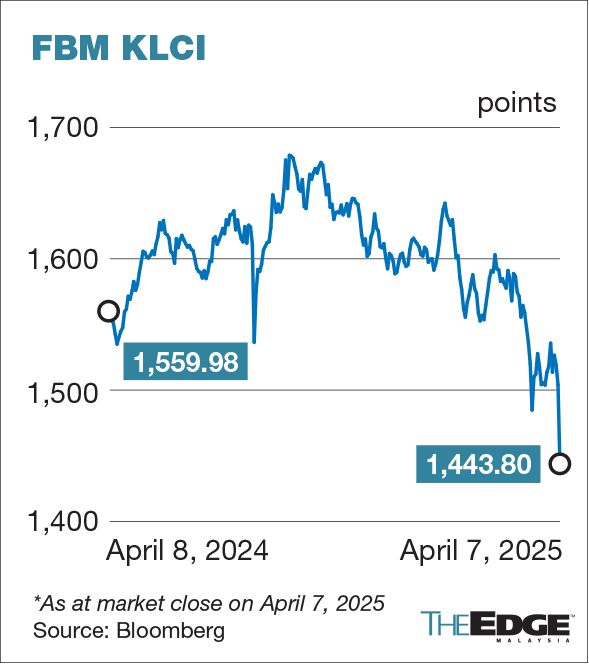

KUALA LUMPUR (April 7): Global markets were in a sea of red on Monday, roiled by tariff fears, and Bursa Malaysia was no exception. The local market saw RM93.15 billion worth of market capitalisation erased as the FBM KLCI recorded its steepest single-day decline since the unwinding of the yen carry trade on Aug 5 last year, dropping 4.01% to close at 1,443.80.

The benchmark index had earlier fallen as much as 85.09 points or 5.65% to 1,419.05 — its steepest one-day drop since March 2008 during the global financial crisis — before easing to 1,443.8.

The sell-off that began last week after the US announced reciprocal tariffs on goods imported from its trading partners intensified as China retaliated by slapping a 34% levy on US goods, while US Secretary of Commerce Howard Lutnick reaffirmed that the Trump administration will not delay the April 9 start date for the reciprocal tariffs.

Regional markets experienced even more significant falls. The Hang Seng Index in Hong Kong tumbled 13.22% in a single day, while the Taiwanese Taiex dropped 9.7% and Japan’s Nikkei 225 lost 7.83%. Trading in Taiwan and Japan triggered circuit breakers earlier in the day.

Other Asean markets, traditionally considered US-friendly, were not spared. Singapore’s STI fell by 7.66%, while the Philippines’ PSEi declined by 4.3%, reflecting the widespread market turmoil.

