This article first appeared in Capital, The Edge Malaysia Weekly on March 17, 2025 - March 23, 2025

Telecommunication

Neutral

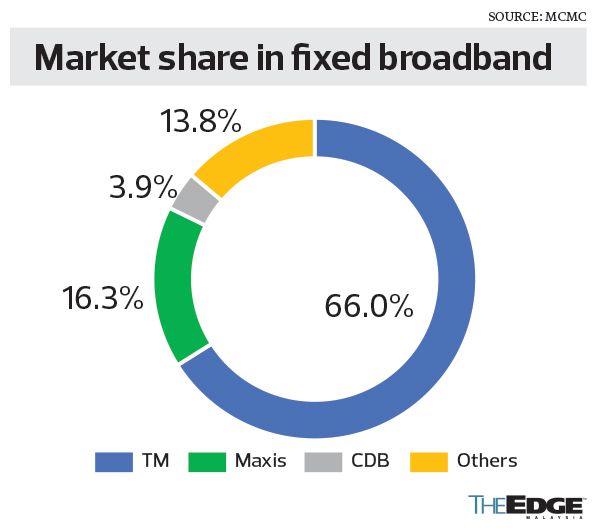

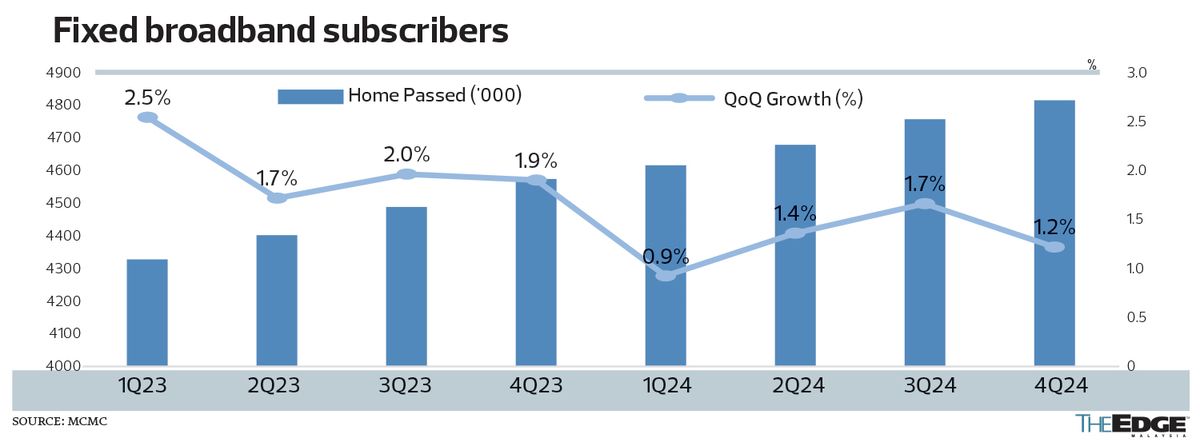

APEX SECURITIES (MARCH 10): Fixed broadband adoption remained strong, with subscribers rising 5.3% year on year (y-o-y) and 1.2% quarter on quarter (q-o-q) to 4.8 million in 4Q2024, led by increasing demand for high-speed connectivity for remote work, online learning and streaming. 5G adoption surged by 119.9% y-o-y to 18.2 million subscribers in 2024, while 4G subscriptions declined by 28.1% y-o-y, reflecting a significant shift in consumer preference. The government has identified locations for Jendela Phase 2 and is currently assessing the most suitable technologies for its implementation. Although a concrete timeline has yet to be determined, we believe the tender process should commence latest by end-2025. Furthermore, we also note that contractor performance from Phase 1 will play a crucial role in vendor selection, ensuring that only experienced and reliable contractors are appointed. This is expected to narrow down competition, favouring players with a strong track record in government projects. We downgrade our rating on the sector to “neutral” (previously “overweight”), as we expect significant capital expenditure (capex) for network upgrades to continue squeezing profitability. In addition, we believe that stagnant average revenue per user (ARPU) growth, coupled with fading optimism over the data centre boom, could lead to a de-rating in valuations. Our top pick for the year will be Redtone Digital Bhd (KL:REDTONE) (Buy; Fair value (FV): 95 sen) as it is well positioned to benefit from Jendela P2, with the government prioritising nationwide network expansion. We opined a collaboration with U Mobile Sdn Bhd for 5G infrastructure will drive new contract wins and top line growth. Besides that, we favour Telekom Malaysia Bhd (KL:TM) (Buy, FV: RM7.40) as a key asset owner, given its critical role