KUALA LUMPUR (March 24): Malaysia’s banking system remains well-capitalised against potential liquidity shocks and supportive of financial intermediation for the Malaysian economy, according to Bank Negara Malaysia (BNM).

The central bank’s view is premised on the banking system’s total capital ratio of 18.3% and capital buffers of RM136.8 billion, well above the regulatory minimum as at end-December 2024, it said in its Financial Stability Review — Second Half 2024, released on Monday.

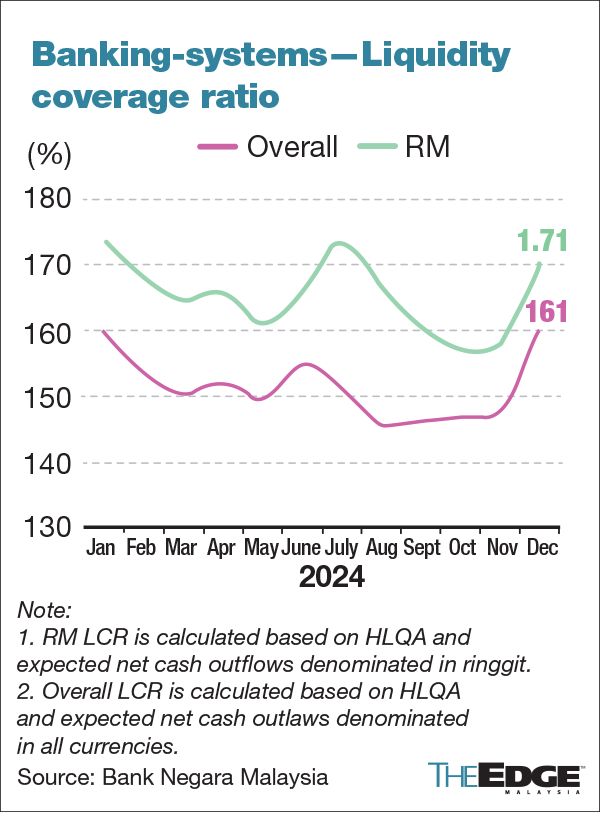

The banking system also has enough cash and assets to see it through short-term and long-term financial obligations, with a liquidity coverage ratio of 160.7% and a net stable funding ratio of 116.3%, both “healthy and above regulatory minima”, BNM said.

The central bank believes the banking system is resilient to liquidity shocks, with strong capital buffers that help banks continue to provide credit and absorb unexpected losses.

Stress tests confirmed the system’s ability to withstand economic shocks, using two severe scenarios — worse than the 2008 Global Financial Crisis and the 2020 pandemic — to assess the resilience of financial institutions.

Healthy lending rate, improved loan quality

Annual lending rate remained healthy at a 5.5% year-on-year (y-o-y) increase at end-December 2024, against a 2015-2019 compound annual growth rate (CAGR) of 5.3%, according to BNM.

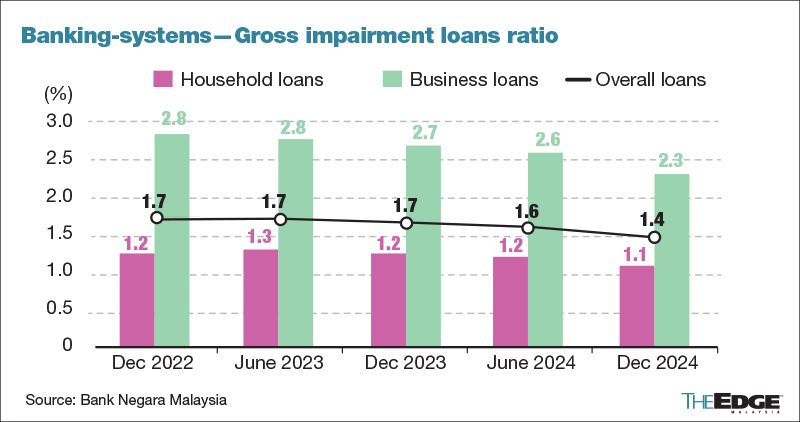

The central bank said asset quality also continued to improve. Gross impaired loans ratio declined to 1.4% at end-December 2024, versus 1.7% at end-December 2023.

The share of loans classified as Stage 2 — having higher credit risk — declined further below the pre-pandemic (2018-2020) average of 8%, to 6.6% in 2024.

