A weekly round-up of tanker and dry bulk market (March 28, 2025)

This report is produced by the Baltic Exchange.

The Baltic Exchange, a wholly-owned subsidiary of Singapore Exchange, is the world's only independent source of maritime market information for the trading and settlement of physical and derivative contracts.

Its international community of over 650 members encompasses the majority of world shipping interests and commits to a code of business conduct overseen by the Baltic.

For daily freight market reports and assessments, please visit www.balticexchange.com.

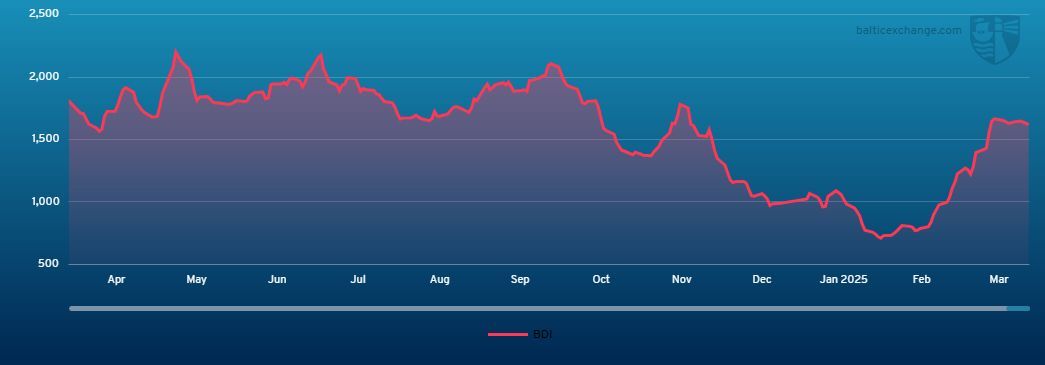

Capesize

The Capesize market started the week on a firmer note but gradually softened as activity failed to gain momentum. The BCI 5TC began positively at US$22,311 but declined steadily, closing the week at US$20,503. In the Pacific, initial optimism driven by fresh cargo and miner activity was quickly overshadowed by a buildup of tonnage, leading to a steady decline in rates. Offers on C5 slipped from US$9.30 early in the week to US$8.65 by week's end, with TC rates struggling to hold above the US$20,000 mark. In the Atlantic, sentiment initially supported by tight tonnage in ballast weakened as softer fixtures emerged, particularly on the South Brazil and West Africa to China routes. C3 levels, initially in the high US$25s, steadily eroded to the very low US$23s, for index dates, with little resistance from market participants. The North Atlantic saw some support from fronthaul activity, particularly with West Africa stems, however, trans-Atlantic cargo remained scarce, adding to the bearish tone.

Panamax

A solid week for the Panamax market, as both basins saw sizeable gains. In the Atlantic, an active week saw NC South America as the common driver for both fronthaul and trans-Atlantic demand. US$20,000 was seen concluded on 82,000dwt tonnage delivery Jorf Lasfar for a trip via NC South America redelivery Fareast, whilst further South, rates traded at contrasting levels dependent on date arrivals, voyage cargoes were seen trading at a discount to P6 equivalent but solid demand throughout April into May helped to supported timecharter rates overall. The Pacific market rose steadily throughout the week buoyed by decent demand both ex NoPac and Australia the former seeing rates concluded at US$15,000 on several index type units, activity ex Indonesia remained steady rather than spectacular but with firm levels available trips into India, rates for the P5 route gained circa US$1,800 week on week as tighter tonnage impacted. Limited period activity, rates varied between US$14,500 and US$16,500 for 82,000dwt types for short period.

Ultramax/Supramax

A rather uneventful week for the sector as the political uncertainty caused a more cautious approach. The Atlantic generally remained steady although there was a more positive feel from the Continent-Mediterranean as brokers spoke of better levels of enquiry. The US Gulf remained relatively flat as brokers were saying rates remained in the mid-upper teens for fronthaul ultramax. The South Atlantic again was finely balanced although a 63,000 was heard fixed delivery Recalada trip to Egypt at US$18,000. Demand remained from South Africa, a 64,000 fixing delivery Lagos via Saldanha Bay trip China at US$15,000. Otherwise, the Asian arena lost ground as sentiment remained negative. An ultramax was heard fixed delivery Far East for a NoPac round in the mid US$13,000s. Otherwise a 64,000 fixed delivery Yangzhou for a trip to Bangladesh at US$16,000. Backhaul business was a little subdued although a 52,000 was heard fixed basis delivery Jingtang trip to the Mediterranean at US$15,000. Period activity was limited although a 57,000dwt open Hong Kong fixed for 1 year’s trading in the US$13,000s.

