Singaporean banks reach all-time high after JS-SEZ agreement

KUALA LUMPUR (Jan 8): The three biggest banks in Singapore — Oversea-Chinese Banking Corp (OCBC), DBS Group Holdings Ltd and United Overseas Bank (UOB) — closed at all-time highs on Wednesday after Malaysia and Singapore signed the Johor-Singapore Special Economic Zone (JS-SEZ) agreement.

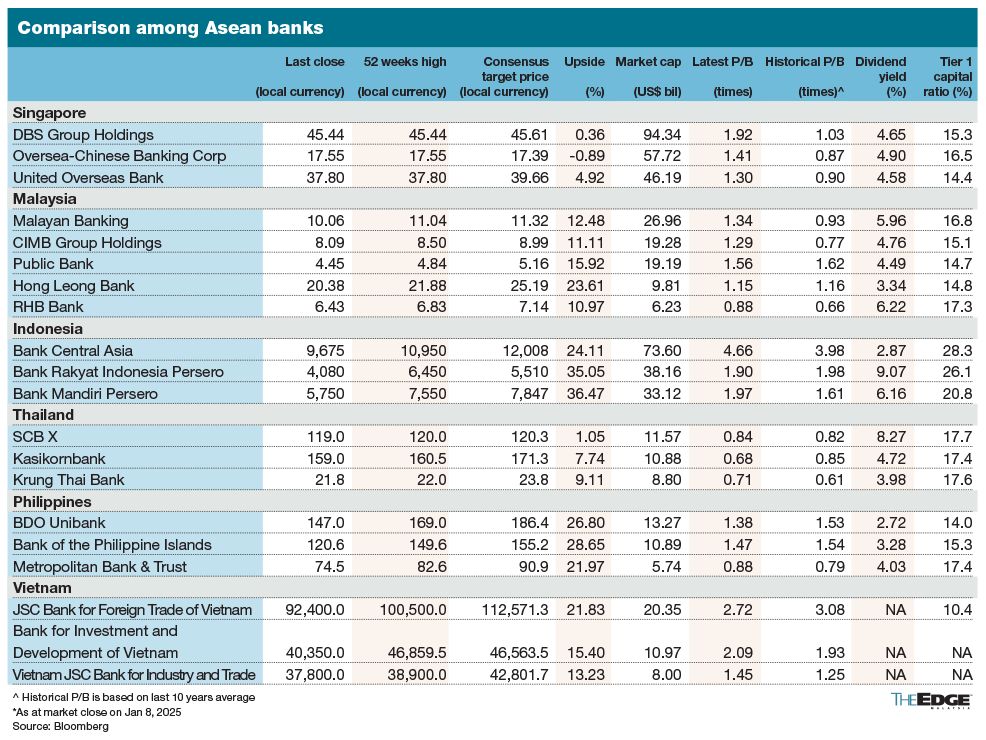

Shares of OCBC rose 4.15% or 70 cents to S$17.55, while DBS closed 2.11% or 94 cents higher at S$45.44; UOB closed at S$37.80, up 75 cents or 2.02%.

All three banks are now trading at record high price-to-book valuations, with DBS at 1.92 times, followed by OCBC at 1.41 times and UOB at 1.30 times.

The banks' strong share price performances have pushed their valuation past some of their counterparts in Thailand and Malaysia.

Analysts see Singaporean banks as prime proxies to Asean's economic growth, driven by inflows of foreign direct investments (FDIs).

Maybank Securities' Thilan Wickramasinghe observed that Singaporean banks have been investing in regionally integrating their wholesale and retail banking over the past five to six years, which has enabled them to capture and facilitate supply chain shifts from North Asia to Asean.

UOB Kay Hian's analyst Jonathan Koh also shared a similar view, noting that FDIs into Asean countries are projected to expand at a compound annual growth rate (CAGR) of 8.3% to reach US$356 billion (RM1.6 trillion) in 2030.

Both analysts think OCBC and UOB are beneficiaries of the JS-SEZ and Asean supply chain repositioning due to their extensive network within the region.

Wickramasinghe, in his thematic report titled "Singapore Winners", believes that Singaporean banks are likely to capture business opportunities in the new economic zone arising from increased labour and capital flows.

The twinning operations of multinational corporations (MNCs) in Singapore and the JS-SEZ, together with the Singapore government's funding for small and medium enterprises (SMEs) to expand in the JS-SEZ, will drive higher credit demand as well as non-interest income (NOII) in the form of advisory, transaction banking and cash management services, he said.

Retail banking will also benefit from increased cross-border spending and drive more credit card fees, he said.

Singapore banks are also expected to enjoy lower costs as they can take advantage of relatively lower labour and rental costs by moving their back-office functions to service centres in Johor, he said.

Dividends from SG banks may exceed projections

There could be upsides to dividend projections for Singaporean banks from better-than-expected earnings and more aggressive capital returns, according to RHB Research.

While DBS offers dividend safety, given its guidance for a fixed step-up in absolute dividends per share, RHB Research thinks OCBC and UOB may offer higher dividends should earnings next year turn out to be better than expected.

But UOB Kay Hian's Jonathan Koh think DBS may potentially pay special dividends in 2025, on top of a step-up in quarterly dividends. OCBC could also consider raising its dividend payout, he said.

The positive views are mostly due to Singaporean banks' strong asset quality.

RHB noted that the banks have adopted Basel III reforms, which were introduced to make banks safer after the 2008 global financial crisis, and reported fully phased-in CET-1 ratios of 15-16%.

The CET-1, or Common Equity Tier 1 ratio, measures how much of a bank's capital is its own money compared to riskier assets like loans. Under Basel III rules, the minimum CET-1 ratio is 4.5%.

- Tariff shock awaits China after trade surplus hits US$103 bil

- Malaysian semiconductor stocks fall amid US probes, software firms steady

- Maybank customers can now make QR payments through MAE app in Cambodia

- HRD Corp's chief executive Shahul Hameed steps down, confirming The Edge report

- Nation gathers to bid farewell to Pak Lah

- UK employers cut jobs in run-up to Reeves' tax hike

- Investors haven’t been this bearish in 30 years, BofA poll shows

- Fire Dept targets 18,000 homestay inspections in Melaka ahead of VM2026

- Malaysia keeps May crude palm oil export duty at 10%, lowers reference price

- India’s trade gap widens as Trump roils markets with tariff war