009-2016 where it was the reverse.

Why the reversal of trend in recent years?

Astramina’s Wong concedes that many companies choose to list on the ACE Market because its listing criteria is less stringent. For starters, unlike Main Market listings, there is no requirement of a RM20 million profit track record or market capitalisation requirement.

“People choose both the ACE and LEAP Markets because their threshold for listing is flexible. In fact, it is predominantly a sponsor-driven market. This means that if the sponsor feels the company can do well and get a good reception from a listing, they will go ahead with the exercise,” Wong elaborates.

“With Bursa acting as the one-stop agency, I do anticipate more listings on the ACE Market moving forward. So long as the investment banks or qualified sponsors think it is worthwhile and are willing to anchor these listing transactions, we will see more companies going for ACE and LEAP listings,” she predicts.

Tradeview’s Ng concurs that there will be a continued increase in ACE Market listings, in part because of the lower threshold listing requirements compared with the Main Market, but mostly because of the potentially shortened timeframe and ease of process of listing with Bursa serving as the one-stop centre.

“This will enhance the value proposition to list on the ACE Market as it may be just as, if not more, attractive than say the Catalist board of the Singapore Exchange (SGX),” he observes.

Ng points to Malaysia’s large SME (small and medium enterprise) segment, which makes up 90% of total business establishment in the country. There are some good quality names, he asserts, many with even stronger track records than some of the PLCs.

“In the past few years, if we were to track the performance of IPOs on the ACE Market versus the Main Market, it would appear that many ACE Market IPOs performed much better in terms of percentage of return,” he highlights.

Across the 11 ACE Market listings in 2021, the average return over the IPO price was 42%. On the other hand, across seven Main Market listings — including dual-listed OM Holdings Ltd that made its debut in June last year — the average return stood at only 2.2%.

Ng also pointed out that some of the mega IPOs on Bursa in recent years, including Lotte Chemical Titan Holding Bhd, Leong Hup International Bhd and Eco World International Bhd, had not met the expectation of shareholders and investors, and may have dampened corporate and investor sentiment.

“This makes the ACE Market listing option much more enticing. In addition, for companies with the size and profitability that qualifies for Main Market listing on Bursa, they have other options in regional stock markets such as SGX or Hong Kong, which may provide a larger base for fundraising avenue with easier and faster listing regulatory processes,” he observes.

Ensuring same level of investor protection

However, whether warranted or not, some segments of the investing community are of the view that penny stocks and ACE Market counters are subject to speculative trading activities.

And owing to their smaller market capitalisation, and less stringent listing criteria, most fund managers and institutional investors simply will not consider ACE Market companies.

Given that the SC is viewed as one of the more professional regulatory bodies in Malaysia, will there be the same level of investor protection in the future now that the commission is out of the ACE Market IPO approving process?

Vision Group’s Chua sees investor education to improve savviness and understanding of stock market investment as more crucial.

“Education is the best protection for investors while ensuring capital markets continue to be business friendly and vibrant. Bursa can continue to accelerate initiatives to drive investor awareness in areas such as ESG (environmental, social and governance) to drive companies towards good business practices,” he opines.

Chua stresses the need for a balanced and delicate consideration between investor protection and supporting Malaysian businesses to become giants of the future.

“As long as investors are well informed of the risk in investing in every market, there should be a good degree of autonomy left in the hands of investors to decide what is best for them, based on their risk appetite and investment objectives,” he reiterates.

Astramina’s Wong admits that Bursa and the SC are operating at very professional and high levels, and that both are recognised for their high corporate governance standards, so much so that some might even suggest they are overly stringent.

“For example, sometimes the same set of criteria is used for all companies across the board. This does not always work. Students applying to enter kindergarten should be assessed using kindergarten standards. The authorities in the market today impose very high standards, and this should not be the case. As the market matures, more responsibility should go to the sponsors,” suggests Wong, who believes there should be some de-regularisation over time, leaving it to the sponsors and market to make the decisions.

“There is only so much the authorities can do. The market cannot thrive if the authorities impose too many rules and market players are in constant fear and need to check with the authorities for everything. Just come out with a set of rules, and let the market players interpret it themselves. If they breach the rules, then penalise them by all means. This should be the way if we want the market to evolve,” she reiterates.

While the SC was never the approving authority for ACE Market listings as per the Capital Markets and Services Act 2007 (CMSA 2007), it still had a role to play in assessing the prospectus registered by ACE Market prospects, Tradeview’s Ng observes.

“The SC would also be involved during the transfer of listing to the Main Board. So, it is accurate to say that the SC being the independent regulator is very crucial towards safeguarding the interests of investors.”

He also acknowledges that there may be concerns over Bursa, being the sole approving authority, to have complete discretion of allowing ACE Market listings, noting it is in its interest as a corporate entity with a bottom-line key performance indicator (KPI).

That said, he has sufficient confidence in Bursa to do its job professionally as it is in the bourse’s best interest to have not only quantity but good quality companies listed on the ACE Market lest it sacrifices long-term interest for short-term gain.

“I believe the high standards adopted by the SC can be a good reference for Bursa to continuously practise, which includes the profitability test, market cap test and infrastructure test, among others. Bursa itself has disclosure requirements that should be applicable to ACE Market prospects as these are important steps to ensure investor protection,” Ng remarks.

