This article first appeared in The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

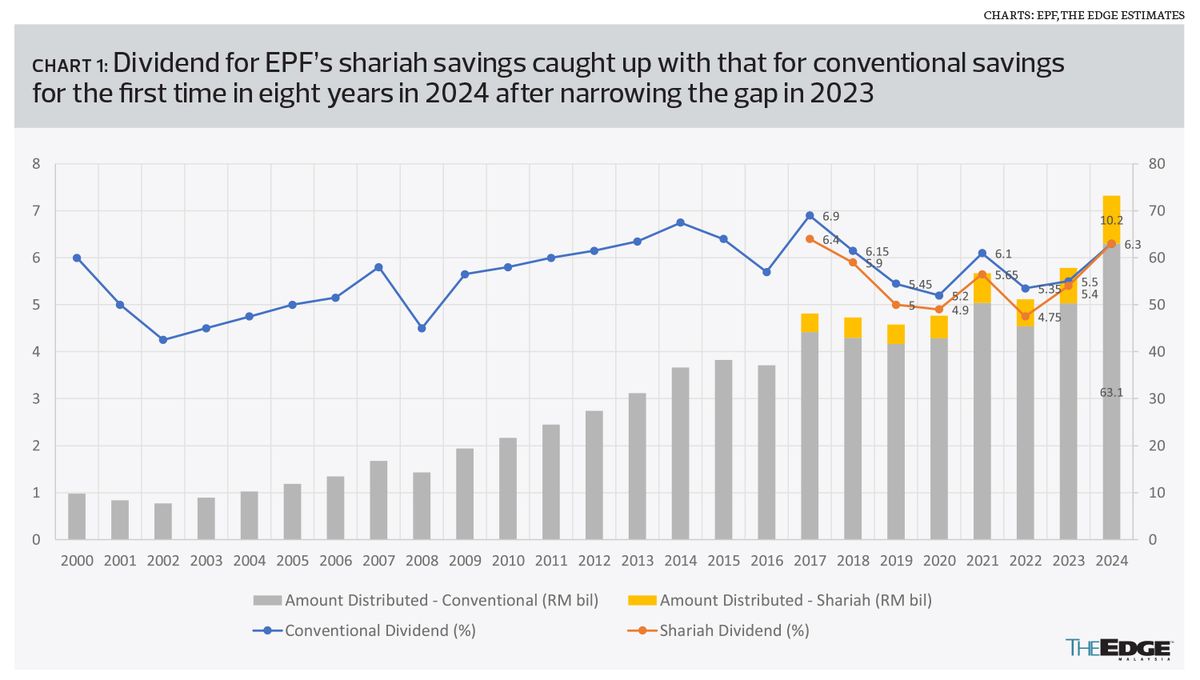

THERE is no denying that the Employees Provident Fund’s (EPF) 6.3% dividend declared for both conventional savings and shariah savings for 2024 is nothing short of spectacular and would have been celebrated with more vigour — if not for the lingering questions surrounding its seemingly untimely sale of Malaysia Airports Holdings Bhd (MAHB) shares in 2023.

At least two members of parliament questioned the size of EPF’s dividend payout of RM73.24 billion in 2024, which represents 98.4% of its RM74.46 billion investment income that year — a significantly higher ratio compared to 2023 (the RM57.81 billion payout was below 90% of the headline investment income that year). The observation that there were “other motivations” was also voiced on social media hours after the EPF declared dividend rates that exceeded most expectations.

The issue with this comparison lies, however, not only in the 2024 figures but also in the 2023 figures, as EPF is expected to pay out all realised income to members as dividends annually, after deducting costs — more on this later.

For the record, EPF’s 2024 dividend performance was near the upper end of projections by The Edge in November. Our back-of-the-envelope calculations had shown the EPF dividend for 2024 coming in between 5.4% and 6.4% for conventional savings and between 5.5% and 6.5% for shariah savings. (Scan the QR code to read the article “EPF’s 2024 shariah dividend may exceed 6%, beat conventional savings”, The Edge, Issue 1550, Nov 18, 2024.)

Six months ago, The Edge projected that EPF dividends for 2024 could exceed 6%. (Scan the QR code to read the article “EPF’s 2024 dividend could hit 6% if 2H performs as well as 1H”, The Edge, Issue 1537, Aug 19, 2024.)

Three months ago, The Edge had projected that EPF’s dividend for shariah savings would exceed 6%, possibly even beating conventional savings, following strong performance in the first nine months of the year. This is the first time since shariah savings was introduced in 2017 that the dividend for shariah savings has equalled that for conventional savings (see Chart 1).

