Capital gains are an important aspect of investing for those who buy into a company on the stock market. Hence, those who invested early in Kobay Technology Bhd would certainly appreciate how their investment has grown in the last four years.

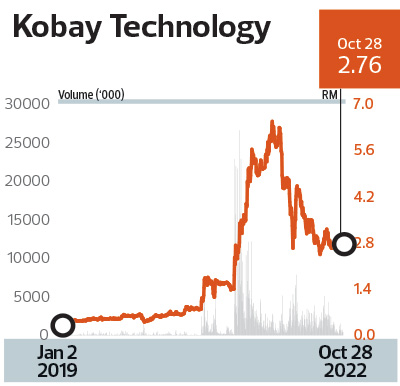

Investors’ patience was probably tested in the earlier years. Kobay’s adjusted share price stood at a mere 45 sen on March 29, 2019, and did not change much in the following year. However, by March 31, 2021, the share price had shot up to RM1.56 and it leaped further to RM4.38 by March 31, 2022.

That brought the three-year compound annual growth rate (CAGR) for its shareholder return to 114% — which led to Kobay winning this year’s BRC award for the highest returns to shareholders over three years in the industrial products and services sector.

Since April, however, Kobay’s share price has been on a steady decline. Closing at RM2.65 to value the company at RM864.38 million at the time of writing, its market capitalisation slipped below the RM1 billion mark. But the company still had a market cap of more than RM1 billion at end-March to qualify for the BRC. Still, at least one sell-side analyst reckons that the company should be worth more than RM1 billion.

The Penang-based company’s business is divided into two main segments, with the first being the manufacturing of precision components, tooling, automation equipment and fabricated structures. Its other segment is property development, with its maiden project in Langkawi having a gross development value of RM318 million. Its upcoming projects are largely located in Penang and Kuala Lumpur.

A large portion of the group’s revenue is derived from its manufacturing segment, given how Kobay only made its foray into property development in 2016.

The group, which has a financial year ending June 30, saw its revenue grow from RM169.15 million in FY2019 to RM197.52 million in FY2020. However, its revenue fell to RM156.99 million in FY2021.

Kobay said in its annual report that the revenue from its manufacturing division was affected by lower orders from the aerospace and oil and gas industries, which were impacted by the Covid-19 pandemic, thus causing the decline in group revenue.

Interestingly, while revenue faltered in FY2021, its net profit hit a record high of RM26.76 million. Notably, its net profit had climbed steadily from RM18.92 million in FY2019 to RM23.93 million in FY2020. The net profit margin for FY2021 improved by 4.9 percentage points from 12.1% in FY2020 to 17% in FY2021.

Its recently concluded FY2022 was another good year for Kobay, with its net profit almost doubling to RM51.29 million from RM26.76 million in the previous year.

Revenue also saw significant growth, doubling to RM354.27 million in FY2022 from RM156.99 million in the previous year. The rise in revenue and net profit was attributed to higher demand from the electrical and electronics industry and contribution from its newly acquired pharmaceutical business.

In July 2021, the group received shareholder approval to purchase 70% of pharmaceutical company Avelon Group for RM47.7 million (with an option to buy the remaining 30%), in a deal that came with a profit guarantee of RM25.5 million over three years (which is an average of RM8.5 million a year). Avelon has four pharmacies operating under the brand Park@City, a retail store that sells BioBay brand products and a warehouse in the Klang Valley.

In a Sept 12 report, Hong Leong Investment Bank Research (HLIB Research) said Kobay was in the final stage of preparations for its venture into the manufacturing of aluminium frames for solar panels, which would further expand its clientele.

“Management expects FY2023 expansion to be largely driven by the organic growth of the core business with a set target of between 50% and 80%. The new business segments will be an additional bonus for the group, namely the solar segment and EMS,” the HLIB Research analysts wrote, reiterating their “buy” recommendation on the stock.

Its target price, however, had been lowered to RM4.94 from RM6.08 to reflect a downward revision to its FY2023 earnings forecast, which reduces the value of its manufacturing business to RM1.36 billion (RM4.16/share) from RM1.73 billion (RM5.30/share) while still pegged to a multiple of 25 times. Using a sum-of-parts method, HLIB continued to value Kobay’s property division at FY2021 book value of RM80.9 million (25 sen/share) and its pharmaceutical business at 20 times FY2023 earnings (RM172.4 million, or 53 sen/share).

The research house added that the property development segment is expected to recover gradually on the back of the completion of the Langkawi project by the end of 2022. “In view of the escalating cost of building materials and increase in borrowing costs, Kobay will take measures to mitigate the impact and pace out new launches according to market demand,” it wrote.

- BYD unveils battery system that charges an EV in five minutes

- MRCB, Sapura Energy, Solarvest, Salcon, Rohas Tecnic, HHRG, Jentayu, Focus Point, Catcha Digital, Poh Huat, Dutch Lady, AmanahRaya REIT

- MACC chief says Ismail Sabri has a lot to answer to, vows thorough probe

- Loke: Malaysia to receive two ETS train sets from China next month

- Jentayu Sustainables’ Sabah hydro asset acquisitions mutually terminated

- Creative Technology cuts workforce, adding to global wave of tech layoffs - report

- Pimco turns more negative on German bonds ahead of debt vote

- Volkswagen's Audi to cut 7,500 jobs in administration, development by 2029

- Asia Poly disposes of entire stake in Ta Win

- OECD warns of tariff drag on growth as Trump vows to press on with levies