This article first appeared in The Edge Malaysia Weekly on February 10, 2025 - February 16, 2025

ELRIDGE Energy Holdings Bhd (KL:ELRIDGE), a manufacturer of biomass fuel products such as palm kernel shells (PKS) and wood pellets, is actively working to expand its production capacity for PKS to capitalise on the burgeoning demand for biomass energy.

Biomass energy, generated by burning forestry and agriculture waste such as PKS, sawdust, rice husks, and wood pellets and chips, is growing globally as countries accelerate their transition to using cleaner energy. Some governments like the UK, South Korea and Japan give subsidies to support power plants using biomass.

“This puts Elridge in a sweet spot,” says Salihudin Mohd Razali, executive director and finance director of Elridge, in an interview with The Edge.

Its customers are based in Asia-Pacific. Elridge’s initial public offering (IPO) prospectus shows that Singapore was its largest market in the first four months of its financial year ended April 30, 2024 (4MFY2024), contributing 47.6% to its revenue, followed by Indonesia (31.5%), Japan (14%) and Malaysia (6.8%).

“Our customers mainly comprise biomass fuel product trading companies, which procure and resell the products to end-users such as industrial boiler operators for generation of heat and power plant operators. At times, we may also sell to end-users directly,” he adds.

Elridge executive director and CEO Oliver Yeo Hock Cheong is aiming for higher sales of its PKS in Japan, boosted by the Japanese government’s energy policies to achieve carbon neutrality, or net zero greenhouse gas emissions, by 2050.

In the aftermath of the 2011 Fukushima nuclear disaster, Japan began diversifying its electricity mix with nuclear power, imported coal and liquefied natural gas (LNG). Moving forward, it has laid out a plan called the “Best Energy Mix” for 2030, which comprises 21% nuclear energy, 27% LNG, 26% coal, 3% oil and 23% renewables.

“Now the focus from the Japanese government is to shift their coal-fired power plants to biomass power plants. In addition, the government offers some feed-in tariff (FIT) incentives. We want to capitalise on that. Initially, we started off with a lot of Malaysian customers, but over the years, between 2021 and 2023, we increased our exports. Demand from Japan alone is huge. Even the Philippines, Thailand and Singapore are very strong in biomass,” says Yeo.

“From our engagement with our Japanese customers, Japan’s Ministry of Economy, Trade and Industry has approved around 900 biomass power plants. Each power plant’s monthly usage is around 20,000 tonnes of biomass, depending on size. Even if Elridge’s capacity increases by 200 times, we still cannot meet that demand. On top of that, some existing coal-fired power plants in Japan are being converted into biomass power plants.

“The trend in biomass for sustainable energy options is something that many countries are pursuing as a replacement for coal-fired power plants. They can’t change everything overnight, but PKS is easier for them compared with other types of biomass. And Malaysia, being the world’s second-largest producer of palm oil, we have ample supply [of raw materials for the manufacturing of PKS].”

The 46-year-old Yeo holds a direct 5.86% stake in Elridge and an indirect 36.99% stake through Kayavest Sdn Bhd (16.37%) and Mikro MSC Bhd (KL:MIKROMB) (20.62%).

The group sources its raw materials from traders, oil palm plantation and milling companies, and transporters of palm fruits or logs.

Last year, the group landed two memoranda of understanding (MoUs) — one with PT Orion APAC Indonesia to supply 150,000 tonnes of PKS per year for three years from April this year, and another with Japan’s JFE Shoji Corp to supply the same quantity of PKS per year for 15 years, also from April. It remains to be seen whether the MoUs will be converted into multiyear contracts.

Currently, Elridge has a plant in Port Klang, Selangor, which has a capacity of 720,000 tonnes per year. In June last year, the group commissioned a second manufacturing plant with a capacity of 240,000 tonnes per year in Kapar, Selangor. This brings its cumulative production capacity to 960,000 tonnes per year, of which the utilisation rate is about 60% to 70%, says Yeo.

