This article first appeared in The Edge Malaysia Weekly on March 31, 2025 - April 6, 2025

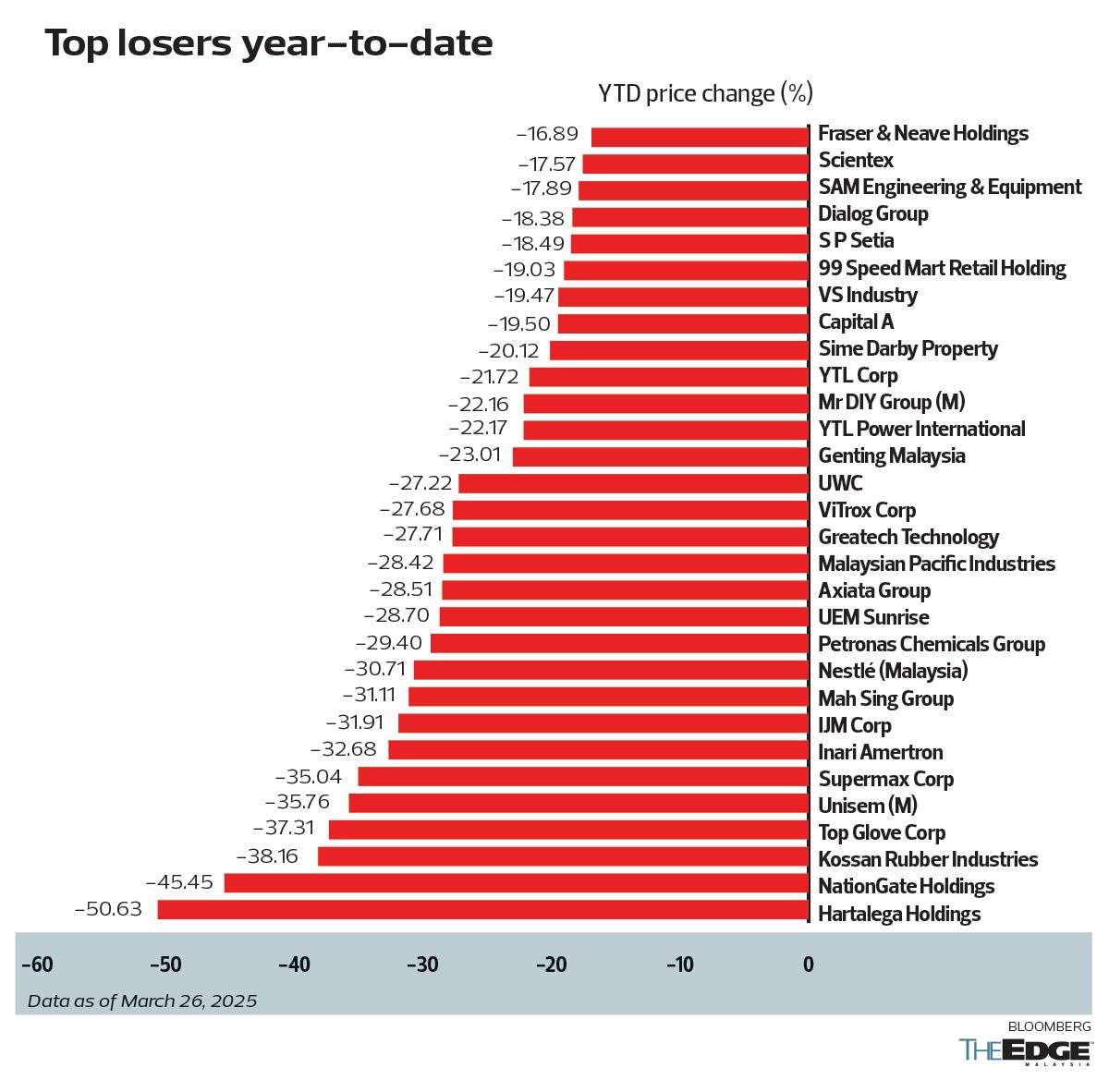

OF the 115 companies that had a market capitalisation of at least RM1 billion as at last Tuesday, 95 - or 83% - have seen a year-to-date (YTD) fall in their share prices. Taking a defensive investment approach in the challenging market, The Edge highlights 10 stocks worth looking at in the second quarter.

