(Photo by Freepik)

This article first appeared in The Edge Malaysia Weekly on March 31, 2025 - April 6, 2025

IN 2024, the local stock market posted its first annual positive return since 2020, outperforming the MSCI Asia Pacific and MSCI Asean indices and prompting hopes that the trend would continue into 2025.

It has not — at least not in the first three months of the year. The local bourse has weakened in tandem with the lacklustre performance of regional markets, with foreign funds making a hasty and voluminous exit, raising concerns over how the bourse will perform in the second quarter.

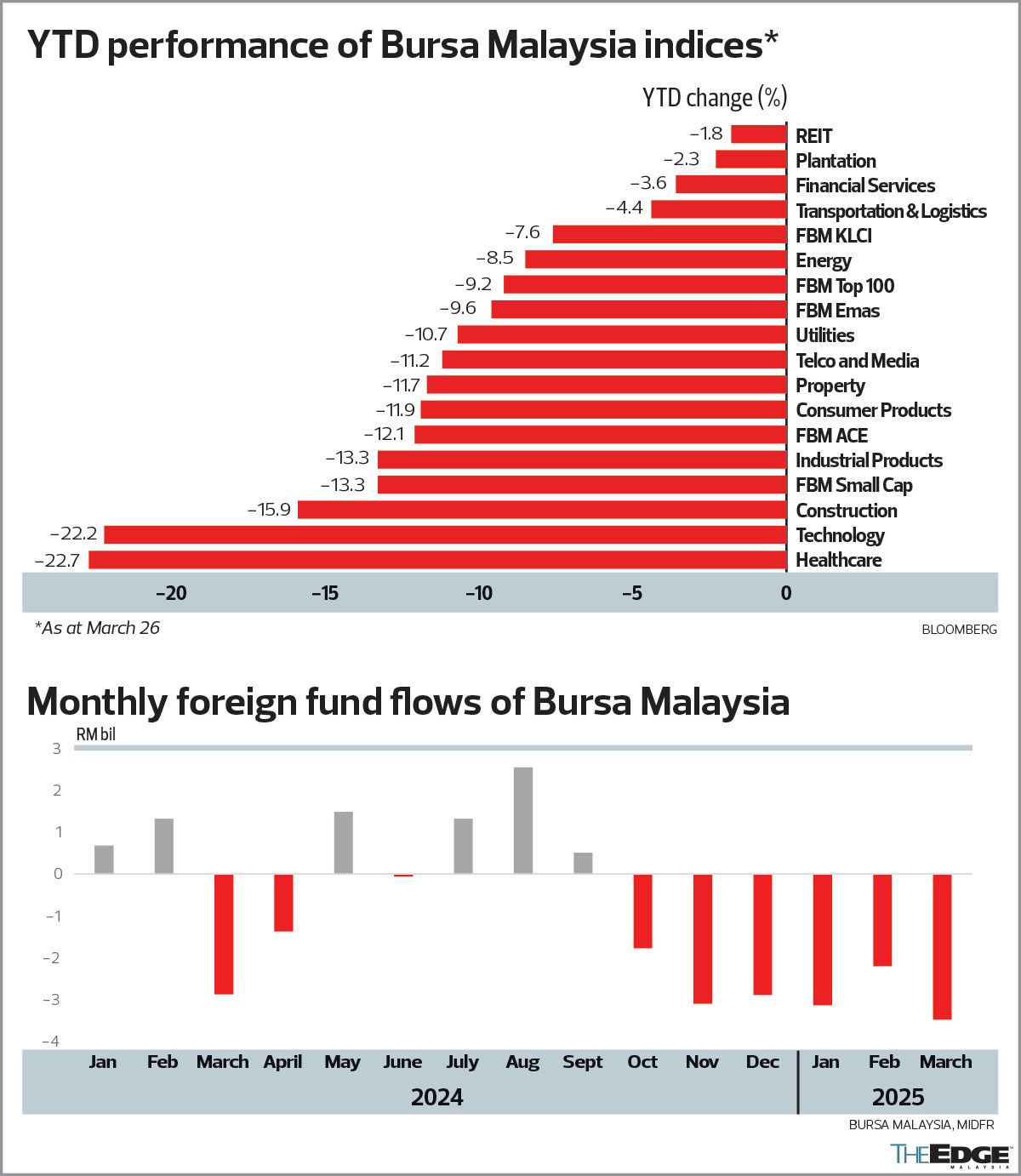

Compared to last year’s closing of 1,642.33 points, the FBM KLCI slipped as much as 10% to a one-year low of 1,478.84 points on March 12, before recovering slightly to 1,535.73 points last Thursday.

Since the start of the year, the benchmark has eased 6.5%. As investors shunned risky assets, the broader market performance of Bursa Malaysia has not been encouraging either, with the FBM Emas Index slipping 9.6% in 1Q, while the FBM ACE Index saw a bigger drop of 12.1%, owing to the lack of liquidity in the small-cap space. Year to date (YTD), the market value of Bursa-listed stocks has decreased 11% to RM1.87 trillion, from RM2.1 trillion as at end-2024.

