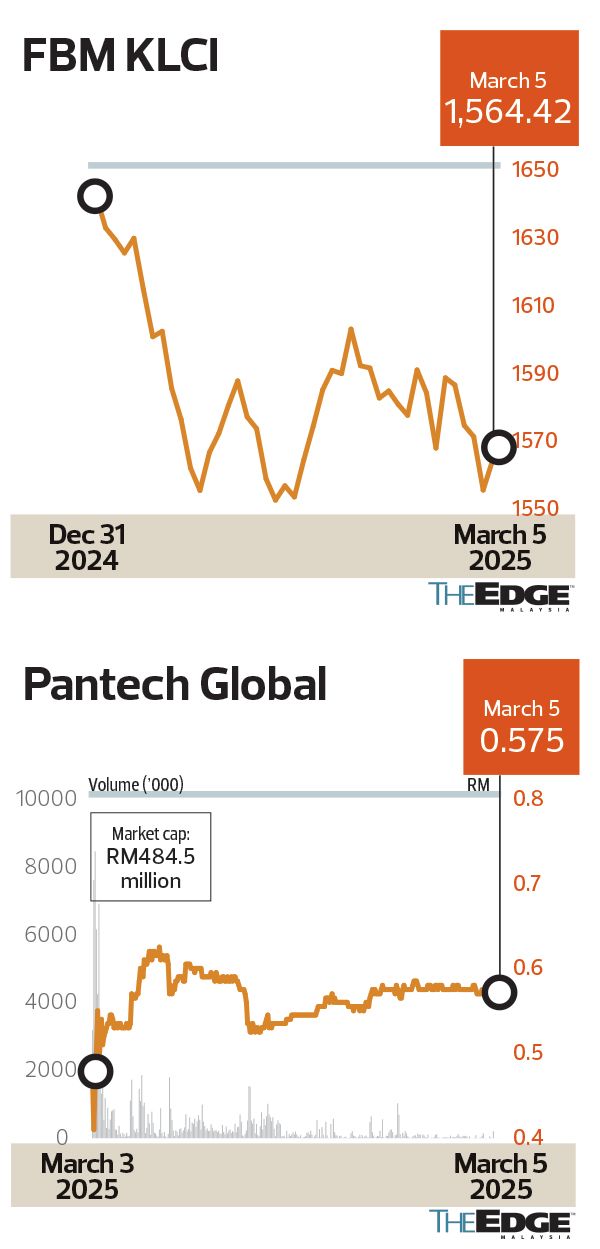

The FBM KLCI has lost 4.7% since the start of the year amid escalating global trade tensions and aggressive foreign investor sell-offs . (Photo by Suhaimi Yusuf/The Edge)

This article first appeared in Capital, The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

PANTECH Global Bhd’s (KL:PGLOBAL) underwhelming debut on the Main Market of Bursa Malaysia last Monday reflected the jitters in the market as it marked the first initial public offering (IPO) among nine so far this year to close below its issue price on day one. Market experts say that although the IPO pipeline at Bursa Malaysia is still resilient, uncertainties in financial markets may test the performance of upcoming IPOs.

Despite an impressive oversubscription rate of 44.83 times, the pipe, valve and fittings manufacturer’s share price opened at 46.5 sen in early trade before settling at 57.5 sen, marking a significant decrease from its IPO price of 68 sen.

The tepid reception comes against a backdrop of a declining FBM KLCI, which has lost 4.7% since the start of the year amid escalating global trade tensions and aggressive foreign investor sell-offs.

Market experts point to valuation and pricing concerns, particularly in a week when broader market sentiment was anything but forgiving.

January itself saw foreign investors offload RM3.1 billion worth of equities, the highest monthly net selling by foreign investors since 2020, according to CIMB Securities in a Feb 5 note.

In the subsequent four trading days after Feb 26, the FBM KLCI shed a further 2% to 1,555.66 points on March 4 following US President Donald Trump’s reiteration on March 3 that 25% tariffs on imports from Mexico and Canada would be implemented the next day. There is already an additional 10% tariff on Chinese exports to the US from February, putting the total levy on Chinese goods at 20%. All three responded with retaliatory tariffs.

In other Asian markets, Japan’s Nikkei 225 declined 1.2% to 37,331.18, Hong Kong’s Hang Seng Index dipped 0.28% to 22,941.77 and the Stock Exchange of Thailand fell 1.5% during the same period.

