This article first appeared in Capital, The Edge Malaysia Weekly on March 17, 2025 - March 23, 2025

LAST week, Wall Street saw its sharpest single-day fall in more than two years due to fears of stagflation and recession — arising from tit-for-tat tariff measures — that could hit the world’s largest economy.

As the real impact from the trade war is yet to be ascertained, investors should maintain their exposure in the US market as US firms, on average, offer better investment returns and profit margins compared with the rest of the world, says Grant Bowers, senior vice-president and portfolio manager at Franklin Equity Group.

Franklin Equity had assets under management of over US$135 billion (RM596.3 billion) as at December 2024.

That said, investors are advised to diversify beyond the Magnificent Seven mega-cap stocks into the large and mid-cap space with a focus on healthcare, financial, industrial, consumer and technology.

“One of the areas we’re finding opportunities is beyond the Magnificent Seven stocks. We like the Magnificent Seven stocks, but I think the market is bigger and broader. Generally the Magnificent Seven stocks still have very good businesses and are profitable. [But] for a bull market to continue, we need to see a broadening of the market,” he tells The Edge in an interview.

“Compared to the benchmark, we’re underweight the Magnificent Seven stocks. We own them and like them, but we are not as heavily focused on that. We think that having the ability to buy across the spectrum and diversify is very important. If you want exposure to the US equity market, taking a diversified approach is really the key.”

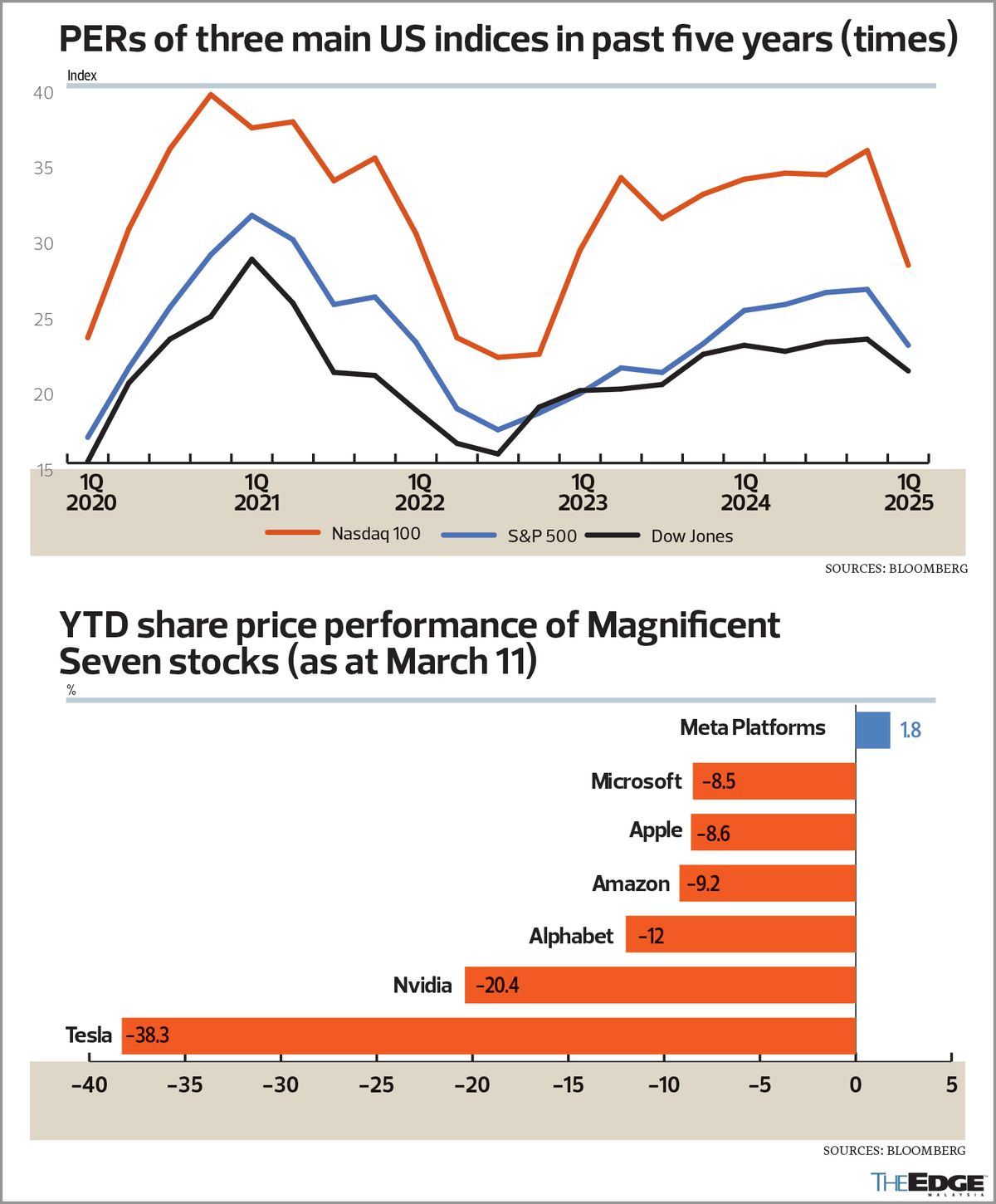

Prior to the market downward trend that started in mid-February, US equities had been the star performer, with the S&P 500 registering a one-year gain of more than 20%.

