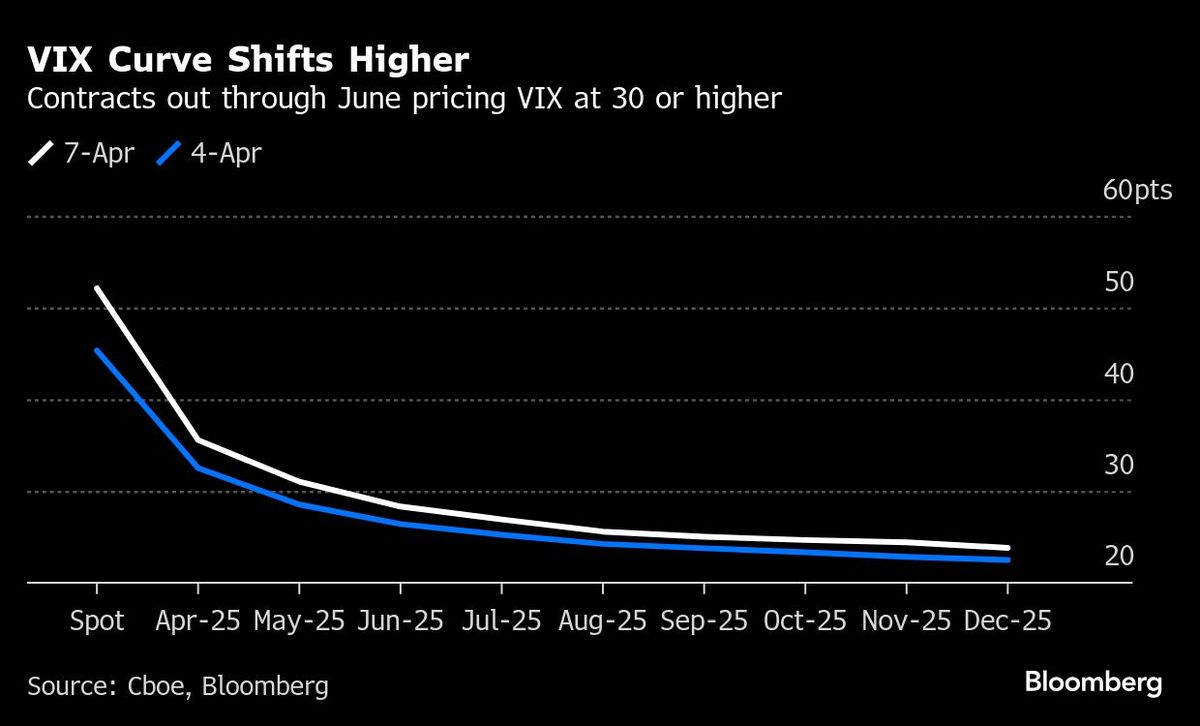

(April 7): The Cboe Volatility Index (VIX) is higher following an overnight spike above 60, and the futures curve is signalling that volatility may remain elevated for months.

Contracts out through June are trading near 30 — well above the 10-year average of 19 for the spot index. It’s a sharp change from a week ago, when the June future was hovering around 20.

The VIX — which gauges expected volatility for the S&P 500 about a month out — is holding around 51 with stocks down 3% in early US trading. While the VIX will need further steep losses in stocks to rise higher, the market is pricing more volatility, given spiraling trade war and deep economic uncertainty it has created.

“We expect the minimum level of realised volatility to remain elevated given the cause of the spike is government policy,” Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence, wrote in a research note on Monday.

While the latest VIX spike looks reminiscent of the quick August market stress, the underlying drivers are different. The critical difference is that last year’s event was largely a technical break-out due to the carry trade unwind. This can also partially explain why the VIX retraced so quickly in the aftermath.

The current market turmoil is far more fundamentally driven, as a growth scare brought on by tariffs. According to Max Grinacoff, head of US equity derivatives research at UBS Securities LLC, this is even more worrisome and therefore the VIX move will not be faded as quickly.

Intraday volatility has been on the rise, masked somewhat by the 13% plunge in the S&P 500 since Wednesday after the US announced steep, wide-ranging tariffs. That’s providing more opportunities for some investors holding options to trade the swings.

Short-term S&P 500 options volatility has blown out far above longer-dated contracts, signalling long term implied volatility could worsen if economic stress continues to escalate, according to Mandy Xu, head of derivatives market intelligence at Cboe Global Markets.

Xu notes that while one-month implied volatility on the SPX is at a five year high at 41%, one year volatility at 23% is still below 2020 levels, and even below where it was during the 2022 bear market.

“SPX term structure is now the most inverted since Covid, however, most of that is driven by the front-end,” said Xu. That suggests volatility has “scope to increase particularly if recession risk increases.”

Uploaded by Felyx Teoh

- All Malaysia-based carriers failed to meet international punctuality target in January — Mavcom

- Trump floats possible exceptions to 10% baseline tariff, says 'something positive to come' in trade fight with China

- US bond yields and gold rise, dollar down as turbulent week comes to an end

- EU races to expand €2 tril trade network as US links sour

- Navigating Trump’s tariff endgame

- Asean to act as one on US tariffs — PM

- Trump planning order to enable critical metals stockpiling — FT

- Kelantan gets 30% increase in allocation, proof that govt fair to all, says PM

- Cahya Mata Sarawak plans second clinker line to double cement output

- Trump's trade team chases 90 deals in 90 days. Experts say good luck with that