“Consistent with this, loans under repayment assistance programmes declined to 1.7% of total banking system loans (June 2024: 2%), while newly rescheduled and restructured loans of borrowers facing financial strains remained small at 0.08% of banks’ total loans (June 2024: 0.09%),” it said.

Loan loss coverage ratio increased to 129% in 2024 versus a 2015-2019 average of 114.4%, reflecting an increase in collective impairments held by banks on the back of continued robust loan growth in 2024, BNM said.

Deposits, meanwhile, grew at 3% year-on-year (y-o-y) in 2024, slower than the compound annual growth rate (CAGR) between 2015-2019 of 4.4%.

Earnings boost from higher interest income

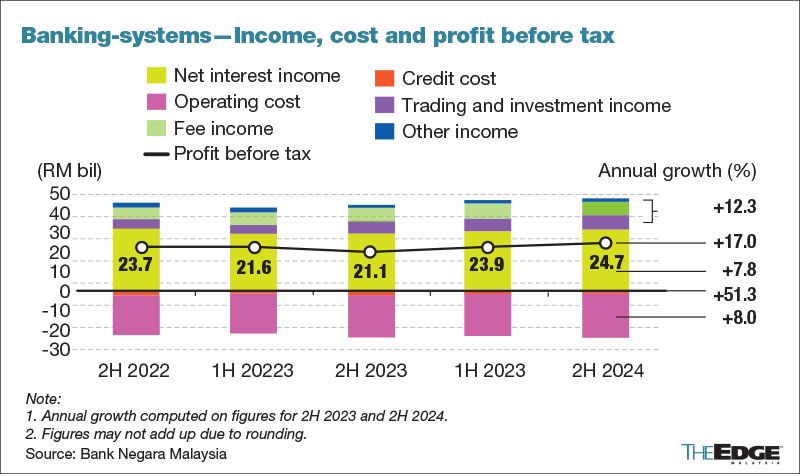

BNM said banks’ earnings improved y-o-y in 2024, supported by interest income amid robust overall loan growth.

Higher interest income and slower growth in interest expense contributed to improved net interest margins of 2.2% as at end-December 2024, versus 2% at end-June 2024 and 1.96% in average between 2015-2019.

“Meanwhile, the cost-to-income (CTI) ratio increased slightly to 47.9% (June 2024: 46.6%), mainly driven by an increase in employee expenses,” it added.

BNM said substantial foreign exchange gains in the third quarter of 2024 drove banks to log trading and investment income of RM7.8 billion in the second half of 2024 (2H2024), which provided additional support to earnings.

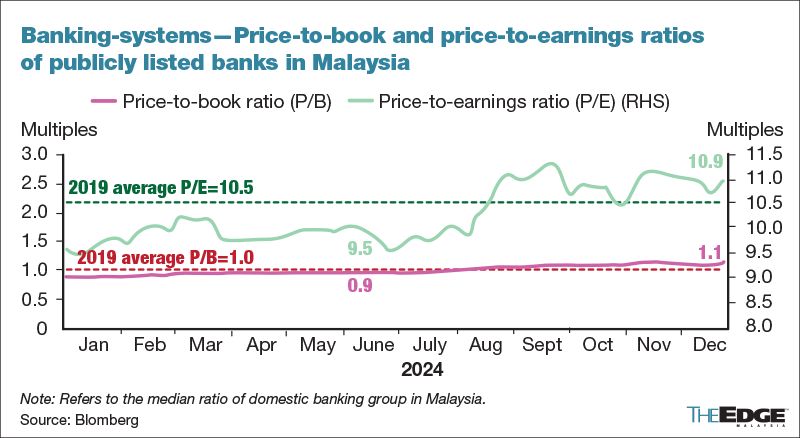

“Consistent with higher earnings in 2H2024, returns on assets and equity of the banking system rose slightly to 1.4% and 12.2% respectively (June 2024: 1.3% and 12.1% respectively). This, in turn, supported the market valuations of listed banks, as measured by the price-to-book and price-to-earnings ratios,” the central bank said.

“Looking ahead, the positive growth outlook for the economy will provide sustained support for banks’ profitability,” it added.

- Xpeng may add EV output in Europe, Latin America in growth push

- Xi tests US allies in Indo-Pacific as Trump looks elsewhere

- Trump says he could cut China tariffs to secure TikTok deal

- Trump weighs imposing copper import tariffs in weeks, not months

- Trump to hit auto imports with 25% tariff in trade fight