(Photo by 123RF)

This article first appeared in The Edge Malaysia Weekly on March 17, 2025 - March 23, 2025

GLOBAL market risks are tilting towards the wrong end of the spectrum amid elevated trade tensions between the US and a slew of countries, fuelling concerns of stagflation and recession risks in the world’s largest economy, notwithstanding US President Donald Trump’s pro-growth agenda.

At the White House last week, Trump was quick to downplay talk of a US economic recession so soon after gaining his second term as president. “I don’t see it at all. I think this country’s going to boom.”

In the latest round of tariff proposals, Trump vowed to impose a 200% tariff on European Union wine, in response to the EU’s retaliation against his steel and aluminium tariffs. On the other hand, he scrapped a plan to double US tariffs on Canadian steel and metal imports to 50% — even though a 25% tariff still took effect last Wednesday — after the Canadian province of Ontario suspended a 25% surcharge on electricity exports to the US.

Trump’s optimism aside, Sunway University Business School professor of economics Dr Yeah Kim Leng says global markets may have to brace for the eventuality of the US going into a recession due to increased uncertainties as well as the softening of its economy.

“Tariffs will result in higher prices and inflation, which will have an adverse knock-on impact on consumer spending. Then, the weak consumer sentiment will deteriorate further. The impact is not just on consumption, but also on the financial market, as corporate earnings are likely to decline. Even if the US does not fall into a recession, growth will likely be slower than the 2% to 3% in the past few years,” he tells The Edge.

When stagflation occurs, the US economy will see job losses and wage cuts, he observes, thus creating greater stress on households as well as businesses.

DBS Group Research chief economist Taimur Baig sees the probability of a US stagflation rising to between 30% and 35% this year.

“The highest probability scenario for the US is stagflation. We don’t necessarily mean the 1970s style [of stagflation] — the really terrible recessionary outcome and double-digit inflation. We’re not talking about that, but we certainly are talking about growth being below trend and inflation not going anywhere near the 2% mark that the US Fed (Federal Reserve) tries to convince everybody that it needs to see before it can cut rates,” he said in a webinar last Wednesday.

Having said that, Baig believes the underlying momentum in the US economy may help it avert a recession. “One quarter of negative growth is quite possible. For two consecutive quarters of negative growth, which is sort of justifying a recession, I’m not too sure about that. There was a lot of underlying momentum coming from 2024, which is still there in the US, with respect to helping the economic outlook. I wouldn’t be too much into the recessionary doom camp but, certainly, growth slows down just as inflation gets sticky.”

Concurring, JP Morgan chief global economist Bruce Kasman says the chances of a US recession rose to 40% from 30% at the start of the year. His current forecast for the US is for 2% gross domestic product (GDP) growth this year.

During the 1970s stagflation era, inflation failed to return to previous levels after the first oil shock in 1973, coupled with a US recession from 1973 to 1975. Inflation inched even higher, following a second oil shock in 1979, according to Deutsche Bank.