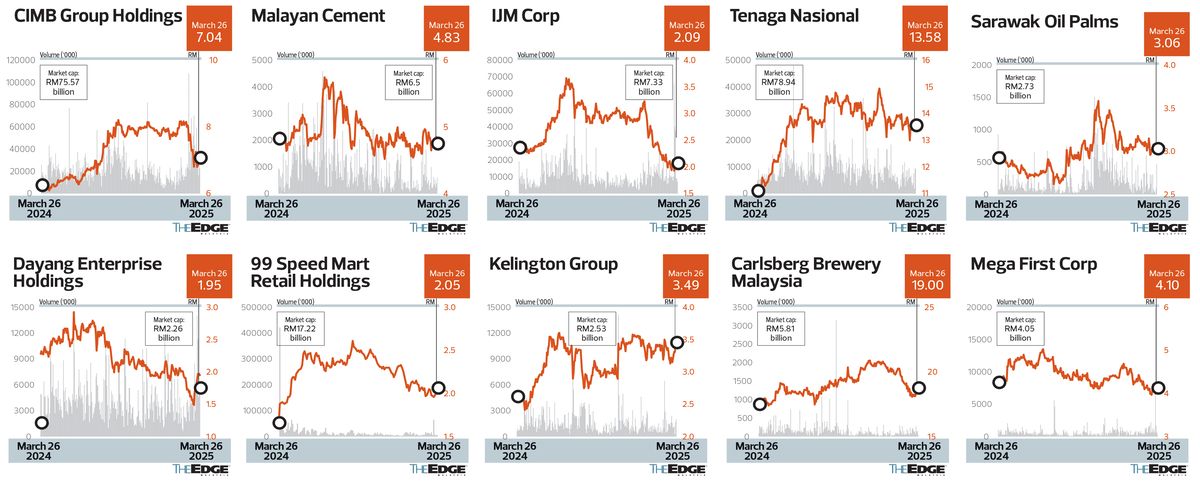

Malayan Cement Bhd

As Malaysia’s largest cement producer, Malayan Cement (KL:MCEMENT) will continue to benefit from ongoing infrastructure developments such as the Penang Light Rapid Transit project and West Ipoh Span Expressway. In addition, it will gain from robust demand for industrial development and property projects.

Another catalyst is the Johor-Singapore Special Economic Zone, as the initiative aims to attract 50 projects in the first five years since establishment.

Malayan Cement, a unit of conglomerate YTL Corp Bhd (KL:YTL), is trading at a 12-month forward price-earnings ratio (PER) of 12.5 times. All six analysts covering the stock have a “buy” call, with a consensus target price of RM6.84, suggesting an upside potential of 41%.

The company’s annual profit is forecast to rise further to RM522 million for the financial year ending June 30, 2025 (FY2025), and RM545.6 million for FY2026, from RM428.7 million in FY2024. The monthly average cement price has held steady at RM380 per tonne since July 2023.

CIMB Group Holdings Bhd

Banking stocks have been relatively less affected by massive foreign fund selling in the first three months of the year. We consider CIMB (KL:CIMB) one of the better picks, given its upside potential of more than 25% against a consensus target price of RM8.85, and decent dividend yield of 5.7%.

While there have been recent headwinds in the Indonesian stock market, its 92.5%-owned Indonesian unit PT Bank CIMB Niaga Tbk, which contributes about 25% of the group’s profit before tax, is expected to record sustainable earnings growth because of credit quality improvement.

