(From left) Henry Butcher Malaysia Solutions Sdn Bhd director Fahariah Abd Wahab, Henry Butcher Malaysia (Sel) Sdn Bhd director Datuk Desmond Tew, Henry Butcher Malaysia Sdn Bhd group managing director Long Tian Chek, Henry Butcher Real Estate Sdn Bhd COO Tang Chee Meng, Henry Butcher Malaysia (Pontian) Sdn Bhd director Cheng Wui Kiang, and Henry Butcher Malaysia (Seberang Perai) Sdn Bhd associate director Fook Tone Huat at the launch of the HB Perspective: Malaysia Property Outlook 2025 report.

This article first appeared in City & Country, The Edge Malaysia Weekly on February 17, 2025 - February 23, 2025

The property market’s industrial and residential subsectors will be the top two performers for 2025 barring any unforeseen circumstances, according to Henry Butcher Malaysia during the launch of its HB Perspective: Malaysia Property Outlook 2025 report on Jan 22.

The consultancy’s chief operating officer Tang Chee Meng said: “We believe that the industrial subsector will continue to lead in terms of market performance, unless US President Donald Trump comes in with a lot of restrictions that will jeopardise all the supply chains, and the Malaysian government’s ambition of making the country a regional centre of chip design and manufacturing fails.

“Otherwise, we believe the industrial subsector will continue to lead the way in terms of performance … especially when you look at the past year, when big multinationals like Google and Microsoft announced plans to set up base here.

“The residential subsector has always been the mainstay of the property market. It usually contributes 65% of total transactions in terms of numbers. We believe it will most probably be the second subsector to do well.”

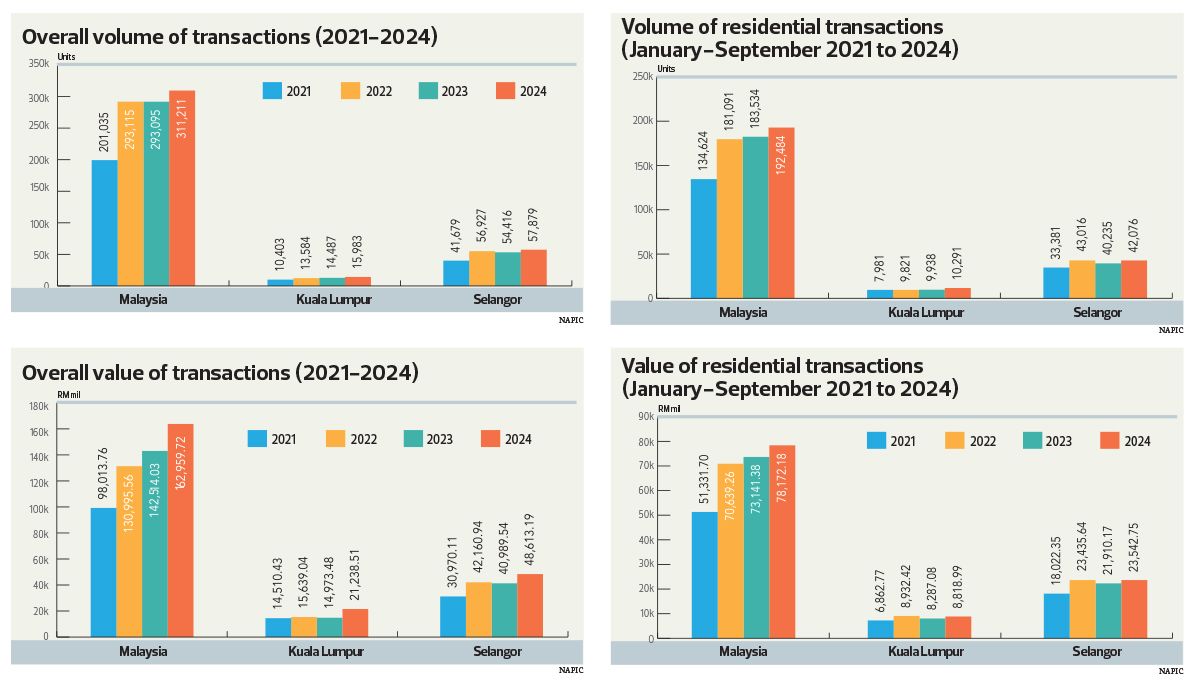

According to Tang, details mentioned in the report are for the first nine months of 2024 (9M2024) as the data from the National Property Information Centre for the final quarter has not been published yet.

“However, our projections and opinions on the outlook don’t depend on these statistics as we consider several factors, such as the economy, investments, political climate, government infrastructure projects and what is happening overseas, before coming to a conclusion,” Tang prefaced before sharing the highlights of the report.

Residential uptick expected

Tang highlighted several factors for the positive outlook on the residential subsector. These include Bank Negara Malaysia’s overnight policy rate remaining at 3%, landbanking activities by property developers, the increase in the minimum wage rate to RM1,700 per month, the tabling of the Urban Renewal Act, the flat 4% stamp duty for foreigners and companies, the digitalisation of the property industry and the numerous infrastructure projects, as well as foreign direct investment (FDI) coming into the country, and the stable government.

