Photo by Kenny Yap/The Edge

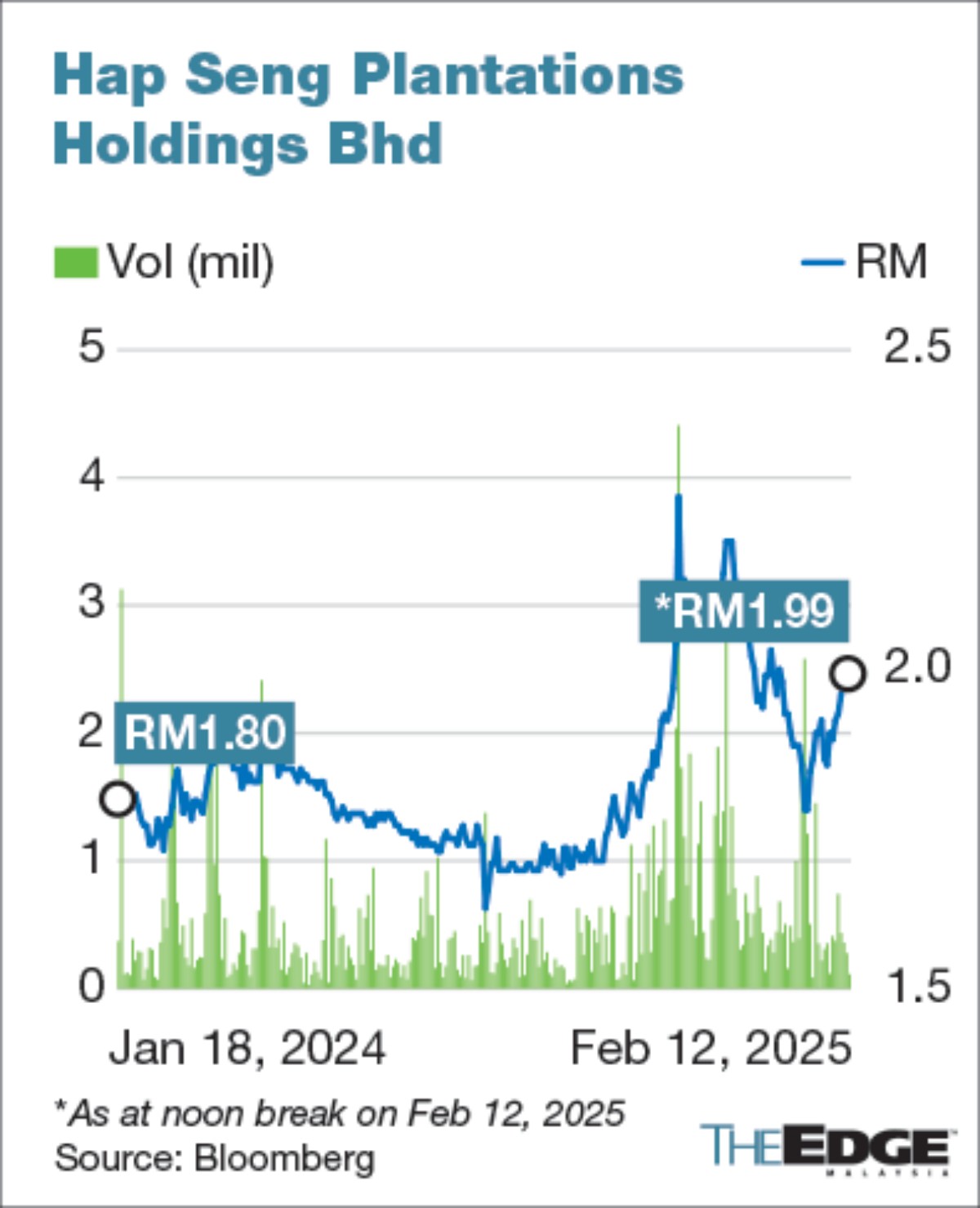

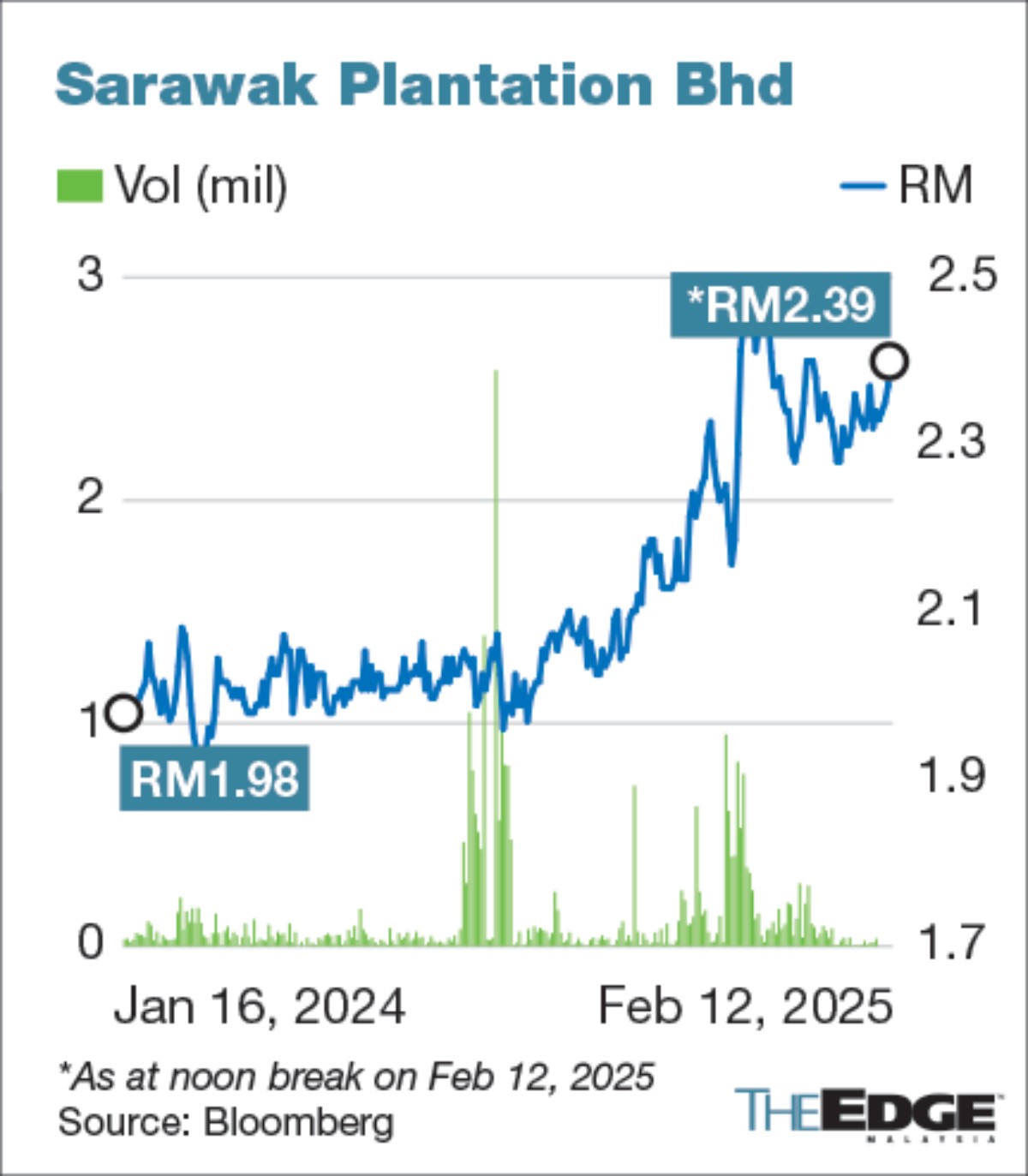

KUALA LUMPUR (Feb 12): BIMB Securities Research said pure upstream plantation companies, such as Hap Seng Plantations Holdings Bhd (KL:HSPLANT) and Sarawak Plantation Bhd (KL:SWKPLNT), are expected to report stronger earnings for the fourth quarter of 2024 (4Q2024).