Handysize

This week, the market has shown a mixed performance across the regions. In the Continent and Mediterranean, there’s a sense of stability, supported by a healthy cargo book and ongoing orders. For instance, A 33,000dwt fixed for delivery Rotterdam trip to redelivery West Mediterranean with grains at US$14,000 for Morocco and at US$15,000 for Algeria. In the South Atlantic and US Gulf, market fundamentals remained generally slow. A 39,000dwt heard fixed for delivery Recalada to redelivery Salvador-Fortaleza range with grains at US$14,750. Meanwhile, in Asia, the market remained healthy, with a steady demand-supply balance, particularly in Southeast Asia, several strong fixtures reported. A 38,000dwt open Villanueva March 27 onward heard fixed via Dampier to China with salt at US$13,300. Period activity was limited, although a 28,000-dwt open North China fixed 3/5 months trading at US$10,350.

Clean

LR2

MEG LR2’s reached an impasse this week with freight levels ultimately dropping, but only modestly. The TC1 75Kt MEG/Japan index went from WS163.61 to WS153.33. A TC20 90kt MEG/UK-Continent assessment dropped by US$243,000 to US$3.956 million.

West of Suez, Mediterranean/East LR2’s of TC15 held stable with the index dipping just below US$3 million to US$2.985 million.

LR1

MEG LR1 freight climbed again this week. The TC5 55kt MEG/Japan index has come up another 9.06 points to WS180.94. A voyage west on TC8 65kt MEG/UK-Continent went from US$3.12 million to US$3.33 million.

On the UK- Continent LR1’s was stronger this week with the TC16 60kt ARA/West Africa index climbing 2.81 points to WS115.94.

MR

Following last week’s climb MRs in the MEG were retested down this week, the TC17 35kt MEG/East Africa index lost 27.5 points to WS237.5 as a result.

UK-Continent MR’s spiked mid-week to then resettle back down by the end. The TC2 37kt ARA/US-Atlantic coast trip peaked at WS195 up from WS177.5 to then return to WS185.63 at time of writing. The Baltic description round trip TCE for the run has subsequently ended up at US$29,086 /day.

USG MRs saw a strong upturn in freight levels this week off the back of an influx in enquiry removing prompt vessels from the market. The TC14 38kt US-Gulf/UK-Continent went from WS121.43 to WS136.79. The TC18 the 38kt US Gulf/Brazil index similarly went up by 25 points to WS201.43 and a Caribbean run on TC21, 38kt US-Gulf/Caribbean jumped another 38% to 839,286.

The MR Atlantic Triangulation Basket TCE went from US$28,283 to US$31,802.

Handymax

Baltic Clean Handymax routes came back downward this week. In the Mediterranean, the TC6 index shed 30 points to WS248.89 and on the UK-Continent the TC23 30kt Cross UK-Continent went from WS206.94 to WS198.06.

VLCC

The market eased this week with the rate for the 270,000 mt Middle East Gulf to China trip (TD3C) about six points lower at WS58.95 corresponding to a round-trip TCE of US$39,224. In the Atlantic market, the rate for 260,000mt West Africa/China (TD15) also fell by six points to WS59.88 giving a round voyage TCE of US$40,899 per day. The rate for 270,000mt US Gulf/China (TD22) increased again, improving by US$262,555 since last Friday, to US$8,522,500 which shows a daily round trip TCE of US$45,838.

Suezmax

Suezmax rates turned back up in the Atlantic with the rate for the 130,000mt Nigeria/UK Continent voyage (TD20) recovering seven points to WS102.92 meaning a daily round-trip TCE of US$45,125 while the TD27 route (Guyana to UK Continent basis 130,000mt) increased by six points to WS100.28 translating to a daily round trip TCE of US$43,322 basis discharge in Rotterdam. For the TD6 route of 135,000mt CPC/Med the rate has remained about the WS130 level showing a daily TCE of a US$63,123 round-trip. In the Middle East, the rate for the TD23 route of 140,000mt Middle East Gulf to the Mediterranean (via the Suez Canal) has stayed around the WS93-94 level.