Market experts who have been watching IPOs closely have put Pantech Global’s dismal performance down to a matter of “valuation and pricing” during a “merciless week at the financial markets”. The company’s price-earnings ratio (PER) of 11.63 times based on its IPO price and FY2024 earnings is above the industry average of about 10 times.

Explaining the investment psyche during market turbulence, market experts tell The Edge that in a risk-off environment, investors tend to assign lower PER valuations to IPOs.

“For companies exposed to tariff risks, investors may project lower future earnings, anticipating that current earnings may not be sustainable. In Pantech Global’s case, its listing PER was 11 times [based on annualised FY2025 earnings], higher than other players in the steel and aluminium industry, which typically trade at nine to 10 times at best. This valuation premium, combined with tariff concerns [could have] contributed to its weak IPO performance,” says Tradeview Research director of investment advice Nurazlin A Samad.

Several other dealmakers have put Pantech Global’s debut disappointment to a pricing issue.

“If the parent company [Pantech Group Holdings Bhd (KL:PANTECH)] has a PER of only eight times, there’s no reason that its subsidiary should trade at a premium,” remarks a dealmaker who does not want to be named.

A number of other companies that were listed last year have not been spared in the challenging market conditions. Several of them saw their share price dip below their IPO price (see IPO table on Page 35).

Rakuten Trade head of equity sales Vincent Lau says, “It is difficult to watch. We have seen some counters dip even below territory during Covid-19, with technology stocks and small- to mid-cap counters bearing the brunt of the [foreign investor] sell-off.”

Having expressed disappointment in Pantech Global’s performance last Monday, the company’s group managing director Adrian Tan tells The Edge: “[Barring] soft market conditions and a knee-jerk reaction arising from announcements from the US, there could be some misconception about our business. We know that some investors may have lumped Pantech Global in with conventional steel companies. However, we operate much further downstream as we manufacture value-added steel products which are critical components in industrial fluid transmission systems.

“We understand that tariffs are a concern for the economy and industry, but I would like to emphasise that Pantech Global is not a commodity or steel company. When people think of steel companies, it usually refers to upstream producers of raw materials like billets, slabs or bars, which are highly sensitive to price fluctuations.

“Regarding the tariffs [by the US], they apply across the board to all countries. This puts everyone in the same boat, so to speak, and the playing field is level. Despite this, our price remains competitive, as the cost of manufacturing the same or similar products [as ours] in the US is much higher. This actually gives us an advantage rather than puts us at a disadvantage.”

He adds that the group is not reliant on “any single market”, given its business with 28 markets around the world, including Malaysia.

Tan says the group is looking to make inroads into the Middle East, North Africa and South America to mitigate overdependence on any single region and vulnerability to sudden policy changes.

IPOs with unique market positioning seen as attractive

For now, investors are concerned about what would become of upcoming IPOs. After all, the pipeline of about 52 more flotation exercises for 2025 has been a matter of interest to the investing community.

To this end, Tradeview Research’s Nurazlin maintains that IPOs with unique market positioning — “such as those in the domestic consumer sector, construction and e-commerce” — may attract higher investor interest.

As to whether IPOs would still be an attractive bet amid market volatility, Nurazlin says, “In a risk-off environment, weak global sentiment could trigger sell-offs across markets as investors lock in profits, raise cash for future opportunities or prepare for potential redemptions. Additionally, Malaysia and other Asean markets may serve as a funding source for Chinese stock purchases, particularly in thematic trades driven by artificial intelligence.

“That said, we believe Malaysian stocks remain fundamentally resilient, with limited direct impact from the US tariffs on Canada, Mexico and China. We recommend bargain-hunting once the market stabilises, while maintaining a healthy cash position in the meantime. While global growth may slow due to tariff implementations, central banks are prepared to support markets through rate cuts, potentially paving the way for a recovery in the coming months.”

Rakuten Trade’s Lau says, “I am still positive on IPOs, although we may see opening day gains dip to the 5% to 10% range compared to typical gains of 30% and higher.”

