KUALA LUMPUR (March 24): Personal financing disbursed to civil servant borrowers has seen a sharp increase since the salary hike implemented in December last year, according to Bank Negara Malaysia (BNM).

Monthly personal financing disbursements to civil servant borrowers surged to an average of RM6.4 billion in December 2024 and January 2025, versus a 2023-2024 monthly average of RM3.6 billion, BNM said in its Financial Stability Review report released on Monday.

The central bank said this outstripped personal financing disbursements to other borrowers, which expanded more moderately at an average of RM4.5 billion in the same period against a 2023-2024 monthly average of RM4.1 billion.

The surge in personal financing disbursements to civil servants was one of two developments BNM flagged as “notable developments during the period [that] warrant continued vigilance” concerning household debt.

The other development underlined was organised fraudsters targeting borrowers with repayment arrears, mostly civil servants, to refinance their existing debt with the false promise of lucrative returns from dubious investment schemes.

“Both developments have so far been contained with banks increasing their vigilance during credit assessments, alongside an intensification of financial education efforts,” BNM said.

“Crucially, sound lending standards observed by banks will remain key to support household resilience, particularly among non-prime borrowers in an environment of rising cost of living,” it added. Non-prime borrowers refer to less-creditworthy borrowers, including those with records of missed repayments, according to BNM.

Last year, civil servants under the management and professional category received an 8% salary hike effective Dec 1, under the first phase of the government’s 15% pay raise initiative. A further 7% raise is slated under the second phase, effective Jan 1, 2026.

Civil servants under the upper management category saw a 4% raise under the first phase, and will see another 3% hike in the second phase.