This year, CIMB’s net earnings are expected to exceed RM8 billion after hitting a record high of RM7.73 billion in 2024 on the back of healthy loan growth.

Following the completion of its Forward23+ strategic plan, the group unveiled a six-year road map, dubbed Forward30, to accelerate business growth. It aims to raise return on equity to between 12% and 13% by 2027, from 11.2% in 2024, while reducing the cost of funds by 10 to 20 basis points by 2030 in an effort to build a leading deposit franchise.

IJM Corp Bhd

Despite recent online allegations on IJM Corp (KL:IJM) and the proposed Mass Rapid Transit 3 (MRT 3) project, the company has reassured stakeholders that its job prospects remain intact. In fact, it is said to be close to bagging two data centre projects from prominent international clients.

Prior to the selldown in its shares, following the allegations, the construction and property developer also bore the brunt of proposed US rules on advanced chip exports.

Even so, IJM’s order book remained solid at RM6 billion as at end-2024, with RM2.7 billion worth of jobs secured between April and December 2024 (9MFY2025). The contracts are for data centres, electrical and electronics (E&E) manufacturing facilities and logistics warehouse projects.

At a 12-month forward PER of 15.1 times, IJM presents a better opportunity than its peers such as Gamuda Bhd (KL:GAMUDA) and Sunway Construction Group Bhd (KL:SUNCON), whose 12-month forward PER stands at 18.7 times and 20.2 times respectively.

Several analysts have highlighted that the valuation gap between IJM and its larger peers is unjustified, especially as the company has a diversified earnings base with recurring income from tolls and Kuantan Port.

Tenaga Nasional Bhd

As a key proxy for the data centre play, Tenaga Nasional’s (KL:TENAGA) (TNB) risks are less than those of other companies tapping the opportunities in this space.

It expects electricity demand from data centres to reach 5,000mw by 2035, accounting for 15% to 20% of total electricity demand in the country. As at end-2024, 18 data centre projects had been completed, with a total accumulated capacity of 1.9gw.

Tenaga saw a 6.5% growth in electricity demand in 2024, and analysts expect demand to remain solid in the near term. Late last year, the utility giant announced that Peninsular Malaysia’s base electricity tariff would be set at 45.62 sen per kilowatt hour (kWh) for the three-year regulatory period of 2025 to 2027 (RP4), a 14.2% increase from 39.95 sen/kWh set in RP3 (2022 to 2024).

Tenaga is also a proxy for the country’s energy transition growth journey under the National Energy Transition Roadmap, benefiting from the continuous upgrade in transmission and distribution assets.

With a consensus target price of RM16.31, the company’s shares offer an upside potential of about 20%, and a dividend yield of 3.8%.

Sarawak Oil Palms Bhd

Sarawak Oil Palms’ (KL:SOP) earnings per share (EPS) forecasts were revised upwards by 10.8% after net profit expanded 48.5% to RM446.75 million in FY2024 ended Dec 31, 2024, from RM300.87 million in FY2023.

It has a land bank of 122,000ha in Sarawak, of which planted areas account for 82,309ha. Its tree age profile is decent, as two-thirds of its planted area, or 55,463ha, are in the prime production tree age of 11 to 20 years.

SOP also has a downstream complex and seven mills. It aims to achieve a revenue of RMB2.4 million (RM1.46 million) from the debut of its flagship product, AvantHealth Avtriee Tocotrienols, in the Chinese market.

YTD, crude palm oil (CPO) prices have averaged above RM4,700 a tonne. Analysts believe the rollout of the B40 mandate (40% palm oil fuel and 60% diesel) in Indonesia will continue to support CPO prices at high levels.

Other supporting factors for CPO include a tighter supply arising from lower production of fresh fruit bunches.

Of the four analysts covering SOP, three recommend a “buy” and one a “hold”. Based on the consensus target price of RM4.34, the stock has an implied upside potential of 41.7%.