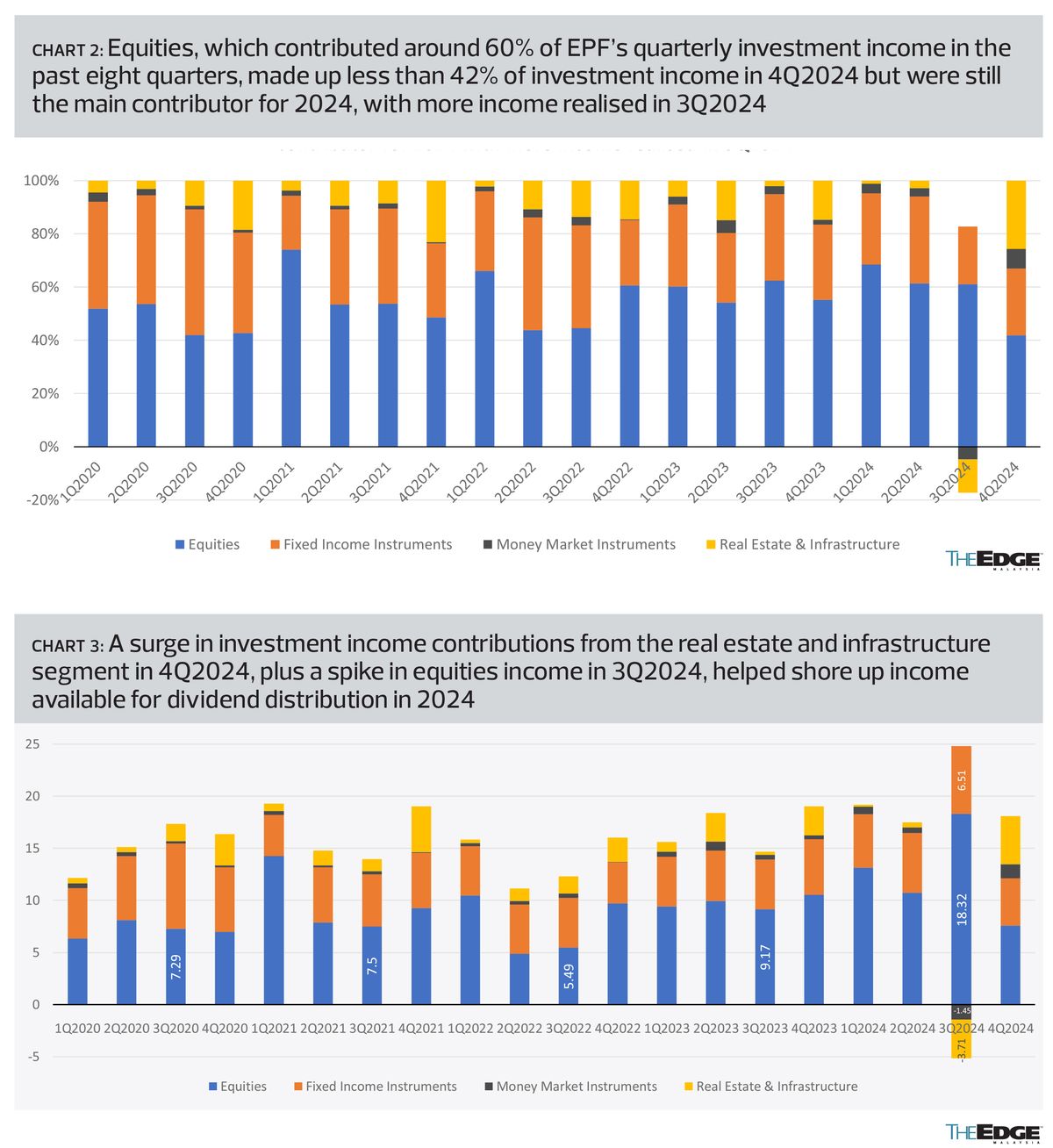

While The Edge suggested the dividend for conventional savings could still hit 6%, our reservations were due to anecdotal evidence of strong growth in its fund size — which shores up the amount EPF needs to pay for every 1% of dividend to members — amid potential surprises in a challenging external environment. EPF also reported RM5.16 billion in foreign exchange translation losses at its real estate and infrastructure as well as money market portfolios in the third quarter as the ringgit appreciated against the US dollar, which perhaps necessitated a more aggressive profit-taking stance in its equities portfolio to boost overall figures.

