This article first appeared in Forum, The Edge Malaysia Weekly on March 29, 2021 - April 4, 2021

"Malaysia represents an encouraging environment for potential investors and operators. It is ranked 12th in the World Bank’s Ease of Doing Business index ... Power market liberalisation efforts are also underway, under the Malaysia Electricity Supply Industry (MESI) 2.0 reforms. This programme is driving gradual liberalisation of power market segments, with a fully competitive power market targeted over the coming years, opening up opportunities for investment and competition.”

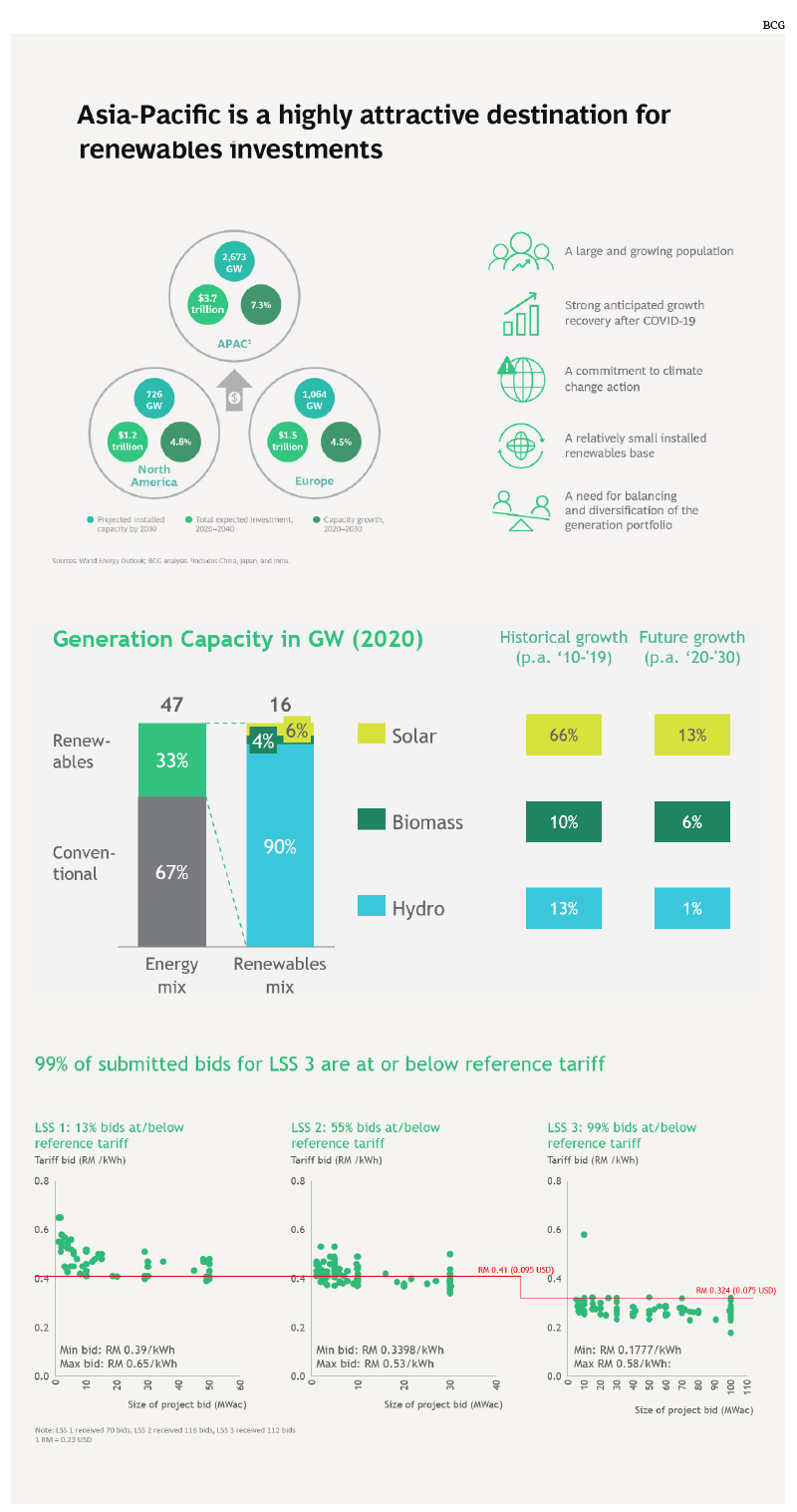

Asia-Pacific’s (APAC) renewable energy capacity will grow by 7% year on year over the next decade, adding a significant two terawatts of capacity by 2030. This remarkable growth will be driven by rising populations, strong economic prospects and lucrative potential in a market with relatively low renewable penetration.

Southeast Asia is an important part of this growth journey, with electricity demand in the region expected to grow at double the global average over the coming years. The region’s overall electricity demand is expected to double by 2040. In Malaysia alone, installed capacity is projected to expand by over 30%, from 36gw in 2020 to 47gw by 2030, with most of the growth from solar power installations.

Boston Consulting Group’s (BCG) recent report, “Riding the Renewables Wave in Asia-Pacific”, explores the potential for investors and operators in a market with an expected US$3.7 trillion (RM15.3 trillion) of planned investment, more than the combined renewable investment commitments of North America and Europe.

Green post-pandemic recovery commitments will deepen this shift, expanding government revenues by up to 30% thanks to coal subsidy elimination, while leveraging a valuable investment landscape.

Southeast Asia’s shifting landscape

Renewable energy in APAC will benefit from significant falls in generation costs, alongside growing support for technologies such as utility-scale batteries and green hydrogen.

The levelised cost of energy (LCOE) for solar power has fallen at an annual rate of 19% over the last decade. Offshore wind costs are also dropping, supported by technology transfer from mature European markets.