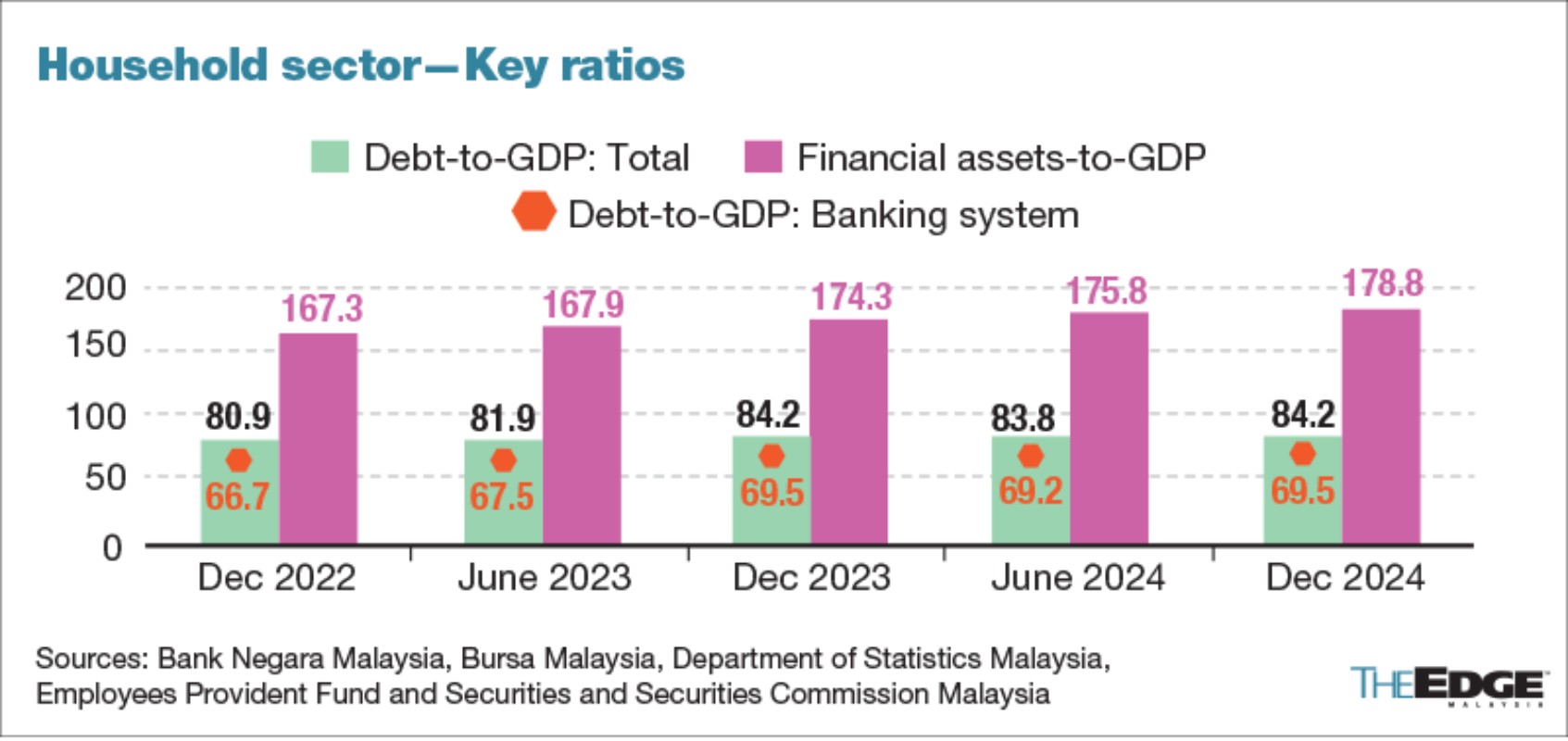

Household debt-to-GDP remains steady year-on-year, up from mid-year

Looking broader, BNM reported that the aggregate household debt-to-gross domestic product (GDP) ratio stood flat at 84.2% at end-December 2024, from a year ago.

However, the ratio has risen from 83.8% in mid-2024, which the central bank attributed to continued improvements in labour market conditions and economic activity.

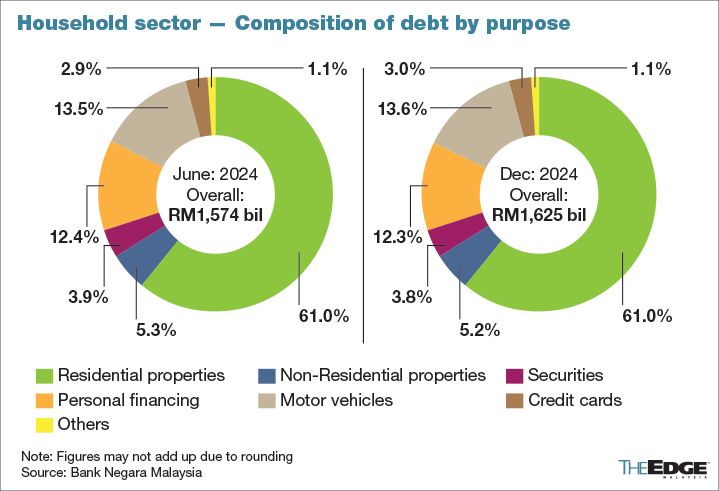

The growth in overall debt was mainly driven by housing and car loans, it noted, which collectively comprised 74.6% of household debt.

