This article first appeared in Capital, The Edge Malaysia Weekly on January 20, 2025 - January 26, 2025

Construction

OVERWEIGHT

CIMB SECURITIES RESEARCH (JAN 15): Based on our observations, the US government’s potential restrictions on artificial intelligence (AI) chip exports would have minimal impact on the existing data centre (DC) contracts of Malaysian contractors at this juncture, as most of their clients are either multinational technology companies or global hyperscale operators.

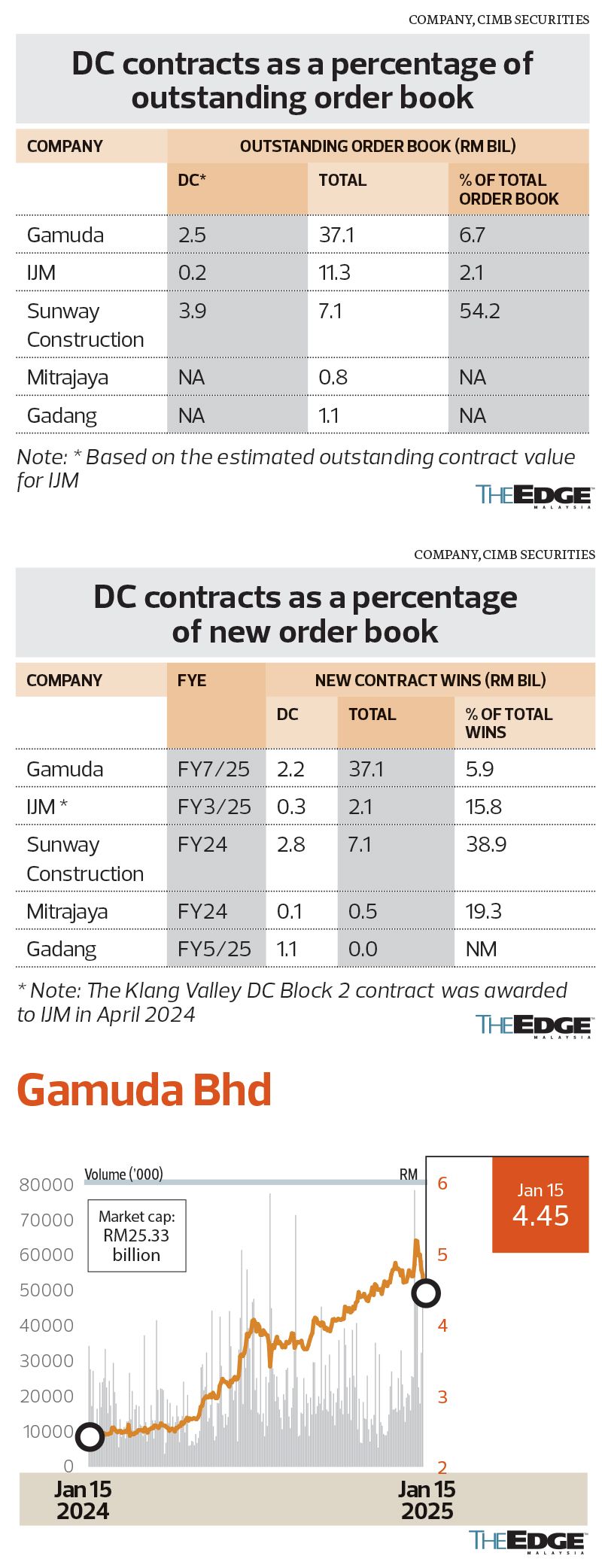

IJM Corp Bhd (KL:IJM) won a RM332 million contract to construct Block 2 of Telekom Malaysia Bhd’s (KL:TM) Iskandar Puteri DC — its maiden DC win. Meanwhile, the groundbreaking ceremony for Gamuda Bhd’s (KL:GAMUDA) proposed 389-acre DC hub at the Springfield Industrial Park (land cost: RM424 million, or RM25 psf) took place on Jan 9.

For construction-related stocks, Sunway Bhd (KL:SUNWAY) — through its 65%-owned Sunway Construction Group Bhd (KL:SUNCON) — has the highest exposure to DC contracts at RM3.9 billion, or 54% of its outstanding order book. For Gamuda and IJM, the unbilled portion of their DC order books is estimated at RM2.5 billion (7% of total) and RM0.2 billion (2% of total) respectively. Outside our coverage, Mitrajaya Holdings Bhd (KL:MITRA) won a RM87 million contract to undertake foundation works for the NEXTDC KL1 DC project in Petaling Jaya, while Gadang Holdings Bhd (KL:GADANG) bagged a RM280 million contract under TM’s Klang Valley DC Block 2 (both contracts were awarded in April 2024). More importantly, ongoing DC work orders are still progressing, although lingering uncertainties over the US government’s future stance on AI chip exports may temporarily cloud the outlook for DC-related builds.

