(From left): Newly appointed BNM deputy governor Aznan Abdul Aziz; recently retired former BNM deputy governor, now BNM technical adviser on financial stability Jessica Chew Cheng Lian; BNM governor Datuk Seri Abdul Rasheed Ghaffour, and BNM deputy governors Marzunisham Omar and Adnan Zaylani Mohamad Zahid at the BNM Annual Report 2024 release on Monday. (Photo by Shahrin Yahya/The Edge)

KUALA LUMPUR (March 24): Bank Negara Malaysia (BNM) maintained its forecast for the country's economy to expand steadily this year, as domestic demand stays robust amid intensifying external headwinds.

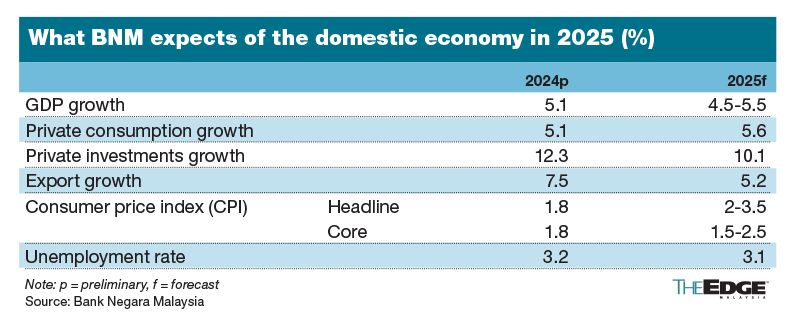

Gross domestic product (GDP) growth will likely range between 4.5% and 5.5% for 2025, the central bank reiterated in its Economic and Monetary Review report released on Monday, in line with the Ministry of Finance’s Budget 2025 forecast. In 2024, the Malaysian economy expanded by 5.1%.

“In the face of external uncertainties, domestic demand is expected to remain Malaysia’s anchor of growth amid steady private sector expenditure,” BNM said.

Household spending is expected to increase, driven by employment and faster income growth, as well as policy support, while investment activity will continue to see a robust expansion as the upcycle extends into 2025, the central bank noted. Growth in exports, however, will be moderate, it said.

Unemployment will improve to 3.1% this year — near the 3% level economists generally consider as the economy having full employment.

Inflation to pick up as expected

Inflation, meanwhile, will come in hotter this year as expected. The consumer price index (CPI), the country’s main gauge for inflation, will rise 2.0% to 3.5% — unchanged from its previous forecast. Core inflation would be in the bounds of 1.5% to 2.5%.

In 2024, both headline and core inflation was 1.8%.

The central bank noted that the wider forecast range took into consideration impacts from the rollout of major policy reform measures — including the RON95 subsidy rationalisation, sales and service tax (SST) expansion, and wage-related measures.

“The impact of policy measures [on] inflation is subject to details surrounding implementation,” BNM said. “The effects, however, are expected to be transitory and manageable.”

The direct impact from a one-off RON95 fuel price adjustment to inflation is projected to lapse a year after its implementation, BNM said. The planned SST expansions are primarily focused on non-essential food and durable products, which are “a small subset of the CPI basket,” it noted.

The indirect effects on inflation via spillovers to prices of other goods and services will also be largely contained, the central bank said.

However, BNM cautioned that there would be upside risks to inflation if domestic reforms take place against a stronger-than-expected demand environment, where firms find it easier to raise prices and pass on costs to consumers.

“This may lead to knock-on effects on the prices of other goods and services, contributing to pressures on underlying inflation,” BNM flagged. “The degree of these interactions and spillovers are expected to be reflected in the pervasiveness and persistence of inflation, which are monitored very closely.”

Externally, the upside risks to inflation would be from trade restrictions, alongside retaliatory actions among key trading nations. “Such developments may lead to higher domestic inflation through three channels: increased imported inflation; a stronger dollar due to risk aversion in financial markets; and higher production costs as a result of supply chain disruptions,” BNM said.

- UOB Kay Hian appoints Anne Leh as new CEO

- Gas Malaysia declares final dividend of 10.28 sen per share

- Kenneth Vun now MD at both Symphony Life and XOX

- Change of guard at Ekuinas — sources

- LSH Capital, Matrix Concepts, Symphony Life, Gamuda, Gas Malaysia, Kim Loong, United Malacca, MyNews, Marine & General, Dayang, Nestcon, Solarvest, Rohas Tecnic, Bintai Kinden