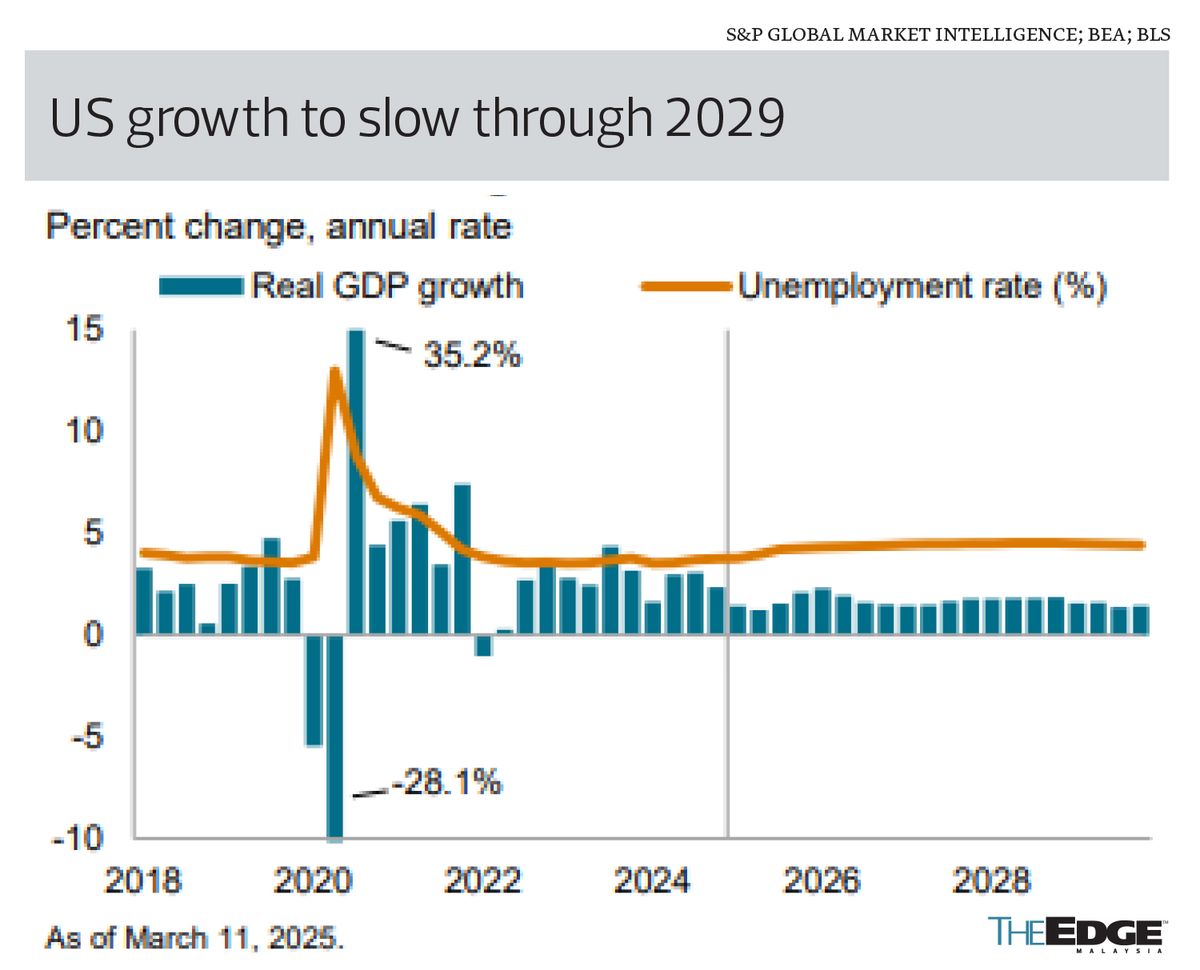

In 2024, US GDP grew 2.8%, and White House economic adviser Kevin Hassett expects growth to be at least 2% to 2.5% in the first quarter of 2025.