However, the recent trade war worries have sent the tech-heavy Nasdaq into a steep correction. For the year to March 11, six out of the Magnificent Seven were in the red — Tesla Inc (-38.3%), Nvidia Corp (-20.4%), Alphabet Inc (-12%), Amazon.com Inc (-9.2%), Apple Inc (-8.6%) and Microsoft Corp (-8.5%). Only Meta Platforms Inc registered a small positive return of 1.8%.

Consequently, the price-earnings ratio (PER) of the seven stocks has fallen to about 30 times, but is still higher than that of the S&P 500 (22.8 times), Dow Jones (21.1 times) and Nasdaq 100 (28.1 times).

Bowers acknowledges that US market valuations are not cheap, with its equities moving closer to their fair value.

“The road is not as easy as it was two years ago, but you have to remember that two years ago, every economist in the world was saying the US was going into a recession. And they didn’t get it right. In fact, the US market continued to move higher and did very well. So it’s tough to make predictions.”

Despite the market volatility brought about by US President Donald Trump’s tariffs and foreign policies, Bowers is of the view that the US economic outlook remains positive, as it is structurally and fundamentally healthy.

“We’ve seen some squishy data and a little bit of stress in the market in the last few weeks, but the reality is, the current view and the long-term view remains pretty well intact and consistent with the theme we’ve been seeing since last year.”

The US economy grew 2.3% in the last quarter of 2024, taking full-year expansion to 2.8%.

The tariff storm notwithstanding, Bower is optimistic some of these proposals can still be negotiated.

“If you go back and look at Trump’s first term as US president, there were a lot of proposals, but the end result was significantly less than proposed. I would say, right now, the market is working with that same assumption — a lot of these initial proposals that are really big in numbers and headline grabbing … will ultimately be negotiated down into smaller proposals.”

Encouraging growth rate seen for corporate earnings

Bowers is also not particularly concerned about the tariff impact on US corporate earnings, instead expecting them to grow “at an encouraging rate of 10% to 11%” this year.

“Historically, tariffs get passed through to the end users. So you would see more inflationary potential, rather than [their] being detrimental to corporate margins and profits. It’s yet to be seen how that will really play out.

“Trump, aside from the rhetoric, brings a very pro-business environment, with deregulatory policies and lower taxes. And that is really supportive of the US economy. I think, in general, that’s going to be a tailwind,” he opines.

Other supporting factors include ongoing investments in generative artificial intelligence (AI), healthcare innovation, the industrial renaissance as well as the reshoring of US industrial capacity.

“All these are going to be secular growth tailwinds for the market, and should continue to support stocks in general. So my advice to clients has always been, don’t try and time the market. The US is the biggest economy in the world. It doesn’t need to be your biggest position, but every investor should have some exposure to the US economy.”

In addition, he points out that profit margins of US corporates are well above the rest of the world’s.

“You look at returns on invested capital and the actual labour productivity. The US continues to move higher. Most other countries, especially post-Covid 19, have kind of stagnated. So I think there is a real case for why the US market has done so well in the last two years.”

For Bowers, the key risk for the US market is the inflationary risk arising from Trump’s policies.

“We don’t really know how the Trump administration’s plans are going to play out. Some of them could have an inflationary effect, and we should pay attention to inflation risks.”

He says the US Federal Reserve remains supportive of the economy, with one or two rate cuts projected this year. “I wouldn’t be surprised if we see another rate cut in the first half of the year, especially if we continue to see some of the data coming in a little bit soft. I think inflation probably remains a bit sticky, in the 3% range.”

In the 12 months through February, the US Consumer Price Index rose 2.8%.

Asked for his view on Chinese start-up DeepSeek, Bowers observes: “I would say it’s evolutionary, not revolutionary. I don’t think it should be perceived as a threat. It should be perceived as China not being left out of AI. China has an AI strategy, it’s just that they don’t have advanced computing power, so they are behind the US. DeepSeek doesn’t change that. I think what DeepSeek did was sort of wake up the world that China will be innovative with how they apply AI and investments in AI.”

Chinese tech giant Alibaba Group Holding Ltd, for instance, has said it will invest more than US$50 billion in AI and cloud computing over the next three years.

Meanwhile, Microsoft’s recent move to cancel a substantial amount of data centre capacity in the US has sparked speculation that there is an oversupply of data centres.

Bowers is unfazed by the oversupply concerns, noting that it is purely due to Microsoft’s focus shift within the AI space by adjusting its infrastructure in other areas. The company has said it plans to invest more than US$80 billion in AI this year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- UOB Kay Hian appoints Anne Leh as new CEO

- Gas Malaysia declares final dividend of 10.28 sen per share

- Kenneth Vun now MD at both Symphony Life and XOX

- Change of guard at Ekuinas — sources

- LSH Capital, Matrix Concepts, Symphony Life, Gamuda, Gas Malaysia, Kim Loong, United Malacca, MyNews, Marine & General, Dayang, Nestcon, Solarvest, Rohas Tecnic, Bintai Kinden