Also shoring up income available for dividend distribution in 2024 was a surge in realised income in the real estate and infrastructure segment in 4Q2024, which probably contributed a quarter of investment income, just above contributions from the fixed income segment, our back-of-the-envelope calculations showed (see Charts 2 and 3).

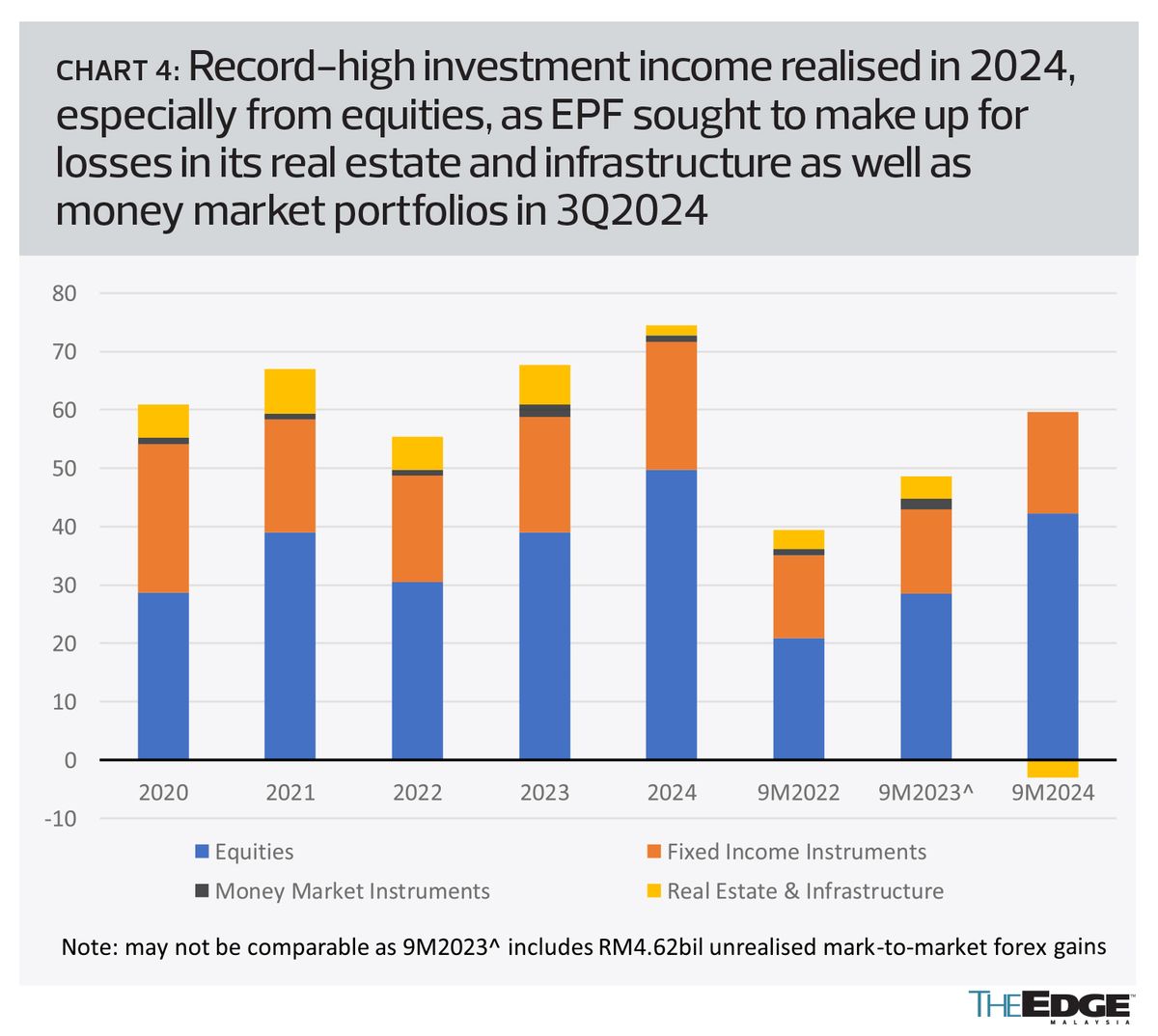

Equities, which contributed some 60% of quarterly investment income on average in the past eight quarters, contributed only about 42% of investment income in 4Q2024. Even so, with equities making up 93% of investment income in 3Q2024, equities continue to contribute two-thirds of investment income in 2024 while 29% came from the fixed income instruments, where annual returns were 4.27% last year (see Chart 4).