in providing connectivity. Regardless of Digital Nasional Bhd’s or U Mobile’s plans for the second network, both will still need to rely on TM’s fibre infrastructure in the near term to ensure seamless 5G service delivery. Meanwhile, we view Axiata Group Bhd (KL:AXIATA) (Buy, FV: RM2.10) as a compelling value play as it is currently trading at 4.4 times forward EV/Ebitda (-1 standard deviation), with strong potential to unlock synergies from the upcoming PT XL Axiata Tbk and PT Smartfren Telecom merger. For Maxis Bhd (KL:MAXIS) (Buy, FV: RM4) and CelcomDigi Bhd (KL:CDB) (Hold, FV: RM4), we expect operating expenditure to remain elevated, in line with FY24, due to the higher capex spending.

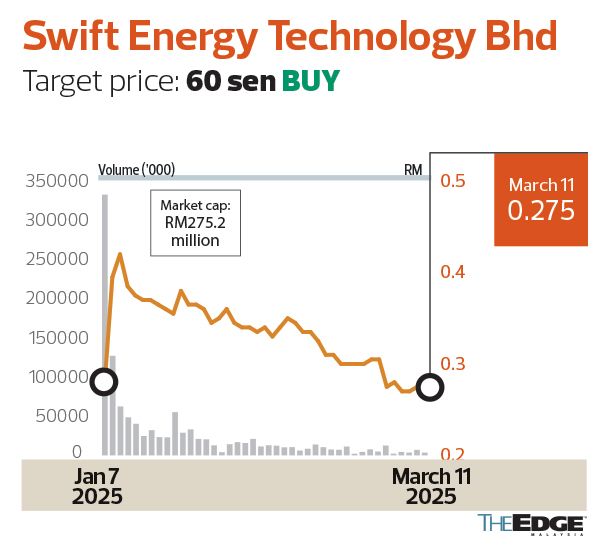

Swift Energy Technology Bhd

Target price: 60 sen BUY

KENANGA RESEARCH (MARCH 10): Swift Energy Technology (KL:SET) has secured two unexpected contracts worth RM24.37 million: one for Shell’s platform and the other for Petroliam Nasional Bhd’s META project. Notably, the company has struck a game-changing deal with China’s only major contractor for Shell’s platform in Nigeria — marking both its second collaboration with China and its second-largest contract to date. Year-to-date wins surged to RM44.5 million, driving its order book to a record RM100 million high. With strong momentum, bigger wins are brewing and a major ramp-up is expected in 2H25.

We maintain our forecasts and target price of 60 sen, implying a potential double-bagger with an “outperform” call. We like SET for: (i) being the only explosion-proof solar photovoltaic player in Asean and one of only six globally, distinguished by its comprehensive product offerings, (ii) capitalising on global net zero commitments in oil and gas (O&G) industry, and (iii) being a proxy to Wilmar International Ltd’s expansion plan. Risks to our call include: (i) its dependency on global renewable energy policy, (ii) the slowdown in O&G and grain product industries, and (iii) non-renewal of product certifications such as ATEX and IECEx.

