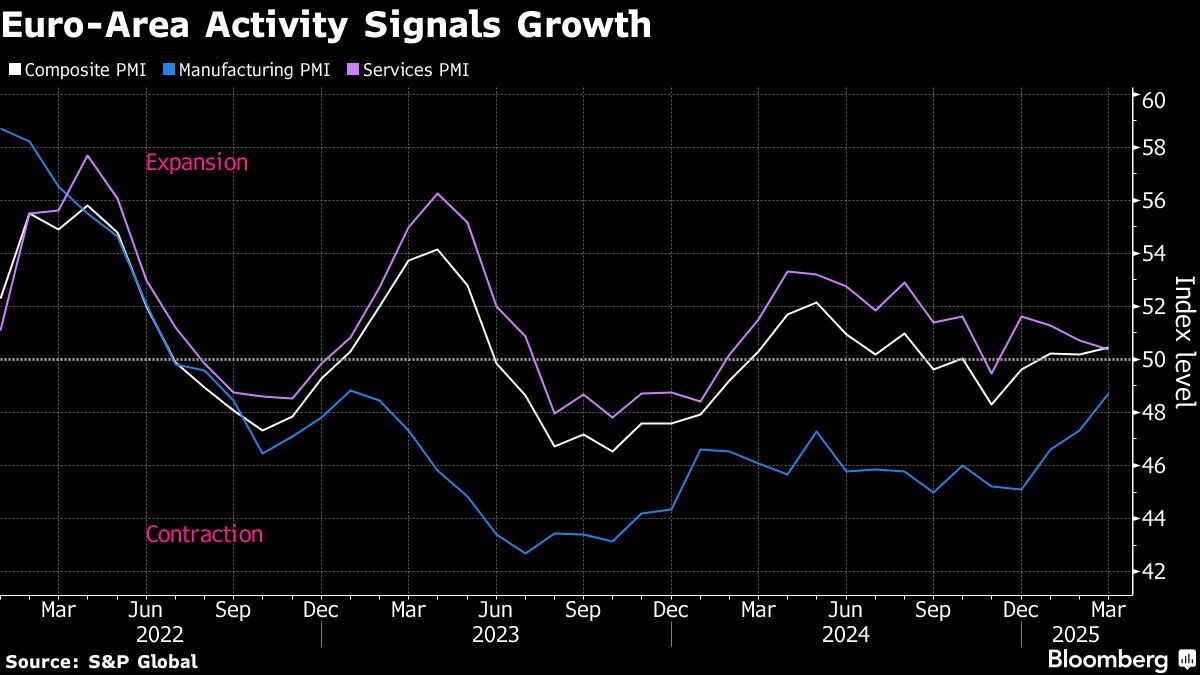

(March 24): Business activity in the euro area reached its highest level in seven months as manufacturers recovered more than expected ahead of a massive increase in German spending.

The Composite Purchasing Managers’ Index by S&P Global rose slightly to 50.4, further above the 50 threshold separating expansion from contraction. Analysts had predicted a slightly higher reading of 50.7.