Dayang Enterprise Holdings Bhd

The Sarawak-based oil and gas supportive service provider Dayang Enterprise Holdings Bhd (KL:DAYANG) has not been spared from the recent selldown triggered by subdued market sentiment across the board. Its share price hit a low of RM1.49 on March 12 and has fallen 5.74% YTD.

Analysts believe, however, that Dayang’s prospects are good, supported by its RM5.2 billion order book. Against a backdrop of rising daily charter rates due to the tight supply in the offshore support vessel (OSV) market, the company’s vessel utilisation rates are higher than 70%.

In addition, Dayang is pursuing offshore decommissioning contracts worth RM3 billion locally, including RM1.1 billion in Sarawak. The company is expected to be well positioned for the jobs in the state. Analysts say Dayang, which has a strong net cash position of RM567.64 million, may be looking at onshore maintenance jobs.

Despite Petronas’ reduced guidance for exploration and drilling activities in 2025, offshore service contractors — such as maintenance, construction and modification (MCM) and hookup commissioning (HUC) players, of which Dayang is one — are expected to benefit from the recently awarded pan-Malaysia MCM and HUC service contracts.

Considering the persistent shortage of Malaysia-flagged OSVs, analysts expect higher charter rates in 2025, even though demand may ease slightly.

Analysts expect a slowdown in drilling, and engineering, procurement, construction and commissioning (EPCC) activities this year. They foresee a recovery, however, in the EPCC segment in 2026, based on Petronas’ Activity Outlook report.

Currently, Dayang is trading at a forward PER of 7.95 times and offering an indicative dividend yield of 5%, based on last Thursday’s closing price of RM1.97. Eight analysts recommend a “buy” and one recommends a “hold”. The average target price of RM3.18 implies an upside potential of 61% from its last traded price of RM1.97.

99 Speed Mart Retail Holdings Bhd

Mini-market chain operator 99 Speed Mart Retail Holdings Bhd (KL:99SMART) is probably on the watch list of those who missed the boat during its initial public offering last year at RM1.65 per share.

In an environment of heightened market volatility, analysts view 99 Speed Mart as a defensive investment, although its dividend payments are not expected to be generous, as it caters for the inelastic demand for essentials.

Seven analysts have a “buy” call, while one has recommended a “hold”, with an average target price of RM2.65 — indicating a nearly 33% upside from last Thursday’s closing price of RM2.

The company’s store expansion is progressing steadily, particularly in underserved regions such as Sabah and Sarawak and the east coast of the peninsula. Positive bulk sales trends and strong earnings performance make it attractive.

The group’s core net profit surged 28.5% year on year to RM533.3 million for FY2024 ended Dec 31, 2024, meeting analysts’ expectations. The profit growth was attributed primarily to store expansion and an upward adjustment to the distribution centre fee charged to suppliers.

In FY2024, 99 Speed Mart added 252 new outlets and recorded healthy same-store sales growth of 1.4%, reflecting sustained demand. Total sales transactions grew by 13%.

Looking ahead to 2025, analysts remain optimistic about the group’s plans to open at least 250 new outlets, with the aim of reaching the milestone of 3,000 outlets. The stock has fallen 19% YTD and is currently trading at a forward PER of 30.43 times, with a projected dividend yield of 2% in 2025.

Kelington Group Bhd

Widely regarded as a proxy for global front-end wafer fab expansion, Kelington Group (KL:KGB) was under pressure as the US chip curb ruling sparked selling on semiconductor stocks. Although it has recovered from its lows, it is down 4.2% YTD.

Despite the headwind from President Donald Trump’s administration, analysts remain optimistic about Kelington. Its order book has swelled to RM1.5 billion, while its tender book has ballooned to RM4.2 billion from RM2.62 billion just three months ago. The additional jobs are driven by a strategic partnership with a leading Taiwanese semiconductor company to explore ultra high purity (UHP) job opportunities in Germany and India.