Solar technologies will be a major driver of regional renewables growth. Installed solar capacity expanded 66% in the last decade, driven by significant large-scale solar projects over recent years.

While Malaysia offers little near-term promise in wind power, APAC will emerge as the second-biggest offshore wind market by 2030, with annual growth of 24%, driven by geographical benefits and early-development-phase investment returns.

Renewables currently contribute 18% to Malaysia’s energy mix, dominated by hydropower technologies, which account for 86% of renewable capacity. Malaysia has an ambitious target of renewables, excluding hydropower, to grow to 20% of the generation mix by 2025.

Investing in Malaysia’s renewable opportunity

There is no one-size-fits-all solution to operators or investors looking to leverage Southeast Asia’s high-growth market potential. Players must take a country-specific approach that reflects the local landscape, understanding market dynamics and local potential for specific technologies.

Malaysia represents an encouraging environment for potential investors and operators. It is ranked 12th in the World Bank’s Ease of Doing Business index, reflecting a country that is broadly welcoming of foreign investment and multinational companies.

Power market liberalisation efforts are also underway, under the Malaysia Electricity Supply Industry (MESI) 2.0 reforms. This programme is driving gradual liberalisation of power market segments, with a fully competitive power market targeted over the coming years, opening up opportunities for investment and competition.

Malaysia is expected to more than double renewable capacity from 6gw to 14gw, rising from 18% to 30% of the generation mix. While the overarching ambition of non-hydropower renewables reaching 20% of the energy mix by 2025 may be overly optimistic, it is clear that large-scale solar (LSS) investment remains a major technical and financial opportunity for Malaysia.

Solar photovoltaic (PV) has by far the highest technical potential in Malaysia, and is supported by mechanisms to promote affordability. Malaysia allows installation of solar for self-consumption. Its Net Energy Metering Programme (NEM) provides a pathway to self-generation with excess energy sold back into the grid. The nation’s LSS projects offer a successful pathway to utility-scale solar adoption.

The latest bidding round for LSS reveals that the market is competitive and fragmented. It is also one of the most expensive solar markets in APAC, behind only Japan and Indonesia. The third round of LSS tenders saw 99% of bids below the reference tariff price. Solar power producers in Malaysia are also responsible for the cost of grid connection, adding to the financial burden.

Malaysia’s end-to-end solar PV value chain still reflects some important opportunities for investors and operators, including a well-established solar PV manufacturing industry. Manufacturing, project development, installation and construction, ownership, operation, service and maintenance all offer areas of potential to the right type of industry player.

Foreign investors looking for successful market participation should get involved early in the value chain, which could offer higher returns. Establishing a strong local partnership is critical to success, with ownership rules capping foreign ownership at 49% equity.

Integrated developers operating across manufacturing, development, EPC (engineering, procurement and construction) and asset operations have demonstrated success in Malaysia. There is also a chance to establish cost leadership, driving reductions in LCOE. Demonstrable operational excellence in integration with local partners is also a valuable differentiator.

Biomass power generation offers another potential area of opportunity, leveraging the nation’s palm oil industry as a fuel source. Grid access and connectivity remain issues in this diverse and rural industry, however. Small-scale hydropower is another evolving area that may present opportunities moving forward, benefiting from the nation’s hilly topography and high rainfall.

Click / Tap image to enlarge

A new clean-energy opportunity

Hydropower also feeds into another major long-term opportunity in Malaysia, with the advent of green hydrogen generated from renewable technologies. With a significant large-scale hydropower base, Malaysia’s Sarawak region boasts favourable conditions for a technology long touted as a revolution in green energy.

The majority of the world’s hydrogen is created through traditional fossil fuel power industries. Leveraging renewable technologies would decarbonise the value chain, providing new opportunities for low-carbon power and transport, and benefiting from attractive market potential in industrial nations such as Japan and South Korea. It is estimated that US$12 billion would be required to create an integrated hydrogen project in Sarawak, and US$2.7 billion for a fuel cell train system.

Green hydrogen offers notable equity opportunities for financial players. It also offers technical opportunities in technology service providers, project development, and utility or oil and gas company ownership. While power usage applications for green hydrogen remain in the early stages, there is clear investment potential for infrastructure players and storage developers.

Energy transition as the nation’s engine

Malaysia has an encouraging future of renewable energy adoption, complemented by a broadly attractive investment environment. Maximising existing businesses, expanding the value pool and exploring new frontiers all offer valuable areas to win in this evolving green energy landscape.

New renewable power sources will add value across the value chain, unlocking wide-ranging benefits for the nation. Malaysia’s PV manufacturing and potential to expand its thriving car industry through battery manufacturing represent just two of the numerous opportunities in manufacturing.

The rollout of renewables will create new jobs and open new business opportunities to upgrade existing network infrastructure. Green energy means fresh opportunities for Malaysia.

Dave Sivaprasad is managing director, partner and Southeast Asia leader for climate action at Boston Consulting Group. Priyanshu Kumbhare is a principal at BCG.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysian exporters halt US shipments amid tariff confusion

- Malaysian stocks rebound, broad relief rally adds back RM75 bil to market

- Trump's big blunder — and no, its not tariff per se

- Zafrul: Malaysia welcomes US tariff pause, now assessing implications

- Senator Adam Schiff calls for insider trading investigation into Trump over tariff pause

- Britain's Tesco warns profit to fall as competition intensifies

- Taiwan could buy US$200 billion more from US, increase LNG imports as part of trade deal

- Malaysia’s palm oil stocks rise for first time in six months in March

- Yuan falls versus everything as China’s tariff relief valve

- Phase 2 of Mitraland’s 22 Quartz 95% taken up, third phase launched