With global financial markets still in a tailspin, bond investors will turn to a monthly US payrolls report and a speech by Federal Reserve chair Jerome Powell for clues on the state of the US economy and whether tariffs will shape the Fed’s stance on easing.

(April 4): Traders further boosted their expectations for the Federal Reserve to cut interest-rates this year as fallout from US President Donald Trump’s tariffs convulsed markets for another day.

Money markets now show 100 basis points (bps) of reductions by year-end — equivalent to four 25-basis-point moves — up from about 75bps of cuts before levies were announced. Ten-year yields dipped below 4% once more on Friday to the lowest since before election day, trading at 3.95%. Stocks slumped again, adding to a US$2.5 trillion (RM11.12 trillion) wipeout of US equities.

With global financial markets still in a tailspin, bond investors will later turn to a monthly US payrolls report and a speech by Federal Reserve chair Jerome Powell for clues on the state of the US economy and whether tariffs will shape the Fed’s stance on easing. Markets are already fully pricing in a quarter-point move by June.

“The markets will find it hard not to price in more Fed cuts until risk sentiment stabilises,” said Jordan Rochester, head of macro strategy for EMEA at Mizuho International Plc. “At this stage I suspect they will be cautious to give too much of a steer for markets given the inflationary issue tariffs may cause.”

Equities added to losses on Friday after the S&P 500 Index’s worst day since 2020. US markets are set to open in the red and the moves put MSCI’s global benchmark on track for its biggest weekly loss in seven months.

Still, Trump welcomed the fall in 10-year yields in comments on Thursday. Treasury Secretary Scott Bessent has repeatedly made clear that pushing down that yield — and keeping it down — is a priority for the administration.

European bonds have been swept up in the bond rally, reflecting concerns over the blow to growth from a 20% tariff. The yield on Germany’s 10-year note, the region’s safe asset, has plunged nearly 20bps this week. That puts it on track for the biggest weekly drop since August, taking it to within a few basis points of erasing the surge that greeted the nation’s spending plans in March.

Traders also expect the European Central Bank (ECB) to lower interest rates more sharply, with three quarter-point reductions fully priced in for this year. And the Bank of England is also seen easing 75bps.

For Mark Dowding, chief investment officer at RBC BlueBay Asset Management, the repricing has already gone far enough. He doubts that both the Fed and ECB will be able to respond to tariffs with monetary easing, citing inflationary concerns in the US and an emphasis on fiscal support in Europe, and is instead looking for entry points to bet against bonds once markets settle.

“The rally in bond yields appears overdone,” he wrote in a note. “We think the Fed will do nothing for the foreseeable future, as long as there is not a large rise in unemployment.”

Treasuries have already rallied 3.8% this year, according to a Bloomberg gauge of US debt.

Payrolls loom

In the US, Fed officials have said that a resilient labour market and sticky inflation mean they can afford to stand pat, even as Trump’s tariffs sapped consumer and business confidence. But a weaker-than-expected payroll figure would challenge that view, heightening the Fed’s dilemma over the unusual dual threats of higher inflation and deteriorating growth, and potentially forcing the central bank’s hand to backstop the economy.

Economists surveyed by Bloomberg estimate job growth probably slowed to 140,000 last month, from 151,000 in February, while the unemployment rate held steady at 4.1%. The report is scheduled to be released at 8.30am New York time.

About three hours after those headlines surface, focus will shift to Powell, who will speak on the economic outlook at a public event. Wall Street will be looking for clues on his response to the latest jobs data as well as careening markets in the wake of the aggressive tariff roll-out.

“We do not see any signs of buyer exhaustion in the Treasury market or seller exhaustion in US equities at this point,” wrote JPMorgan Chase & Co strategists including Jay Barry in a note on Thursday. Still, some in the market have expressed concerns about a possible buyers’ strike by overseas holders of treasuries.

Economists generally expect that tariffs will lift inflation and slow growth, keeping the Fed in wait-and-see mode. But the debate over the path of interest rates has ramped up after the tariff announcement. While Morgan Stanley now expects no cuts this year, down from one previously, citing inflation risks, UBS Global Wealth Management see more easing this year.

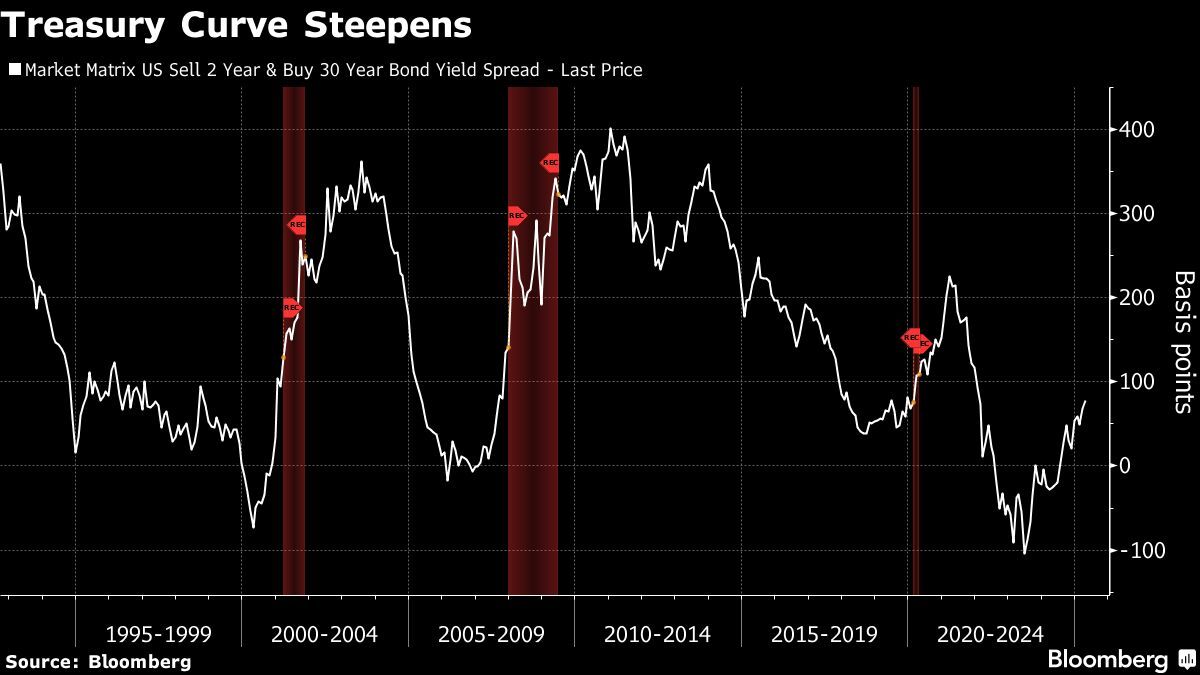

Vineer Bhansali, chief investment officer and founder of Longtail Alpha, said he’s buying two-year notes and selling 30-year bonds, a trade known as a curve steepener. It’s a bet that a slowing economy will force the Fed to lower interest rates, while elevated inflation would lead long-term bonds to underperform.

That growing wager is reflected in the market, with the yield difference between two-year and 30-year bonds widening to 75bps, a three-year high.

“The distribution of possible outcomes has gotten flatter,” Bhansali said. “Anything can happen.”

Uploaded by Felyx Teoh

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Reach Energy, Cahya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Nvidia to produce AI servers worth up to US$500b in US over four years

- Tariff shock awaits China after trade surplus hits US$103 bil