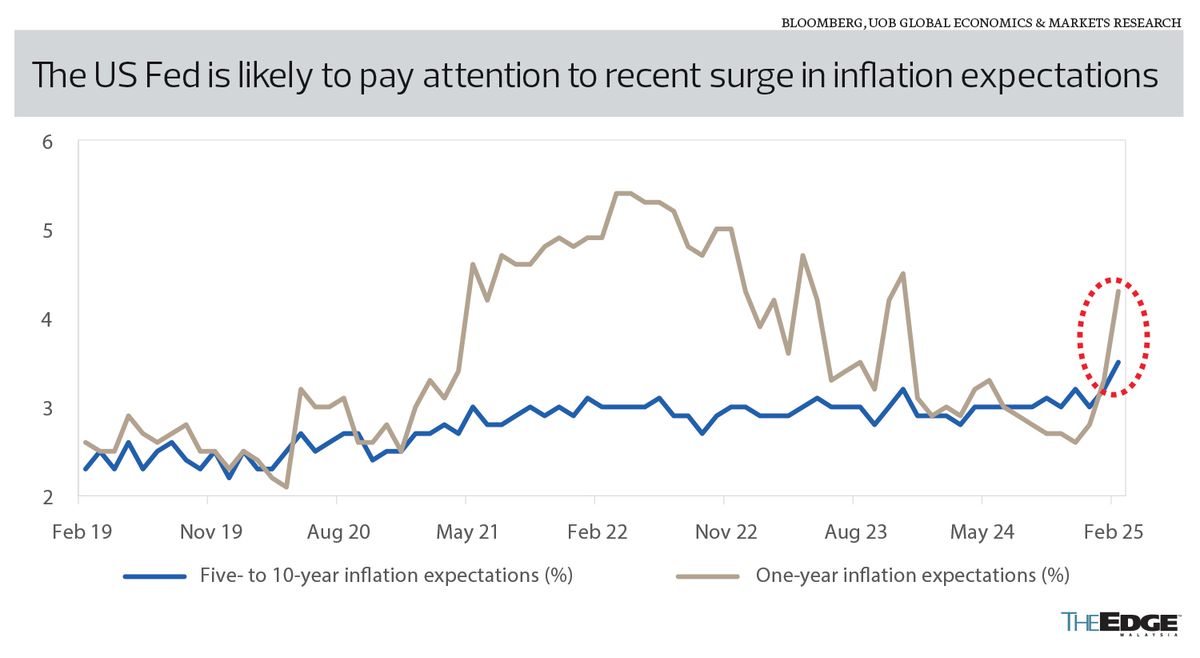

In the 12 months until February, the US Consumer Price Index increased by 2.8%, as prices increased moderately in February, giving the Fed room to keep interest rates unchanged, as the Federal Open Market Committee decision is due on March 19.

Some quarters say, however, that cooler inflation leaves the door open for the Fed to resume the rate easing cycle by mid-year. The current benchmark policy rate is in the 4.25%-to-4.5% range.

More positive on the US outlook, UOB Bank senior economist Julia Goh believes stagflation is unlikely to be a concern for now. “The combination of below-trend US economic growth and higher inflation risks due to Trump’s trade measures has raised the spectre of the US economy falling into stagflation. That is not our base case for now, but a rising risk that the US Fed may have to contend with in its policy formulation ahead.”

Although recent economic indicators and surveys suggest weakening optimism of US growth trajectory, coupled with rising price pressures, Goh is also keeping her US growth forecast at 1.8% in 2025, which is deemed more conservative.

“Risks to our forecast are dependent on the extent of Trump’s policies and risk has tilted to the downside, as tariffs are coming well ahead of US expansionary fiscal policies,” she says.

DBS Group Research’s Baig expects the Fed to implement only two rate cuts and not more than that even if the economy starts showing signs of weakness, as inflation remains a worry.

“In the best case, core inflation will be flat at 2.5% to 2.6%. I see no scenario in which they go lower,” he says.

According to Baig, another concern for the US economy is its household balance sheet. “Households burdened with high interest rates have been struggling, particularly the low end of the income spectrum. So, there’s certainly credit risk manifesting at the bottom 20% to 30% of households. On top of that, with inflation worries coming from tariffs and immigration and tax measures, it will add a significant amount of constraints on the government’s part to support the economy.”

Mitigating measures

To mitigate the repercussions of potential US stagflation and a recession, Sunway University Business School’s Yeah says a greater regional policy coordination — led by China — is required to ensure that the region’s fiscal and monetary policies as well as trade and investment flows remain supportive of growth.

“That means countries have to shift away from trade with the US and see how they can push trade and investment among themselves. We are quite confident that the Asian region has much greater potential. We can withstand the stress because of greater economic integration to create investments among member countries in the region,” he says.

Although it may look challenging for China to achieve its 5% growth target this year, Yeah says China could be supported by its investment relationship with many countries. “If China is able to increase its spending as it shifts towards domestic consumption, then other countries will also have greater opportunities to tap the Chinese market.”

UOB Bank’s Goh has adopted a more cautious stance on China, projecting 4.3% growth on the back of the ongoing trade war with the US. “Some upsides are likely from stronger monetary and fiscal stimulus support.”

Overall, she says, the impact of ongoing global developments on Malaysia will depend on the outcome of reciprocal tariffs in April and the extent of actual tariffs implemented.

“An escalation in trade retaliations as well as a weaker outlook among Malaysia’s key trade partners poses downside risks for Malaysia,” she cautions.

Globally, growth is projected to expand at 3.3% in 2025 and 2026, below the historical (2000 to 2019) average of 3.7%, according to the International Monetary Fund’s report released early this year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Gamuda says to sign several 'imminent' large contracts, as 2Q profit grows 4.8%

- UOB Kay Hian appoints Anne Leh as new CEO

- KLIA Master Plan under review, brick-and-mortar expansion on hold — MAHB

- Gas Malaysia declares final dividend of 10.28 sen per share

- Malaysia’s trade at risk amid US semiconductor tariffs, research group says

- Cops probing video, organisation suspected of promoting communist ideology

- Atlantic releases full Signal text chain on Houthi attacks

- Used cooking oil now main commodity in production of sustainable aviation fuel

- 14,000 pigs culled so far in Selangor to curb ASF outbreak, says Veterinary Services Dept

- Bursa Malaysia, subsidiaries to close for Hari Raya Aidilfitri