“Based on all these factors and not only the statistics, we are confident that the residential property market will be stable and will continue to enjoy steady growth in 2025,” he said.

“There is a possibility that house prices may increase as developers try to recoup the extra costs incurred due to higher building material costs, construction costs and so on as there is a limit to how much the developers can absorb.

“Rehda (Real Estate and Housing Developers’ Association) Malaysia has announced that its members are thinking of increasing prices this year. Of course, the extent of the increase depends on the state of the market. If the market is good, they can raise the price higher, but if the market is so-so, they may have to avoid increasing prices at too fast a pace.

“Overall, we feel the focus for 2025 will still be on landed residential properties because this is the main preference for most Malaysians.”

Affordably-priced high-rise apartments in major towns and cities, especially in the more popular or high-growth locations, will also see demand. Buyers will give eco-friendly homes that have green building standards a look-over and innovative projects in terms of concepts, design and themes will stand out from the pack, he highlighted.

Incidentally, there is a shortage of high-end products as launches have been limited, Tang said. While this might be seen as a gap in the market, developers need to consider various factors.

“Any developer launching this kind of project should be very careful. It has to be in a location that people want to invest in and the design and the pricing must also be right,” he cautioned.

Zeroing in on several states, Tang pointed to Johor with the Johor-Singapore Special Economic Zone (JS-SEZ) as a game changer for the southern state by boosting residential, commercial and industrial subsectors. It could possibly rival the Klang Valley in 10 years, Tang said.

Residential units on Penang Island, along with other types of property, will receive a boost with the implementation of the Mutiara LRT line, which will link George Town city centre to Bayan Lepas and extend to Seberang Perai on the mainland.

In Selangor, state policies such as Integrated Development Region in South Selangor (IDRISS), Smart Selangor Action Plan (SSAP), Selangor Agenda for Green Economy (SAGE) and Rancangan Selangor Pertama (RS-1) will help drive the economy and thus benefit the property market.

Data-oiled industrial sector

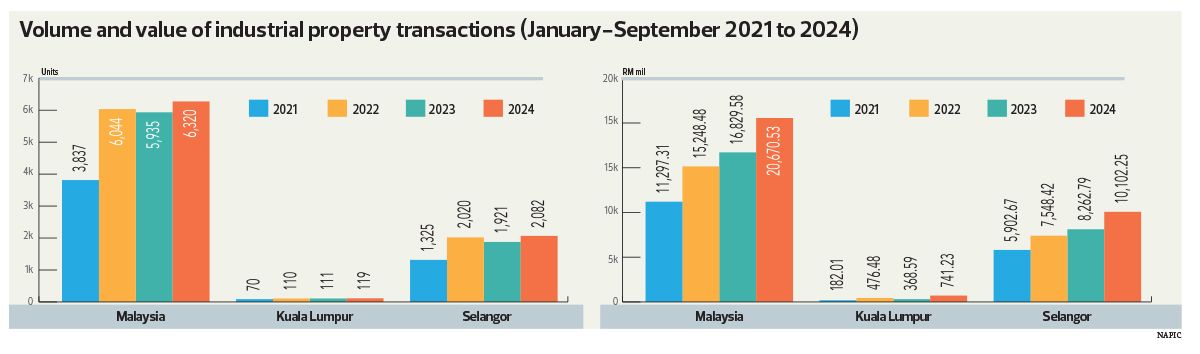

Looking ahead, the industrial subsector will see plenty of positives with the focus on data centres. Furthermore, increased FDIs and direct domestic investments from the previous year will continue to boost this subsector’s growth, Tang stated.

“The hottest topic in the industrial property subsector is data centres. We are seeing more and more of such centres being built mainly in Johor and in Selangor. The government has announced they will be focusing a lot on data centres and also chip design and manufacturing,” he said.

He also pointed to the infrastructure projects in Johor and Penang that will boost the subsector, giving investors a reason to set up factories there.

Tang added that the government’s New Industrial Master Plan 2030 and the National Energy Transition Roadmap will bolster the manufacturing subsector, and policies and programmes such as Industry4WRD, IDRISS and JS-SEZ will have a positive impact on the industrial sector.

However, the new Trump administration could put a spanner in the works, although it is too early to say if that will be the case.

“The Trump 2.0 administration is expected to adopt a protectionist policy and various tariffs will be imposed on imports into the US. This will likely affect countries deemed to be not supportive of the US’ efforts to support the US dollar as well as the domestic economy, and this will include China as well as BRIC members, of which Malaysia has recently been admitted as a partner country.

“However, Malaysia may be able to benefit from some rerouting of Chinese manufacturing activities to the country to enjoy lower tariff rates than direct Chinese exports to the US,” he said.

KLCC offices perform well

Tang highlighted that the KL city centre purpose-built office (PBO) occupancy rate in the 9M2024 period outperformed those outside the city centre.

“The occupancy rate of PBOs in the city centre was 72%, which is better than the 63.2% recorded by PBOs outside the city centre. But this trend may change a bit because some companies may feel that in terms of rental, it is better to shift to where the rental is cheaper and not having to come into the city, which is congested,” he said.