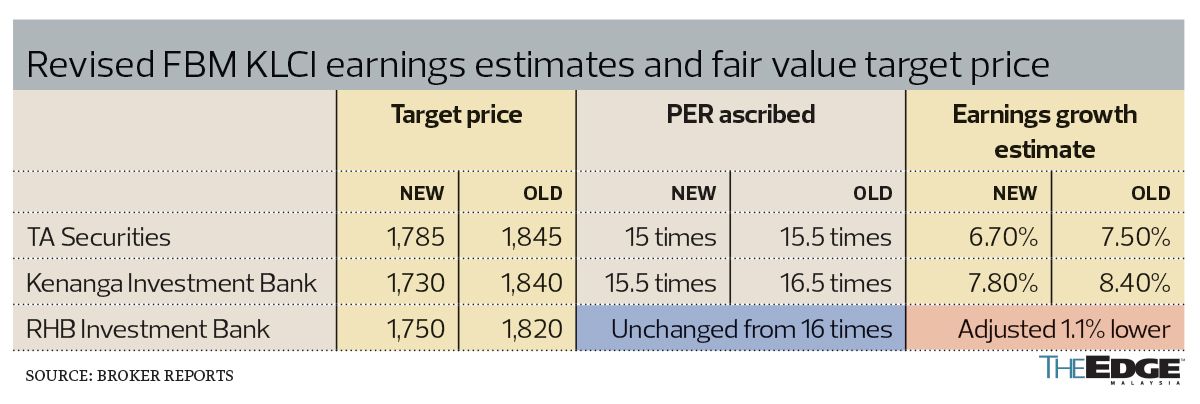

Given the volatility in financial markets so far this year, research houses last week lowered their earnings forecasts and year-end targets for the FBM KLCI due to a weak earnings outlook and sentiment, with TA Securities cautioning that the benchmark will likely continue consolidating, with a negative outlook in the short term as investors monitor Trump’s tariff increases. And this is in spite of the hint of relief seen last Tuesday after US Commerce Secretary Howard Lutnick suggested that the Trump administration may “walk back” some tariffs that had sparked the global sell-off in markets.

At this juncture, some analysts are hopeful that the US will announce a pathway for tax relief for Canada and Mexico, which could alleviate the hefty levy on imports.

For now, TA Securities, Kenanga Investment Bank and RHB Investment Bank have lowered their year-end targets for the FBM KLCI to below 1,800 points. TA Securities and Kenanga Investment Bank lowered both earnings forecasts and PERs, while RHB Investment Bank’s cut was due to an earnings downgrade.

Amid jitters in the broader market, Kenanga Research reiterates in a March 5 note that the banking sector is still a safe bet, explaining that its “overweight” stance on the sector is due to more writebacks as overall staging improved with record low gross impaired loans of 1.44% in December last year.

The research house says most banks point towards higher credit cost — with the exception of RHB Bank Bhd (KL:RHBBANK) and MBSB Bhd (KL:MBSB) — to normalise from writebacks seen over the years.

“That said, initial expectations for the sector still ascribe a net positive improvement to return on equity, which makes the banking sector one of the sparse safe spaces for growth,” said RHB Research, whose top sector picks are AMMB Holdings Bhd (KL:AMBANK) with an “outperform” call and target price (TP) of RM6.80 for its rising ROE prospects and growing dividend yield potential “which may set it apart from other high yielders”.

“Among the large-cap banks, we like Malayan Banking Bhd (KL:MAYBANK) (TP: RM12) because, despite its leading market share, it holds better-than-industry asset quality with earnings growth expected to outpace that of its counterparts,” it adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Special Report: Dispelling aspersions surrounding EPF’s impressive 6.3% dividend for 2024

- Pharmaniaga’s RM653.52m cash call gets shareholder nod

- SC to introduce new fee structure to increase revenue in 2026

- Cahya Mata Sarawak sues deputy chairman Abu Bekir Taib, five others over failed project

- Top Glove targets stronger sales in 2HFY2025, fuelled by improved conditions in US market

- Lloyd’s Register to sell modern tower and return to Victorian HQ

- Salcon, Scanwolf, Reservoir Link, Pharmaniaga, IJM, Lagenda Properties, Land & General, Hextar Global, Top Glove, Cahya Mata Sarawak, Iskandar Waterfront City

- Mulino dismisses reports of US military evaluating Panama Canal options

- AI cloud hosting firm CoreWeave launches US$2.7 bil IPO

- At least 91 killed in Gaza as Israel abandons ceasefire, orders evacuation