KUALA LUMPUR (Feb 24): Analysts are growing optimistic about MISC Bhd (KL:MISC), with at least one issuing an upgrade on the stock, after recent softness in share price.

This positive sentiment stems from a combination of factors, including favourable risk-reward metrics, an attractive dividend yield, and the expectation of earnings growth, particularly in the offshore and petroleum segments.

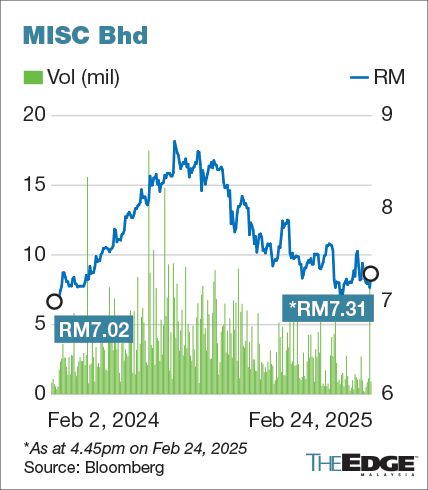

According to Bloomberg, in the last six months, MISC shares declined by 14%.

At the time of writing on Monday, MISC shares were up 10 sen or 1.4% at RM7.25, valuing the company at RM32.36 billion.

In a note on Monday, Hong Leong Investment Bank (HLIB) said MISC's recently announced FY2024 results aligned with the firm’s projections, but fell slightly short of consensus.

Despite this modest underperformance, HLIB revised its stance on MISC from "hold" to "buy", citing the stock’s attractive risk-reward proposition.

The research house remains optimistic about MISC’s earnings trajectory, underpinned by expected growth in its offshore and petroleum operations for FY2025.

In addition, HLIB noted that at current levels, MISC offers a commendable dividend yield of approximately 5%, which should provide investors with a reasonable buffer against downside risks.

TA Securities echoed a similar sentiment, noting that MISC's full-year results were in line with its own expectations.

In light of the recent decline in MISC's share price, the research house has revised its rating on the stock from "hold" to "buy," maintaining a target price of RM8.40 per share.

This target is based on a 16.5 times multiple of the company's projected calendar year 2025 (CY2025) earnings per share, with an additional 5% premium applied for environmental, social, and governance (ESG) factors.

The research house added that should market values improve, MISC has the opportunity to adjust the net book value accordingly.

TA Securities underscored that despite short-term headwinds, the long-term fundamentals of MISC remain intact, with solid contributions anticipated from the company's core offshore and petroleum segments.

“The medium-term outlook for the offshore segment remains optimistic, supported by stable oil prices and ongoing demand for newbuild floating production storage and offloading (FPSO) units across South America, West Africa, and the Asia-Pacific.

“Continued revenue generation from existing long-term contracts and projects in the commissioning phase will further strengthen this segment’s financial performance,” said TA Securities.

In a separate note, RHB Research, while acknowledging a miss in MISC's FY2024 results due to weaker-than-expected performance in the gas segment, remained broadly positive on the stock's prospects.

RHB pointed out that the stock is now trading at a level that is one standard deviation below its five-year mean, rendering it undervalued relative to historical performance.

RHB continues to favour MISC’s robust operating cash flow and solid balance sheet, which positions the company well to capitalise on new growth opportunities, particularly in the FPSO market.

On the petroleum front, the research house is of the view that although crude tanker spot rates in the second half of 2024 were weaker compared to the first half, primarily due to reduced demand from China and production cuts by the Organization of the Petroleum Exporting Countries and its allies (Opec+), the broader outlook for the tanker market remains optimistic.

This positive sentiment is underpinned by robust exports from the Atlantic, growing crude imports in Asia, and a shrinking newbuild order book.

RHB has revised its FY2025 earnings forecast for MISC downwards by 2.3%, reflecting a more cautious outlook for the gas segment.

Despite this adjustment, the research house has raised its target price to RM9.70 from RM9.27, incorporating the latest net debt figures, while maintaining a 4% ESG discount based on an ESG score of 2.8.

MISC continues to maintain a solid balance sheet, the research house said, with its net gearing improving to 0.23 times from 0.25 times, following the successful repayment of borrowings.

MISC reported a RM446.2 million net loss for 4QFY2024, due to higher asset writedowns and a 23% revenue drop.

The company expects a soft liquefied natural gas carrier market in 2025, with recovery after 2026, while the tanker market outlook remains positive, supported by strong demand and stable petroleum shipping earnings.

- Mr DIY founder Tan Yu Yeh relinquishes vice chairman post, to serve as adviser

- 50,000 Malaysian jobs at risk, business chamber warns as it calls for urgent US tariff mitigation council

- Malaysia refutes 47% US import tariff claim, takes measures to prioritise well-being of businesses and people

- Trump hits China tariff retaliation, says policy will remain

- China retaliation on US farm goods hits soybeans, bolstering Brazil

- ‘Worst-case scenario’ for tech wipes $1.4 trillion from Nasdaq

- Anwar says impact of latest US tariff on nation's economy still being assessed

- Tok Mat, Rubio discuss bilateral relations, Asean-US Special Summit date

- US solar’s hoarding habit will help blunt sting from Trump tariffs

- Wall Street rout drags Nasdaq near bear market