This article first appeared in The Edge Malaysia Weekly on November 7, 2022 - November 13, 2022

Gas Malaysia Bhd has won The Edge Billion Ringgit Club award for highest return on equity (ROE) in the utilities sector for the fourth straight year. The group’s ROE remains on an upward trend, having risen from 18.4% in the financial year ended Dec 31, 2019 (FY2019) to 20% in FY2020 and 22.6% in FY2021. This translated into an adjusted weighted ROE of 21% over the three years — the best in class for the sector — according to the awards methodology.

Gas Malaysia sells, markets and distributes natural gas and develops, operates and maintains the natural gas distribution system in Peninsular Malaysia. At end-2021, the company had developed a total of 2,706km of gas pipelines across the peninsula, supplying natural gas to 998 industrial, 1,825 commercial and 22,873 residential customers. It also supplies liquefied petroleum gas to 946 commercial and 12,538 residential customers.

Gas Malaysia’s net profit increased to RM249.62 million in FY2021 from RM212.62 million in FY2020, amid lower administrative expenses and finance costs. It recorded a net profit of RM190.11 million in FY2019.

Revenue slipped to RM5.85 billion in FY2021 from RM6.69 billion in FY2020 due to a lower average natural gas tariff, but was mitigated by the higher volume of natural gas sold and higher recognition of revenue cap. In FY2019, Gas Malaysia’s revenue stood at RM6.89 billion.

The company was not spared the impact of the resurgence in Covid-19 cases and reimposition of the Movement Control Order, which led to a decline in natural gas volumes in the second half of 2021, Gas Malaysia says in its annual report. However, volumes recovered towards the end of the third quarter of 2021 as the government eased Covid-19 containment measures.

Gas Malaysia has consistently rewarded shareholders with dividends. A dividend of 17.67 sen was paid in FY2021 despite uncertain times, representing a total dividend of RM226.9 million. This is higher than the dividend paid in FY2020 of 15.05 sen (representing a total payout of RM193.4 million) and in FY2019 of 14.1 sen (RM181 million).

The local gas market is expected to be fully liberalised this year whereby gas will be traded at market price, including gas to the power sector, based on a willing buyer, willing seller basis. This will enable end users to have alternative sources of gas and attract third-party shippers to enter the market.

The liberalisation of the gas market is expected to have a limited impact on Gas Malaysia’s earnings because its scale of operations gives it a competitive advantage in terms of lower gas costs over its rivals.

“We believe that the liberalisation of the gas market and third party access in 2022 will create a more vibrant yet competitive industry as it will open up to new industry players while simultaneously offering the group attractive growth opportunities throughout the value chain,” Gas Malaysia chairman Tan Sri Wan Zulkiflee Wan Ariffin says in the group’s annual report.

Notwithstanding that, Gas Malaysia will face speed bumps in the near future as global gas prices fall and glove demand slows, Kenanga Research says in a Sept 20 note.

“While Gas Malaysia no longer [shares its] gas volume data since 1QFY2022 for competitive reasons, under the more liberalised market environment, the company has guided for a slowdown in volume which we believe could be attributable to lower production by glove makers that typically contribute to a third of Gas Malaysia’s business volume,” adds Kenanga.

Glove manufacturers account for 33% of the company’s gas demand, followed by consumer products (18%), other products (16%), oleochemical products (11%), glass products (11%), pulp and paper (6%), and steel/aluminium/copper (5%). The volume of gas sold by Gas Malaysia in 2021 stood at 203.3 million MMBtu, versus 200.1 million MMBtu in 2020 and 201.2 million MMBtu in 2019.

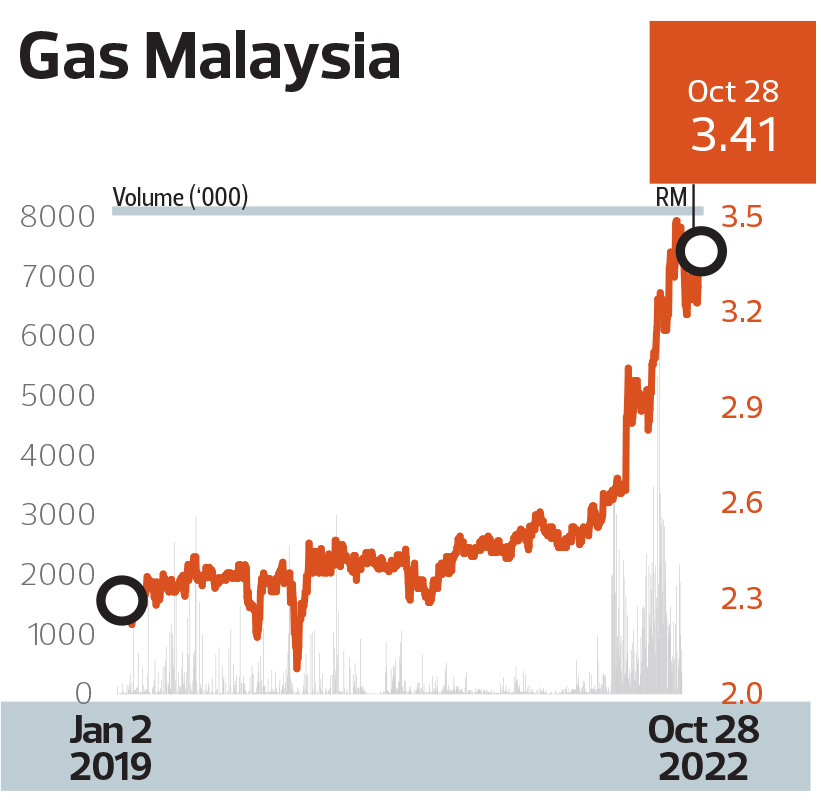

Kenanga has downgraded Gas Malaysia to “market perform” from “outperform” but left the target price at RM3.43. It believes the company’s earnings will peak in FY2022 as gas prices soften.

Nonetheless, Gas Malaysia’s long-term earnings remain defensive and supported by its regulated business (gas transport), which anchors its dividend yield of more than 6%, the research house says.

Gas Malaysia had seven “buy” and two “hold” calls with an average target price of RM4.33, Bloomberg data showed at the time of writing.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Anwar, Xi witness exchange of 31 MOUs and documents to advance Malaysia-China cooperation

- Bina Puri announces boardroom changes, founder director Tan Cheng Kiat retires

- SkyWorld buys three-acre Mont Kiara land for RM110m

- ‘No connection’ between Sapura Industrial and Sapura Group, says MD

- PwC exits more than a dozen countries to avoid scandals, FT reports

- Putrajaya orders temporary closure of KL Tower, says past concessionaire's stay 'unlawful'

- Meta saw TikTok as ‘highly urgent’ threat, Zuckerberg says at antitrust trial

- Sapura Industrial, Gas Malaysia, CapitaLand, Hextar Technologies, Golden Land, Skyworld, Sapura Energy, Bina Puri, Paragon Globe, OCK Group, Nextgreen, Nexgram

- Ivory Properties aborts land disposal deal with Chin Hin following liquidation of subsidiary

- Tesla slumps below 50% share of California’s electric car market