Similarly, we opine that the actual impact on the property sector is fairly insignificant — most of the DC-related ventures are still at the preparatory stage with minimal capex spent, and are backed by multinational technology companies or hyperscalers.

We remain “overweight” on the construction sector and retain Gamuda (“buy”, target price: RM6), IJM (“buy”, TP: RM3.80) and Malaysian Resources Corp Bhd (KL:MRCB) (“buy”, TP: 96 sen) as our top picks. We also reiterate our “neutral” view on the property sector, with Mah Sing Group Bhd (KL:MAHSING) (“buy”, TP: RM2.10) as our preferred pick for its exposure to the affordable housing segment.

Axiata Group Bhd

Target price: RM3.40 BUY

RHB RESEARCH (JAN 14): Management of Axiata Group Bhd (KL:AXIATA) tightened the narrative on balance sheet optimisation, dividend capacity (progressive 10 sen/share) and portfolio transformation (value illumination and monetisation). We continue to like the stock with balance sheet deleveraging and operational improvements as share price catalysts.

Continued focus on balance sheet deleveraging is a key positive, in our view, with net debt/Ebitda at two-year lows (3Q24: 2.5 times). After lowering holdco USD debt by US$2.7 billion in 9M24, Axiata is looking to further pare down holdco debt in FY25-26F via proceeds from asset monetisation (edotco, Link Net, digital services) and equalisation of stake in XL Axiata pursuant to its merger with Smartfren.

edotco would look to enhance yields and maximise dividends in core markets (Malaysia, Bangladesh, Cambodia), deliver in growth markets (Indonesia, the Philippines) and monetise non-core assets (Myanmar [sale pending regulatory approval)], Pakistan, Sri Lanka). In Malaysia, edotco aims to capture a bigger share of the seven “red states” (currently no presence) via partnerships.

CelcomDigi Bhd (KL:CDB) (“buy”, TP: RM4.35) expects more synergies to be realised in FY25-26F. Boost is set to be Ebitda-positive by FY26. It is set to receive a new strategic investor (US$45 million), bringing cumulative investments to US$203 million.

Yinson Holdings Bhd

Target price: RM3.87 OUTPERFORM

KENANGA INVESTMENT BANK RESEARCH (JAN 15): Yinson Holdings Bhd (KL:YINSON) proposed a US$1 billion redeemable convertible preference share (RCPS) and warrant issuance (with an option to increase to US$1.5 billion). The deal’s implied EV/Ebitda is above the peer average, reflecting strong investor confidence in Yinson’s ability to secure more floating production, storage and offloading (FPSO) contracts. We maintain our forecast and SOP target price of RM3.87 at this juncture as the implied valuation of FPSO assets aligns with our assumptions.

We continue to favour Yinson due to a strong FPSO order book pipeline with multiple major FPSO jobs under the conversion stage, which provides significant earnings growth in the coming years; its strong project execution track record, which positions the company to benefit from strong structural demand for FPSO contractors anticipated in the coming years; and the group could seek to monetise its FPSO assets partially (selling a minority stake) to recycle its capital as its new FPSO projects are nearing completion.

Risks to our call include crude oil prices falling below US$70/bbl, raising required internal rate of return for new floating production projects; regulatory and project execution risks; and uncertain returns for renewable energy investments that are mainly focused on emerging markets.

Yenher Holdings Bhd

Target price: RM1.45 BUY

HONG LEONG INVESTMENT BANK RESEARCH (JAN 14): Yenher Holdings Bhd (KL:YENHER) achieved its strongest quarterly performance since listing, with 3Q24 core earnings climbing 26.2% q-o-q and 20.7% y-o-y, bringing 9M24 core earnings to RM16.8 million (+9.3% y-o-y). This growth was driven by robust premix sales to the poultry segment. The impressive underlying results may have been overlooked due to the decline in headline earnings, creating a misleading perception of a weaker operational performance. In reality, operational growth was robust, driven by higher premix manufacturing sales to the poultry segment and supported by the acquisition of new customers.

The group is making solid progress across key initiatives, including its premix and complete feed expansion, Denmark joint venture in biotech feed additives and its new BSF (black soldier fly cultivation) venture, positioning itself to tap high-growth markets. With new capacities on track for commissioning by end-FY25, Yenher will significantly expand its production, setting the stage for an exciting multiyear growth trajectory starting from FY26. Maintain forecasts and “buy” rating with a TP of RM1.45, based on 16 times mid-FY26 EPS.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Making a bold move in Kota Kinabalu

- Ukraine to seek more US investments in talks over economic deal — Bloomberg

- Businessman with 'Tan Sri' title, said to be O&G industry veteran, arrested for RM10m scam

- Indonesian Muslims to celebrate Eid on Monday

- Myanmar hit by fresh 5.1 aftershock, tremors felt in neighbouring countries