With the introduction of mega office tower projects over the past few years, such as The Exchange 106 and Merdeka 118, it has raised concerns of oversupply, although that is yet a certainty, said Tang.

Moreover, with the incoming office supply, the performance of older office buildings will be affected.

“With all this office space coming onstream, older buildings that have not undergone any upgrading or renovation will lose out in terms of retaining tenants and attracting new ones because these new buildings have better facilities with higher specifications. Rent-wise, as the market isn’t that fantastic, the differential isn’t that much. So, you have a situation where tenants are shifting to quality buildings at slightly higher rentals. Owners of all these older buildings, unless they are renovated or repurposed into something else — for example, hotels or serviced apartments — will find they are losing out in the longer term,” he said.

Tang added that if Malaysia’s economic growth goes according to plan and more multinational corporations come in with environmental, social and governance (ESG) specifications for their buildings, it will impact demand for office space and further reduce interest in older buildings.

The country’s total supply of PBOs stood at 18.82 million sq m as at 3Q2024, up slightly from 18.39 million sq m from the same period last year, while the occupancy rate dropped to 71.6% from 72.7% for the same period.

“For KL, PBO space has gone up to 9.657 million sq m as at 3Q2024, of which about 7.554 million sq m or 78% of total supply is located in the city centre. For Selangor, the supply of PBOs is 4.352 million sq m and the occupancy rate has gone up to 71.6% from 70.2% a year ago.

“For Penang, the supply of PBOs is 811,060 sq m. Occupancy rate is better than the national average, at 77.8%. Now 71% of these office spaces are located within George Town and these office spaces have enjoyed higher occupancy rates of above 80% compared to the rest of the state,” he said.

Retail and hospitality on an even keel

The retail subsector is forecast to have a 4% growth rate in 2025. The biggest challenge to this subsector is the rising cost of living, which will influence consumer spending on non-essential items and dining out. Moreover, sales tax was increased to 8% from 6% from March last year, leading to a hike in prices for retail goods and services. This will affect retail spending, Tang highlighted. There is a silver lining, though.

“The Malaysian government increased the remuneration of civil servants from Dec 1, 2024 and these increments should stimulate retail sales during the year-end holidays. The government has also increased the minimum wage from RM1,500 to RM1,700 effective Feb 1, 2025. This will put more disposable income in the hands of consumers and could benefit the retail sector,” he said.

Meanwhile, as at 3Q2024, the Klang Valley — covering Kuala Lumpur, Selangor and Putrajaya — had 290 shopping centres with a total supply of more than 88 million sq ft. The average occupancy rate in KL improved to 78%, Selangor remained unchanged at 73.8% and Putrajaya increased to 76.1%.

Tang said that the weak Malaysian ringgit may encourage international tourists to spend more during their visits, while the high cost of airfares will spur Malaysians to spend their holidays in the country. These will also benefit the hospitality industry.

Last year, the average occupancy rate of hotels in Malaysia in the first six months of 2024 was recorded at 52.6% compared with 50.5% the year before. All states recorded an increase in average occupancy rates, with the highest occupancy rate recorded by Pahang (74.6%), followed by KL (60.3%) and Penang (53.5%).

Tang believes that the hospitality industry will perform well due to several factors. First, the 30-day visa-free initiative for China and India nationals under the Malaysia Visa Liberalisation Plan has been extended to Dec 31, 2026. Also, Asean citizens are currently allowed to stay for more than a month without a visa, according to Tang.

Next year has been designated Visit Malaysia Year and the government is aiming for 26.1 million tourist arrivals with an estimated domestic spending of RM97.6 billion.

Furthermore, financial allocation has also been made for tourism activities.

“In Budget 2025, RM550 million has been earmarked for the Asean Tourism Forum 2025 and Visit Malaysia Year 2026. An additional RM110 million has been allocated for ecotourism.

“The government will also be promoting medical tourism as part of its plans to boost tourist arrivals in the country,” Tang said.

However, one key challenge remains with labour shortage. “The shortage, which has plagued the country, is a major issue faced by the hospitality industry. If the government does not resolve this, it will continue to hamper the recovery and growth of the hospitality industry,” Tang highlighted.

He added that hotels are not in favour of an announcement on earlier check-in times and the labour crunch will make things worse as hotel operators will not have time to ready the rooms for guests.

Despite this, Tang believes that the hospitality industry will fare well in 2025.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Gamuda says to sign several 'imminent' large contracts, as 2Q profit grows 4.8%

- UOB Kay Hian appoints Anne Leh as new CEO

- KLIA Master Plan under review, brick-and-mortar expansion on hold — MAHB

- Gas Malaysia declares final dividend of 10.28 sen per share

- Malaysia’s trade at risk amid US semiconductor tariffs, research group says

- Cops probing video, organisation suspected of promoting communist ideology

- Atlantic releases full Signal text chain on Houthi attacks

- Used cooking oil now main commodity in production of sustainable aviation fuel

- 14,000 pigs culled so far in Selangor to curb ASF outbreak, says Veterinary Services Dept

- Bursa Malaysia, subsidiaries to close for Hari Raya Aidilfitri