A reflection of a higher risk profile, return on investment (ROI) for equities was 9.9% while private equities (10% of equity investments) generated 11.3% returns. ROI for the real estate and infrastructure segment was 5.13% “on a constant currency basis” and 1.89% from money market instruments.

Strength of 2024 payout

As expected, EPF’s total dividend payout was at a new record high in 2024, even as its investment assets grew 10% year-on-year to RM1.25 trillion at end-2024, from RM1.14 trillion at end-2023, driven by portfolio income as well as roughly RM50 billion in net contributions (RM118 billion gross contributions less RM68 billion withdrawals).

EPF paid a total of RM73.24 billion in dividends for 2024, with RM63.05 billion allocated to conventional savings and RM10.19 billion to shariah savings. This compares to a total dividend of RM57.81 billion in 2023, with RM50.3 billion allocated to conventional savings and RM7.48 billion to shariah savings.

While a 6.3% headline dividend for 2024 — a seven-year high — pales in comparison with the 6.9% declared for conventional savings and 6.4% declared for shariah savings in 2017, it is worth noting that the total dividend of RM48.13 billion declared in 2017 (RM44.2 billion for conventional savings and RM3.98 billion for shariah savings) is only enough to pay just over 4% of dividends in 2024.

Conversely, the RM73.24 billion total dividend payout for 2024 would have been enough to pay just over 10% of dividends in 2017.

Overseas assets made up 37% of EPF’s total assets in 2024 but contributed RM37.44 billion, or 50.3%, in investment income last year.

Asked to comment on speculation that EPF’s high dividends for 2024 were somehow politically motivated, the provident fund says: “EPF maintains a high degree of independence in its investment activities, guided by its Strategic Asset Allocation framework to ensure a well-diversified and resilient portfolio. The 6.3% dividend declared for both conventional savings and shariah savings is driven purely by strong investment performance and realised income, with no external pressure or political influence.”

As for the variance in the payout ratio between 2023 and 2024, EPF explains: “The payout ratio varies each year, as it reflects the proportion of the total investment income that is distributed while unrealised income, which is not included in dividend distribution, remains in the fund. In 2023, unrealised income was RM5.72 billion, which cannot be distributed as dividend, given its unrealised nature.”

Indeed, EPF needs to take profit on its investments at some point, as annual dividends can be declared only on realised income and not paper profits.

“As with every year, the dividend rate was thoroughly reviewed and approved by the EPF Board and Investment Panel, both of which uphold strict governance, transparency and accountability in their decision-making. EPF’s priority remains the sustainable growth of members’ retirement savings, and we will continue to adhere to our disciplined investment approach to deliver long-term value,” it tells The Edge.

In its statement dated March 1, EPF had noted that it had “fully separated” its conventional and shariah savings portfolios, which “allows each portfolio to optimise its returns over the long term through an independent strategic asset allocation. The separation also enhances diversification, ensuring that assets under both [conventional and shariah savings] are well distributed across asset classes, geographies, markets and industries for sustainable returns”.

When announcing the 6.3% dividend rate for 2024 on March 1, EPF CEO Ahmad Zulqarnain Onn took care to temper expectations on future dividends also coming above the 6% mark, asking that its 16 million members and the general public “understand that the market will go up and down” and not to be “caught up with the strong market growth” in any given year.

It is certainly no mean feat for EPF to deliver even a 5% annual return, let alone 6%, given the need to safeguard members’ retirement savings while looking for pockets of opportunities to deliver growth. Whether or not it had dipped into the “cookie jar” of unrealised profits to deliver the impressive 6.3% dividend for 2024, EPF will need to continuously replenish that “jar” to sustainably meet the ever-growing dividend expectations as its fund size doubles every decade.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Capital A to proceed with distribution plans after court confirms share capital reduction

- Alliance Bank proposes renounceable rights issue of shares to raise RM600m

- Alliance Bank, Crest Builder, Capital A, AirAsia X, Nestlé, DRB-Hicom, VS Industry, Genting, Salcon, Erdasan, CelcomDigi

- RM1.06b meth seized at West Port in Malaysia's largest-ever drug bust

- Fed's Powell says Trump can’t fire him. That might change

- Former Sabah minister Peter Anthony seeks to review Court of Appeal's decision

- Terengganu was allocated RM1.84 bil for development this year — PM

- Nga tells the people to reject divisive voices that threaten multiracial unity

- China backs Malaysia’s Asean leadership, prioritises ACFTA 3.0

- UAE to pledge US$1.4 tril in US investment after Trump meeting