The group is setting up three more factories in Pasir Gudang, Johor; Kuantan, Pahang; and Lahad Datu, Sabah, this year. On completion of the three new factories, Elridge’s production capacity is expected to increase by 75% to 1.68 million tonnes per year.

Elridge, which was listed under the industrial products and services sector of the ACE Market of Bursa Malaysia in August last year, has earmarked 67% of its IPO proceeds of RM101.5 million for the planned expansion. Of the total, RM47 million, or 46% will be used for the construction of the new factory and warehouse in Kuantan, while RM23.5 million, or 21% of the proceeds will be allocated for the purchase of new machinery and equipment for its three new factories.

“We are having the capacity expansion because we foresee huge demand for PKS. Japanese customers want to ensure that you first meet their specifications in terms of product quality. Secondly, more importantly, can you supply them consistently? They want to know if you have the capacity or not. If not, they won’t sign a long-term contract with you. That is our key differentiation from other players,” Salihudin explains.

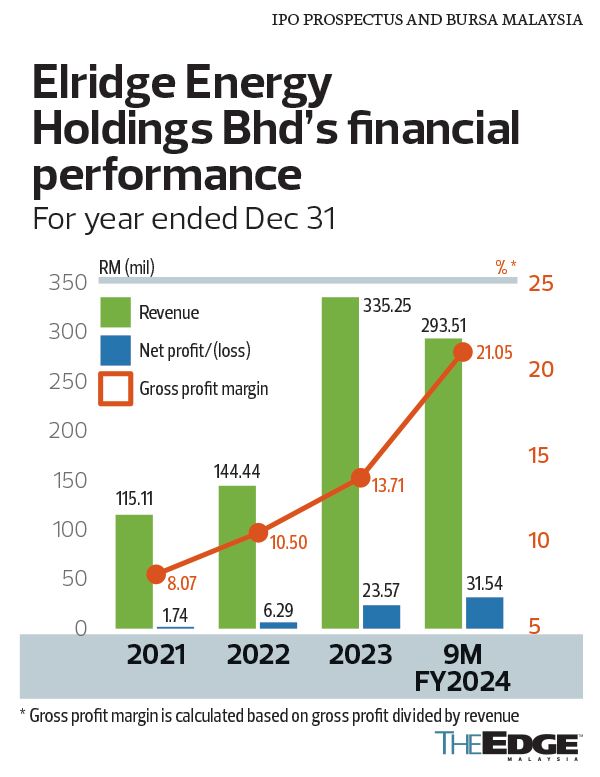

Elridge saw its net profit surge 275% to RM23.57 million in the financial year ended Dec 31, 2023 (FY2023), from RM6.29 million in the previous year, while revenue jumped 132% to RM335.25 million from RM144.44 million.

For the nine months ended Sept 30, 2024, Elridge recorded a net profit of RM31.54 million on revenue of RM293.51 million. Around 85% of its revenue was from the sale of PKS.

“Our operation for wood pellets is currently not that big. Since demand for PKS is so huge, we are not focusing on [wood pellets] for now,” says Yeo.

Salihudin says, “We have an outstanding order book of 720,000 tonnes of PKS for FY2024 and another 710,000 tonnes for FY2025. In addition, we anticipate our contracts with PT Orion APAC Indonesia and JFE Shoji Corp to commence in April. Today, PKS demand far outstrips supply. So, we are confident we can sustain our growth trajectory.

“However, we dare not sign too many contracts and overcommit ourselves.”

The average selling price (ASP) of PKS for customers based in Malaysia stood at RM441.76 per tonne in 4MFY2024, down by a marginal 1.6% from RM448.98 per tonne a year earlier.

The ASP of PKS sold to its foreign customers also fell 10.5% to RM493.71 per tonne in 4MFY2024, from RM551.35 per tonne in 4MFY2023, on lower average cost of purchasing unprocessed PKS arising from higher supply of unprocessed PKS available in the market.

“The PKS for our foreign customers generally command higher ASP, mainly due to the different types of PKS specifications such as moisture content level, ash volume, sulphur volume, impurities, as well as other specifications as specified by our foreign customers, in line with the foreign regulations imposed on the imports of PKS,” says Salihudin.