With the SC being less involved in ACE Market listings, he thinks the regulator can now devote more of its resources on enforcement and surveillance to maintain an orderly market, while investigating market manipulations and pump and dump schemes, among others.

“Understandably, it is a fine line to walk for Bursa but our stock market always had a good reputation when it came to IPO due to the stringent review process. For instance, ASX (Australian Securities Exchange), China A-shares [have] many more ‘cowboy’ listings than Bursa,” Ng opines.

Good sign for LEAP Market transfer

Since 2019, many LEAP Market companies have been urging the SC and Bursa to formulate a clear and smooth transfer framework. As it is, if a LEAP Market company wants to migrate to the ACE Market, there is no difference from applying for a new listing, because there is no transfer mechanism in place at the moment.

For perspective, the SC does not get involved in the IPOs of LEAP Market companies as no prospectuses are required. The submission of LEAP Market listings only requires an information memorandum, which is subject to the approval of Bursa. But when it comes to the prospectus-based ACE Market, the SC had been playing an important role as the gatekeeper; well, at least it was until Dec 31, 2021.

Now that Bursa will be the sole approving authority for the ACE Market, and for that matter, the LEAP Market, will transfers from the LEAP Market to the ACE Market be more seamless, and if so, is a proper board transfer framework needed?

“Yes, we still need a transfer framework for the LEAP Market. And I do believe it is on the way,” says Astramina’s Wong.

Citing sources, The Edge had reported at end-August 2020 that the board transfer framework for the LEAP Market could materialise as early as the first quarter of 2021. But a year has gone by and the long-awaited transfer framework has yet to emerge.

As the LEAP Market is relatively new, Wong feels the authorities need time to assess these companies and see whether they are ready to move to the next market.

“We cannot blame the authorities for not coming out with a transfer framework sooner. At the appropriate time, the right framework can be drawn up and eventually will be out,” she insists.

Bursa’s website shows that there are 44 companies listed on the LEAP Market currently. Despite concerns over the transfer framework, the total number of LEAP Market companies have more than tripled from 13 companies in 2018.

“I don’t believe a LEAP company needs to be delisted before going to the ACE or Main Market. This will be a mockery of having the LEAP Market in the first place. Why then have the LEAP Market? The LEAP Market was meant to promote SMEs. The SMEs are the backbone of the Malaysian economy. So, it is really only a natural progression that the framework will be out soon,” says Wong.

Vision Group’s Chua agrees that a transfer framework is still very crucial for aspiring LEAP Market companies looking to migrate to the ACE Market. Clear, stable and predictable as well as easy to understand regulations have always been essential components in the development of a successful capital market and a thriving global financial hub.

“As to whether it will be a seamless process, it will still be dependent on the supporting infrastructure and process to support the migration after there is clarity on the transfer mechanism. Given the Covid environment, it will be great if the whole process is more digital and this could also encourage more foreign-based companies to participate in our markets,” he says.

In the past, in order to raise funds or to sell out, companies only had the option of going to the banks or private equity funds to take up a strategic stake. The LEAP Market was introduced in July 2017 to become an additional avenue for SMEs to raise funds, just as the banks were tightening lending and becoming more selective in disbursing loans while the outflow of foreign funds had been increasing.

Tradeview’s Ng explains that the transfer framework has been non-existent, partly due to concerns over regulatory arbitrage and bypassing the necessary qualifications to be entitled to list on the ACE Market.

Unfortunately, without the board transfer mechanism, there have been several delisting of LEAP Market companies, owing to the strict rule that they could only raise funds from sophisticated and accredited investors. In short, the LEAP Market lacked vibrancy.

“Naturally, with this new regulatory framework, it would be more convenient for all parties. This is the objective of the regulatory change. However, I believe there is still a need for a transfer framework regardless of the SC’s role,” he says.

In essence, Ng believes the regulatory change is timely given the surge in retail investor participation over the past two years to a decades high. In order to keep them invested and to ensure market vibrancy continues, it is imperative to have a greater variety of companies to cater to different risk tolerance and appetite.

“While there are legitimate concerns that the ACE Market may take a turn for the worse if shady companies can bypass the stringent review process without the SC’s direct involvement, I believe Bursa has been doing a good job as we have seen in the past two years. The quality of companies seems to be better compared with those of yesteryears,” he argues.

In fact, he observes many of the speculative penny stocks on the ACE Market were not those listed in recent years.

“Quite a number are legacy companies where original shareholders have long sold out and now appear to be controlled by nominees or syndicates whose real identities are unknown to the general public. These are the companies that give a bad name to the ACE Market and also Malaysia’s stock market as a whole,” he concludes.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- China said to pause new deals with Li Ka-shing, family following plan to sell Panama ports to BlackRock-led consortium

- Ekuinas announces CEO Syed Yasir Arafat to step down on March 31

- Ekuinas to be under PNB’s purview, say sources

- LTAT declares seven-year high dividend of 5.25% for 2024

- Trump says he could cut China tariffs to secure TikTok deal

- Pos Malaysia’s stock surges 35%, trading volume rises to four-year high

- Anwar hopes Madani Mosque can serve as community centre for Muslims, city dwellers

- Former Maybank CEO Farid Alias redesignated as Bursa non-executive chairman from May, replacing Abdul Wahid who is retiring

- Petronas raises US$5b from its first dollar bond in four years

- Cover Story: Timeline of events at Sapura Energy, impact on profit and debt levels