These companies stand to benefit from higher crude palm oil (CPO) prices, which have helped offset the impact of lower production, stable fertiliser costs and ongoing efforts to enhance operational efficiency.

BIMB Securities anticipates that Hap Seng Plantations will report stronger earnings, driven by higher realised average selling prices, primarily due to spot market sales.

The company is also expected to benefit from a 3% quarter-on-quarter and 1% year-on-year increase in fresh fruit bunch (FFB) output for its fourth quarter of FY2024 (4QFY2024), along with the potential for higher CPO sales volumes.

The higher CPO prices in early 2025 are expected to support a positive performance for these firms.

Meanwhile, RHB said that earnings for 4Q2024 are likely to be largely in line with expectations, based on their projections of production levels.

However, the research house anticipates that five planters may underperform their forecasts due to lower-than-expected FFB output, while seven others are expected to report results that are largely in line with expectations.

The five planters are Kuala Lumpur Kepong Bhd (KL:KLK), IOI Corporation Bhd (KL:IOICORP), TSH Resources Bhd (KL:TSH), Bumitama Agri and Astra Agro Lestari.

The underperformance in productivity was particularly pronounced among planters with land banks in Indonesia.

The delayed impact of the 2024 El Niño is cited as a key factor behind the reduced output in the country, which has had a noticeable effect on these producers' performance, RHB added.

RHB’s top picks remain a mix of pure planters and situational plays — Johor Plantations Group Bhd (KL:JPG), Sarawak Oil Palms (KL:SOP), SD Guthrie Bhd (KL:SDG), Bumitama Agri and PP London Sumatra Indonesia.

Production to recover from March

Malaysia’s palm oil production is expected to pick up momentum beginning in March, following the traditional seasonal slowdown due to wet weather and biological tree rest phases, analysts said.

In a note on Wednesday, TA Securities predicted that production will gradually recover towards the second half of the year, with total output for 2025 estimated at 20.0 million tonnes, reflecting a 3% year-on-year growth.

These seasonal factors, coupled with a narrowing price gap between soybean oil and palm oil, will further support palm oil exports.

It is noteworthy that while China has not yet targeted the soybean market in response to new US tariffs, such a move could reduce soybean demand, lowering soybean oil prices.

This would likely widen the price gap between CPO and soybean oil, making soybean oil more competitive in the vegetable oil market.

While Apex Securities, in a separate note, forecasted a gradual improvement in CPO production, it expects prices to remain elevated for the rest of the first quarter of 2025.

The research house noted that CPO price fell in January 2025 after recording two consecutive months of gains, sliding by 8.7% month-on-month to RM4,673 per tonne.

"Nevertheless, we expect CPO price to gain traction when the palm oil demand recovers post winter in February 2025. Besides, we believe the narrowing price gap between soybean oil and CPO, along with a weaker ringgit, will support palm oil exports by making it more affordable for overseas refiners."

As harvesting conditions stabilise, production is expected to improve, supported by better FFB yields and higher oil extraction rates, it added.

Malaysia's palm oil end-stocks fell further to 1.58 million tonnes in January 2025, marking an 8% month-on-month decline and a 22% year-on-year drop.

This reduction in stocks was largely attributed to lower CPO production, which fell to 1.24 million tonnes in January — a 17% month-on-month decrease and a 12% year-on-year drop.

These trends were largely due to seasonal low production, the rainy season, and the biological tree rest phase, all of which contributed to reduced FFB yields and a lower oil extraction rate.

- Malaysian Highway Authority: 20km traffic jam on KL-Karak Highway as Raya travellers return

- China’s rare earths curbs put multiple US industries at risk

- US starts collecting Trump's new 10% tariff, smashing global trade norms

- China to US: 'Market has spoken' after tariffs spur selloff

- FMM flags significant challenge for 200 businesses amid 20-day gas disruption after Putra Heights fire

- Panasonic donates RM120,000 in e-vouchers to support Putra Heights victims

- Opec+ panel stresses compliance after surprise oil output hike

- Putra Heights fire: Airbnb offers 78 temporary homes for victims — Amirudin

- Indonesia's central bank vows to support rupiah amid trade tariffs threat

- Putra Heights fire: 42 victims still warded — MOH