Management is confident about securing contracts in the two new markets by the second or third quarter of this year, bolstered by its strong track record and partnership with a reputable player.

Higher-margin UHP projects are expected to contribute a larger share of the group’s revenue, with analysts projecting its net profit margin to reach a record-high range of 10% to 13% in the coming quarters.

In view of its existing order book and potential job wins, analysts are upbeat on the stock, raising their EPS forecast by 10.7% in February and target price after the annual results for the financial year ended Dec 31, 2024. The average target price is RM4.20, suggesting an upside potential of 22.9%. Four analysts covering the stock have “buy” calls. The stock is currently trading at a forward PER of 16.62 times.

Carlsberg Brewery Malaysia Bhd

The quarterly earnings performance of the two listed breweries on Bursa Malaysia for 4QFY2024 ended Dec 31, 2024, resulted in divergent share price performances.

Carlsberg Malaysia Bhd’s (KL:CARLSBG) share price has fallen 7.7% YTD whereas Heineken Malaysia Bhd’s (KL:HEIM) has climbed 12.1%.

The disparity is due to Carlsberg’s weaker-than-expected performance, due to challenges at its Singapore operations, despite the anticipated boost from front-loading activities during the Chinese New Year celebrations.

Because of the drop in share price, Carlsberg is trading at a more attractive valuation than Heineken.

Analysts have pointed out several factors that may affect Carlsberg’s profitability, including higher advertising and promotional expenses, inflationary pressures and weaker sales in the Singapore market, following the discontinuation of its distribution of Asahi beer. The company is still projected, however, to deliver sales growth of 6% in FY2025, driven by higher contributions from the Sapporo brand, a new addition to its product portfolio, and the full impact of average selling price adjustments last year.

The stock has seven “buy” calls and one “hold”, and an implied upside of 27.4%, based on the average target price of RM24.29. It is trading at a forward PER of 16.04 times compared with its historical 10-year average of 24.7 times and offers an indicative dividend yield of 5.24%.

Mega First Corp Bhd

Mega First Corp Bhd (KL:MFCB) is also another option for a defensive investment, thanks to its resilient business model. Its nearly 11% YTD decline presents a good entry point for investors looking to allocate funds in defensive sectors.

Analysts are confident that the revised agreement for the Don Sahong hydropower project, effective this year, will enhance and stabilise the company’s earnings profile during the 25-year concession period. The agreement incorporates a fifth turbine generator unit and extends the concession duration by just under five years.

Specifically, it is expected to deliver net savings of RM15.3 million from royalty payments, a reduction in annual amortisation charges for concession assets of RM1.6 million, and a 5.5% y-o-y rise in electricity sales volume, as a result of the commissioning of the fifth turbine.

Mega First is also venturing into new areas such as modern farming and hospitals, while continuing to expand its solar capacity to add value to its operations.

The stock has four “buy” and two “hold” ratings and an average target price of RM5.26, implying a 28.2% upside from its last close of RM4.10. It currently trades at a forward PER of 8.27 times, with a projected dividend yield of 2.2%.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Appellate court directs full trial for 10 purchasers of SkyPark @ Cyberjaya over partial CCC

- Former Petronas manager charged with disclosure of confidential information

- Court orders preacher to pay RM2.5m to KJ for defamatory statements on Covid vaccines

- Malaysia Airlines to resume direct flights to Brisbane after two-year hiatus

- CIMB Securities widens WCT's discount as order book challenges mount, keeps 'hold' call

- China speeds up budget spending to counter tariff woes

- Kelantan, Terengganu PKR chiefs retain division head posts

- Malaysia’s mediation role in Myanmar crisis ‘highly significant’, says expert

- A third of German firms mull cutting jobs in 2025, says think tank

- Trump administration seeks records from Harvard on foreign funding and ties