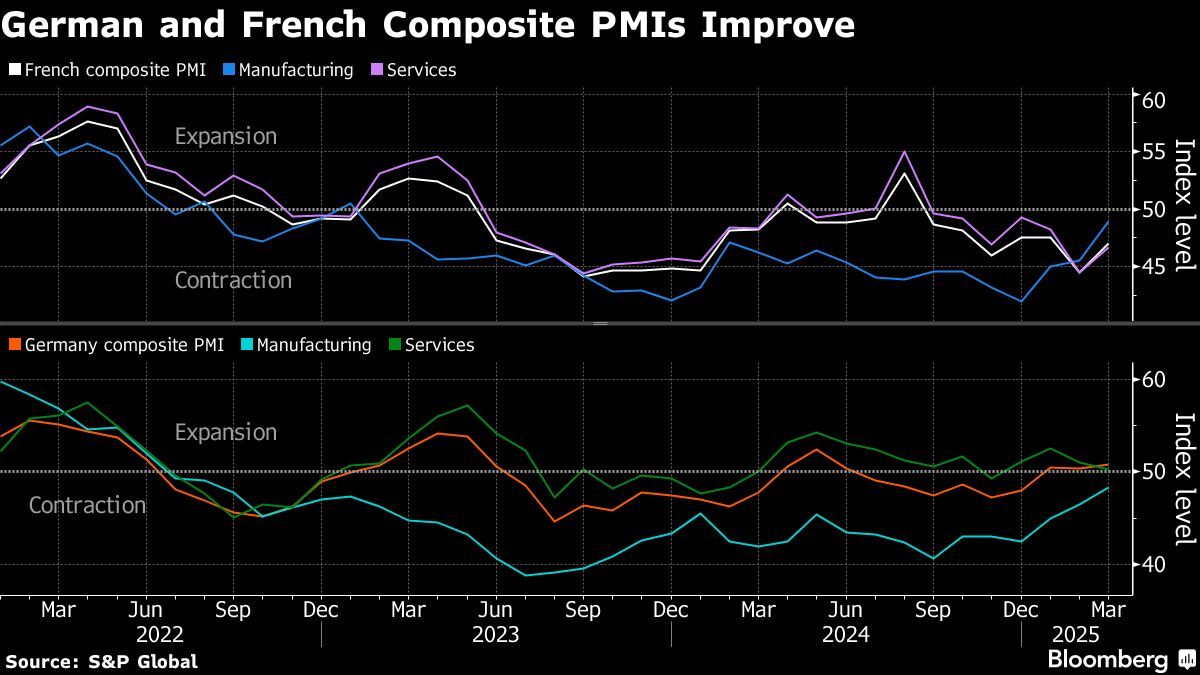

The uptick was largely down to Germany, where a package of infrastructure and defence outlays worth hundreds of billions of euros is set to haul Europe’s largest economy out of five years of stagnation.

But there was also an improvement in France which, while maintaining a sub-50 reading, outpaced analyst expectations as factories also regained some ground.

“Given the will of Europe to invest heavily in defence and infrastructure — in Germany a corresponding historical fiscal package has been approved only last week — hope for a more sustained recovery seems well founded,” Cyrus de la Rubia, an economist at Hamburg Commercial Bank, said Monday in a statement.

The region’s sluggish economy is primed for a boost not just from Germany’s fiscal largess but also a general rearmament drive across the continent in response to waning military support from the US. Factories, which have long been a weak spot — particularly in Germany — are set to be the biggest beneficiaries, even if the improvement takes several months to be felt.

While manufacturers surprised analysts on the upside, the services sector — while still growing — fell short of estimates.

The European Central Bank has also lifted the mood by lowering interest rates for the sixth time since June at this month’s meeting. But the upcoming surge in government spending complicates its task as that will almost certainly prove inflationary.

For now, though, consumer-price growth appears to be heading back to 2%, with the latest headline number from the 20-nation currency bloc coming in at 2.3%.

According to S&P, March saw both input costs and selling prices in the services industry, which is under particular scrutiny at the ECB, rise at a slower pace than in recent months. That could tilt April’s ECB decision toward those backing another reduction in rates. Markets currently see the outcome of that meeting as a coin toss.

“The price development will be well received by the doves,” de la Rubia said. But risks including retaliation against US tariffs, measures to curb goods arriving from China, and higher food prices will “make some ECB members hesitant to cut rates too aggressively”, he added.

PMIs are closely watched by markets as they arrive early in the month and are good at revealing trends and turning points in an economy. A measure of breadth of changes in output rather than depth, business surveys can sometimes be difficult to map directly to quarterly GDP.

Elsewhere, the UK’s composite PMI unexpectedly rose. The US’s reading, due later Monday, is seen dipping a little while remaining above the 50 mark.

Uploaded by Arion Yeow

- Gamuda says to sign several 'imminent' large contracts, as 2Q profit grows 4.8%

- UOB Kay Hian appoints Anne Leh as new CEO

- KLIA Master Plan under review, brick-and-mortar expansion on hold — MAHB

- Gas Malaysia declares final dividend of 10.28 sen per share

- Special Report: Penny stock fever rose as billions poured into market

- Cops probing video, organisation suspected of promoting communist ideology

- Atlantic releases full Signal text chain on Houthi attacks

- Used cooking oil now main commodity in production of sustainable aviation fuel

- 14,000 pigs culled so far in Selangor to curb ASF outbreak, says Veterinary Services Dept

- Bursa Malaysia, subsidiaries to close for Hari Raya Aidilfitri