Aframax

In the North Sea, the rate for the 80,000mt Cross-UK Continent route (TD7) finally improved, jumping 19 points to WS126.67 giving a daily round-trip TCE of over US$43,100 basis Hound Point to Wilhelmshaven.

In the Mediterranean market the rate for 80,000mt Cross-Mediterranean (TD19) has rocketed about 69 points to WS198 (basis Ceyhan to Lavera, that shows a daily round trip TCE of about US$69,372).

Across the Atlantic, the rollercoaster has gone for another turn with the rates for the 70,000mt East Coast Mexico/US Gulf route (TD26) and the 70,000mt Covenas/US Gulf route (TD9) ascending close to 47 and 45 points, respectively, to just above WS189. This shows a daily round-trip TCE of US$49,644 and US$46,392.

The rate for the trans-Atlantic route of 70,000mt US Gulf/UK Continent (TD25) also jumped aboard and rose 34 points to WS182.5 giving a round trip TCE basis Houston/Rotterdam of US$47,747 per day.

LNG

This week, the LNG market experienced a decline, with most routes seeing a drop in rates.

On the BLNG1 Gladstone-Tokyo route, 174k cbm vessels gained US$400, reaching US$27,900 per day, while 160k cbm vessels declined by US$600, settling at US$17,800 per day.

In the Atlantic, the BLNG2 Sabine-UK Continent route saw a US$2,500 drop for 174k cbm vessels, closing at US$28,000 per day, with 160k cbm vessels also falling by US$1,200 to US$14,000 per day. The BLNG3 Sabine-Tokyo route posted similar declines, with 174k cbm vessels down US$1,700 to US$31,400 per day, while 160k cbm vessels dropped by US$800, settling at US$15,800 per day.

In the period market, six-month and one-year rates saw a slight increase. Six-month charters rose by US$100 to US$28,600 per day, while one-year rates jumped US$3,750 to US$33,750 per day. Meanwhile, three-year rates remained unchanged at US$53,500 per day.

LPG

The LPG market saw a downward correction this week, with rates declining across all routes, reversing last week's positive momentum.

On the BLPG1 Ras Tanura-Chiba route, rates fell by US$4.58 to US$57.58, while TCE earnings dropped by US$5,467, settling at US$40,626 per day. This decline reflects weaker sentiment in the Middle East market, due to increasing vessel availability and lack of volumes.

In the Atlantic basin, the BLPG2 Houston-Flushing route also saw a softening trend, with rates decreasing by US$2, closing at US$54.00, while TCE earnings declined by US$3,254, settling at US$52,012 per day.

The BLPG3 Houston-Chiba route experienced the sharpest decline, with rates falling by US$5.83 to US$103.67, while TCE earnings dropped by US$4,978, closing at US$37,447 per day. This suggests a cooling in the long-haul market, potentially due to reduced arbitrage opportunities.

Disclaimer:

While reasonable care has been taken by the Baltic Exchange Information Services Limited (BEISL) and The Baltic Exchange (Asia) Pte. Ltd. (BEA, and together with BEISL being Baltic) in providing this information, all such information is for general use, provided without warranty or representation, is not designed to be used for or relied upon for any specific purpose, and does not infringe upon the legitimate rights and interests of any third party including intellectual property. The Baltic will not accept any liability for any loss incurred in any way whatsoever by any person who seeks to rely on the information contained herein.

All intellectual property and related rights in this information are owned by the Baltic. Any form of copying, distribution, extraction or re-utilisation of this information by any means, whether electronic or otherwise, is expressly prohibited. Persons wishing to do so must first obtain a licence to do so from the Baltic.

- Xi's showdown with Li Ka-shing threatens China’s pro-business push

- Tan Kean Soon steps down as T7 Global executive deputy chairman, board says no operational impact

- Company auditor loses RM1.29m to investment scam

- Volvo Car brings back Samuelsson as CEO to steer turnaround

- Perak emerges as Malaysia's No 1 sweet corn producer