“Our gross profit margin is healthy, at double digits, which is in line with the overall increase in revenue. We managed to get a better selling price and lower cost. Hopefully, we can maintain it throughout the years.”

Its gross profit margin derived from the manufacturing of PKS and wood pellets was 21.05% in 9MFY2024, up from 13.17% in FY2023.

Elridge had a net cash position of RM115.65 million at end-September 2024. Its cash reserves stood at RM155.32 million, while borrowings amounted to RM39.67 million.

“We have ample room to grow if need be. In terms of capital expenditure, we can use proceeds from the IPO. If we were to increase our gearing, it would be more from credit tradelines and it would mostly be for working capital such as to purchase raw materials. But we don’t need it at this point in time,” says Salihudin.

On plans for mergers and acquisitions, he says the group prefers to focus on maximising its capacity for now.

Nevertheless, the group faces credit risks as its financial performance depends on customers’ ability to pay, with credit periods typically ranging from 30 to 90 days. This exposes Elridge to credit risks related to trade receivables, which could be influenced by unforeseeable events such as economic downturns. Delays in payment could impact the group’s cash flow and working capital, potentially affecting its financial performance.

The biomass fuel industry in Asia-Pacific is fragmented, with numerous players that manufacture and/or trade PKS and wood pellets in the region.

Independent market researcher Providence Strategic Partners Sdn Bhd estimates that there are about 30 other industry players involved in the manufacturing of biomass fuel products in Malaysia, of which 14 are involved in the manufacturing of PKS and/or wood pellets. Yeo says Elridge garnered a 22.3% revenue share of the PKS industry in Asia-Pacific of RM1.3 billion in 2023, making it the leading player.

“We have an edge [over our competitors] because of our bigger [production] capacity. For instance, Japanese customers are particular about the quality and reliability [of the biomass fuel products that we supply them]. They also want to see that we have the capacity to support them in firing their power plants. It usually takes us two years before they would sign a contract with us. That’s why our Green Gold Label-certified PKS is important,” says Yeo.

Reclassification to energy sector to enhance company’s appeal

In an Aug 21, 2024 report, Maybank Investment Bank (Maybank IB) said Elridge is trading at a historical FY2023 price-earnings ratio (PER) of 24.6 times, at its IPO price of 29 sen. When annualised, Elridge would trade at 12.9 times annualised 4MFY2024 earnings per share of 2.2 sen.

“Prospects-wise, sales to international markets are expected to drive growth, supported by government initiatives to drive the use of renewable energy (RE),” it added.

Elridge’s share price has risen 7% so far this year and closed at 46 sen last Thursday. The stock is up 59% from its IPO price of 29 sen per share on Aug 22, 2024.

Meanwhile, Elridge is hopeful that its reclassification to the energy sector and RE subsector by Bursa on Jan 13 would better reflect its core business activities and enhance the group’s appeal to a more diverse range of local and international investors.

“From an investor’s point of view, they can compare with other counters. The nearest comparison [with listed entities] are solar companies, which trade at more than 30 times PEs. We hope to get there,” says Salihudin.

As for whether Elridge plans to establish a fixed dividend payout policy, he says the group will focus on growing itself first. “We want to make more money until we become stronger in terms of profits. But going forward, we intend to be a dividend stock,” he adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia’s richest just got wealthier thanks to stronger ringgit — Forbes

- Canada, Japan led foreign treasuries-buying jump in February

- Vista buys Petronas oil stake in US$1.5 bil Argentina deal

- Malaysia Aviation Group posts RM54m earnings for FY2024, its second straight annual profit

- China ready to sign Asean-China Free Trade Upgrade Protocol soonest — Xi

- China offers Philippines 'win-win' path against US 'protectionism'

- Gas supply restored for 259 customers, says Gas Malaysia

- New experiences, changing demographics and AI to influence hospitality industry

- TSMC quarterly profit jumps, upbeat on outlook despite tariff uncertainty

- ECRL on track for completion by December 2026, says MRL CEO