Kerjaya Prospek Group Bhd

Target price: RM2.60 BUY

PHILLIP CAPITAL (MARCH 11): Kerjaya Prospek Group (KL:KERJAYA) has secured a RM51 million contract for piling and earthworks from Eastern & Oriental Bhd (KL:E&O) for a planned 52-storey development on Andaman Island, Penang. With this latest award, the group’s outstanding order book stands at RM4.1 billion, translating into 2.4 times 2024 construction revenue cover ratio and providing revenue visibility until 2027. Assuming a group blended 10% profit after tax margin, we estimate this project to contribute RM5.1 million in Patami over 2025-2026.This contract brings year-to-date wins to RM307 million, accounting for 19% of our RM1.6 billion full-year 2025 order book replenishment assumption. Going forward, we expect contract flows to remain robust, underpinned by contracts from both E&O and Kerjaya Prospek Property Bhd (KL:KPPROP). Near-term prospects include Kerjaya Prospek Property’s upcoming projects in Shah Alam (RM250 million estimated gross development value, or GDV) and Damansara Damai (RM430 million estimated GDV) as well as E&O’s Maris (RM690 million estimated GDV).

We remain optimistic about Kerjaya Prospek Group’s earnings prospects, which are underpinned by its robust contract flows from E&O and Kerjaya Prospek Property. Key downside risks include lower-than-expected order book replenishment and project margin deterioration.

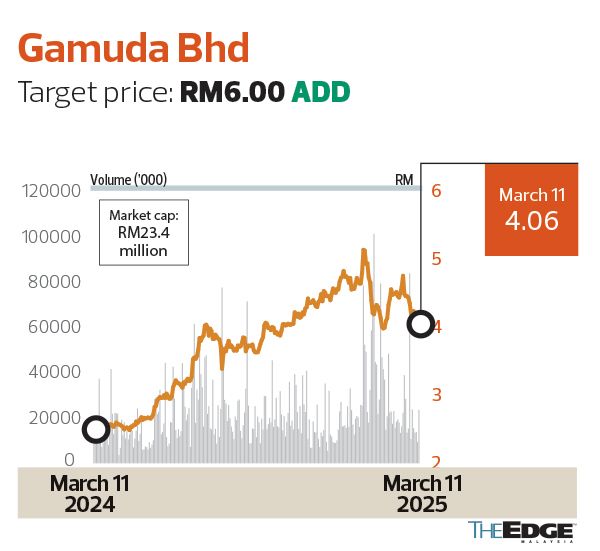

Gamuda Bhd

Target price: RM6.00 ADD

CGS INTERNATIONAL (MARCH 10): Gamuda Bhd (KL:GAMUDA) will release its 2QFY25 results on March 26. We expect it to be a modest quarter. By February 2025, 41% of the company’s RM37 billion order book comprises higher-margin local projects, including data centres, the Upper Padas hydro dam and the Penang Light Rail Transit. However, these projects remain at the early stages of S-curve recognition. Additionally, the higher-margin Vietnam project, Eaton Park, which recorded RM970 million in presales during FY24 (accounting for 20% of total FY24 presales), has not reached the threshold for meaningful recognition.

We remain convinced that Gamuda can hit the higher end of its RM40 billion to RM45 billion order book target by end-2025, given year-to-date FY25 new wins of RM13.4 billion. This would imply that it needs an additional RM20 billion new wins by end-2025, assuming a burn rate of RM1 billion per month. We reiterate “add” on Gamuda for its diversified order book and growing property business. Key downside risks are delays in contract awards and higher raw material costs. Key rerating catalysts are more construction wins and stronger property sales.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Powerful quake in Southeast Asia kills several, 81 trapped in Bangkok building rubble

- Genting says Nevada authorities have signed off settlement terms for Las Vegas complaint

- CK Hutchison will not sign deal to sell strategic Panama ports next week — Reuters

- Businessman who assaulted bodyguards for fasting sentenced to six years and 10 months' jail

- Foreign investors shifting to safer Malaysian assets amid market volatility — analyst

- China's top airlines post fifth year of losses in 2024 in the face of domestic competition

- MN Holdings, Genting, MMAG, LSH Capital, Able Global, Kerjaya Prospek Property, Yinson, GUH Holdings, DNeX and Sarawak Cable

- Huawei bosses likely knew of alleged EU bribes, say Belgians

- Baltic Exchange shipping updates: March 28, 2025

- US pauses financial contributions to WTO — Reuters