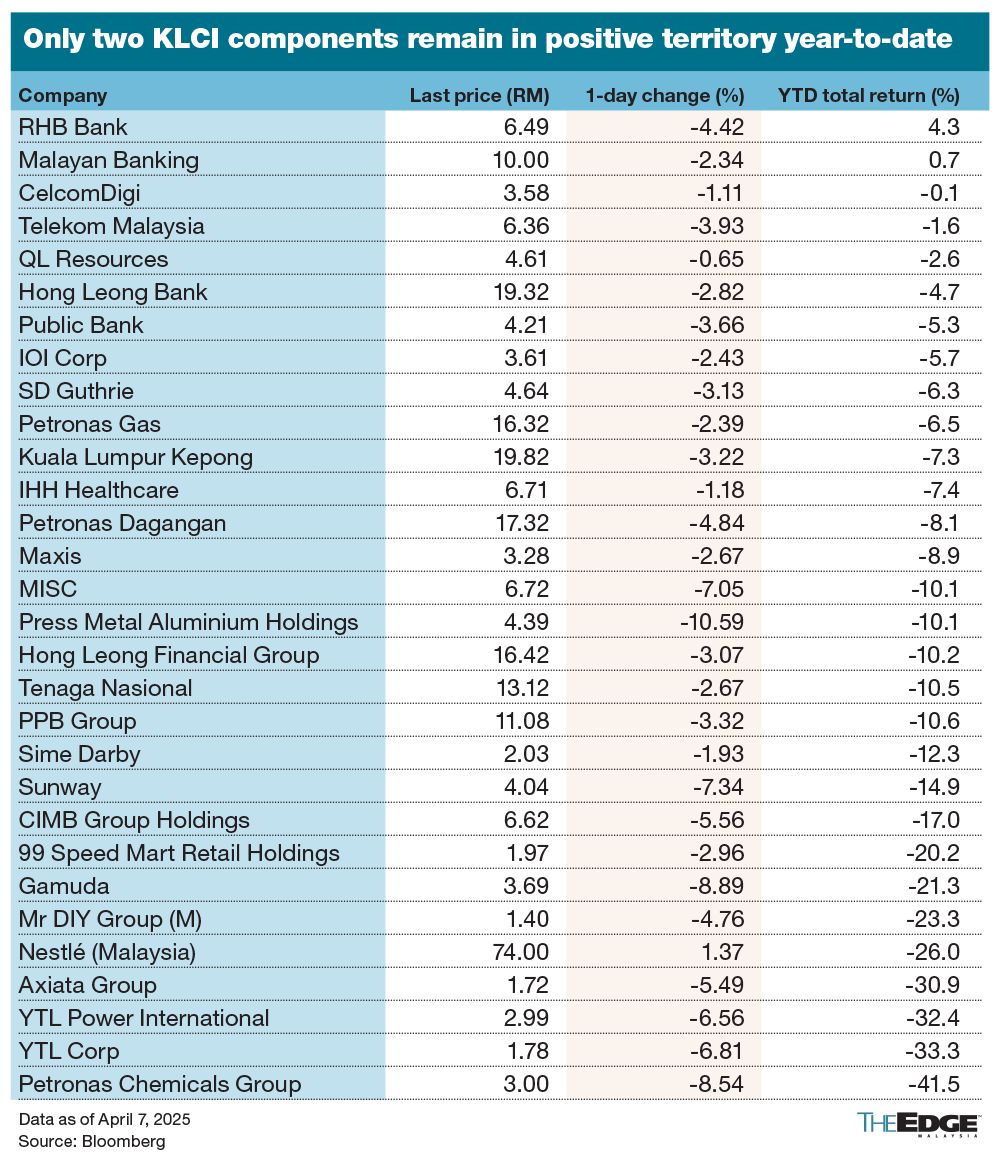

Domestically, the 30 component stocks of the FBM KLCI suffered a combined market capitalisation loss of RM41.06 billion. Nestlé Malaysia Bhd (KL:NESTLE) was the only gainer, while all other constituents fell.

Among the largest losers were Press Metal Aluminium Holdings Bhd (KL:PMETAL), which saw its steepest one-day decline since March 16, 2020, falling 10.59% to RM4.39, Gamuda Bhd (KL:GAMUDA), which dropped 8.89% to RM3.69, and Petronas Chemicals Group Bhd (KL:PCHEM), which went down 8.54% to RM3. The decline at PetChem further solidified its position as the worst-performing KLCI stock year-to-date (YTD), losing 41.5%.

Following Monday's stock market rout, only two KLCI components remain positive YTD (inclusive of dividends): Malayan Banking Bhd (KL:MAYBANK), up 0.7%, and RHB Bank Bhd (KL:RHBBANK), up 4.3% YTD.

Market breadth was overwhelmingly negative, with 1,296 stocks declining compared to just 122 gainers, with smaller-cap stocks facing more significant losses.

The FBM70 Index plunged 7.41%, the FBM Small Cap Index lost 7.63%, while the ACE Index tumbled 8.2% — all marking their largest single-day declines since the yen carry trade unwinding last year.

The top 50 largest companies by market capitalisaton on Bursa Malaysia saw a combined market cap loss of RM52.68 billion, while the next 50 largest companies shed RM16.47 billion, bringing the total loss for the 100 largest companies on Bursa Malaysia to RM69.15 billion.

At the time of writing, European indices were extending their losses, declining by 3% to 4%, while US main index futures remained under pressure, falling by more than 2%.

Kenneth Leong, head of research at Apex Securities, advised a wait-and-see approach as markets continue to absorb the potential impact of reciprocal tariffs. Given the sharp decline in share prices, cutting losses at this stage may be too late for some investors, he observed.

He cautioned investors against rushing to buy the dip, urging them to wait for clearer signs of recovery before making investment decisions. He also noted that US futures markets remain volatile, with Dow Futures slipping 3.22%, reflecting the continued dominance of uncertainty in market sentiment.

Vincent Khoo, head of strategy at UOB Kay Hian, agreed that the structural shift in global trade will lead to extreme market volatility, further exacerbated by an imminent wave of earnings and target price downgrades.

While he acknowledged the possibility that Trump's tariff policy might soften eventually, potentially adopting more of an "exception-than-rule" approach, the market is expected to remain highly defensive for the time being.

For those remaining in equities, Khoo advised sticking to liquid, low-beta and yield-focused stocks, such as those in the consumer, REITs, telecommunications and utilities sectors.

To receive CEO Morning Brief please click here.

- All Malaysia-based carriers failed to meet international punctuality target in January — Mavcom

- Trump floats possible exceptions to 10% baseline tariff, says 'something positive to come' in trade fight with China

- US bond yields and gold rise, dollar down as turbulent week comes to an end

- EU races to expand €2 tril trade network as US links sour

- Navigating Trump’s tariff endgame

- Cahya Mata Sarawak plans second clinker line to double cement output, says performance improving despite legal proceedings

- Penang diversifying exports to offset US tariff impact, says CM

- Gas pipeline fire: 179 witness statements recorded, 769 reports filed

- Asean to act as one on US tariffs — PM

- Trump planning order to enable critical metals stockpiling — FT