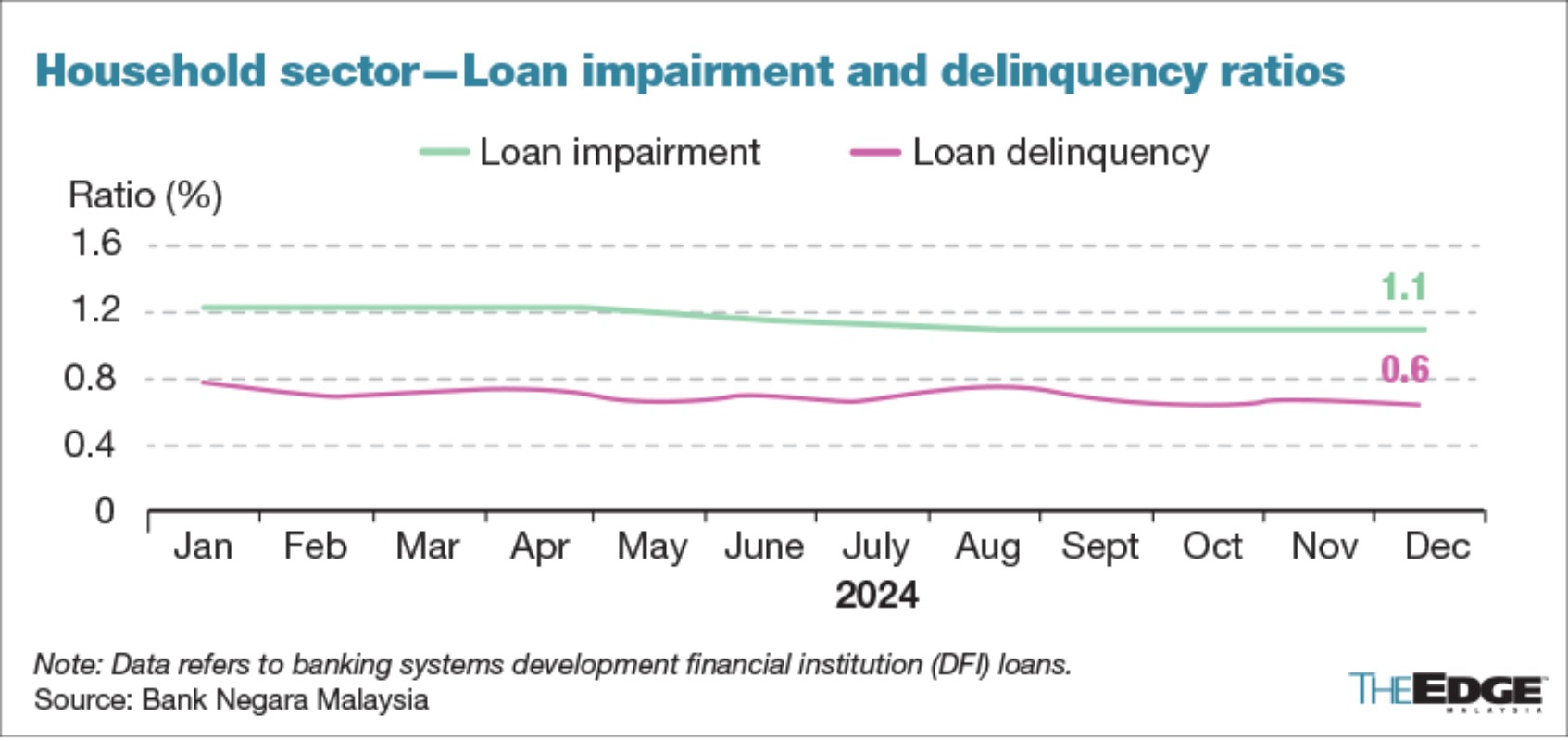

Nonetheless, loan delinquencies and impairments continued to decline across all income groups. Meanwhile, the share of household loans classified as Stage 2 — having higher credit risk — declined marginally to 4.3% as at end-December 2024, versus 4.4% at end-June 2024.

Overall, BNM said household balance sheets remained sound, with household financial assets on aggregate remaining in excess of debt by 2.1 times — providing healthy buffers against adverse shocks.

“Moving forward, households’ debt-servicing capacity will continue to be supported by favourable labour market conditions and sustained income growth,” the central bank said.

Continued efforts to rationalise blanket government subsidies in 2025 are not expected to significantly affect household financial resilience, given corresponding income support measures that are anticipated to still be available to most households,” it also noted.

- Xpeng may add EV output in Europe, Latin America in growth push

- Xi tests US allies in Indo-Pacific as Trump looks elsewhere

- Trump says he could cut China tariffs to secure TikTok deal

- Trump weighs imposing copper import tariffs in weeks, not months

- Trump to hit auto imports with 25% tariff in trade fight