More concerning, net foreign selling of Malaysian equities has extended to 22 weeks in a row. YTD, foreigners offloaded US$1.96 billion (RM8.68 billion) net of Malaysian stocks, the second hardest-hit market in the region after the US$1.99 billion net outflow from Indonesia.

Indeed, the massive foreign sell-off has caught many analysts and fund managers by surprise. Tradeview Capital CEO Ng Zhu Hann, for one, tells The Edge: “I never expected the magnitude to be that serious in terms of the fund outflow, which is my biggest concern for 2Q.”

Similarly, Victor Wan, head of research at Inter-Pacific Securities Sdn Bhd, says: “Foreign funds are still selling at quite a wide margin. So, that is the biggest concern for us. To me, it’s overdone. The question is, are they coming back? What would entice them to do so?”

However, some quarters had anticipated a reversal of foreign fund flows, pulling out from the emerging markets that had performed well in 2024, as the prospects of aggressive rate cuts in the US have waned since late last year.

As at end-February 2025, foreign shareholding in Malaysian equities stood at 19.6%, near the record low of 19.4% registered in January 2025.

The market sell-off started with the artificial intelligence (AI) chip export curbs announced by former US president Joe Biden on Jan 13, resulting in a slump in data centre-linked stocks and AI proxies. Biden’s move was aimed at retaining the US’ dominant status in AI by controlling supply markets, as well as preventing China from accessing AI chips to build frontier models.

The AI narrative was also hit by the emergence of Chinese AI startup DeepSeek, whose successful large language model rocked global markets.

Analysts expect the risk-off mode in the local market to continue in 2Q amid the lack of catalysts to offset the persistent foreign outflows and escalating uncertainties arising from US tariffs. Emerging markets, especially export-dependent economies, are facing more impact from the tariff moves.

The slump in neighbouring markets — Indonesia and Thailand — also weighed on foreigners’ sentiment on the regional markets, including Malaysia. Thailand and Vietnam have seen YTD net foreign selling of US$1.03 billion and US$879.5 billion respectively. The Indonesian stock market garnered significant attention this month, following a sharp and sudden drop of more than 7% in a single day, driven by concerns over escalating fiscal risks. The benchmark Jakarta Composite Index is down 8.6% YTD.

Thailand, the worst-performing market in Asean, has seen its benchmark index SET Index tumble more than 15% as Southeast Asia’s second-largest economy is saddled with high household debt and borrowing costs.

Back home, healthcare and technology have been the hardest-hit sectors, with declines of 22.7% and 22.2% YTD respectively. Construction, industrial products, consumer products, property, telco and media, and utilities have also sunk more than 10%.

Eyes on Trump’s reciprocal tariffs, data centre concerns

In 2Q, all eyes will be on the reciprocal tariffs set to be announced by Trump on April 2. He said, however, that the tariffs would be more lenient than those levied by trade partner countries.

“I think people are going to be very surprised. It will be, in many cases, less than the tariff that they have been charging us for decades. We have not been treated nicely by other countries, but we are going to be nice. So I think people will be pleasantly surprised,” he was reported as saying.

Tradeview’s Ng observes that due to the reciprocal tariffs, many fund managers are waiting on the sidelines to see the impact of the decision. “Even if the announcement is [more] favourable [than expected], the market will still take time to digest it.”

After witnessing the massive foreign outflow from Malaysia, he is less positive on the 2Q market outlook. “I don’t think it’s time for investors to be aggressive yet. It’s always good to conserve more cash and wait a while and see how things play out in the second half.”

The fear of data centre infrastructure being overbuilt is another concern for Ng, who says “the narrative that gave us a tailwind last year has become a headwind this year”.

Nonetheless, he expects a recovery in the local bourse in the second half of the year, as Malaysia’s economy remains resilient in terms of gross domestic product (GDP), unemployment and consumption data. Although there is a concern over a US recession, he believes the impact on the Malaysian market will not be that significant, except for tech stocks.

Owing to the challenging market situation, Ng says, investors are now looking for only one to two US rate cuts this year.

“It’s significant to determine where fund flow goes. If the US Treasury yield comes down and the US stock market is not doing well, then there’s more incentive for the money to flow back to the emerging markets, China and Hong Kong,” he says. “But if the US Treasury yield remains stubborn and the US stock market is not doing well, the fund managers there can just switch to bonds. They may not want to take any unnecessary risks, especially when Asean looks to be quite gloomy, with the Thai and Indonesian markets underperforming.”

Ng advocates that investors go for safer and dividend names while avoiding high-beta stocks such as tech companies.

“It is still not the time to bottom-fish on concerns over the US economy. So, I don’t think it’s the right time to position our tech sector for any recovery yet,” he says, but suggests investors position themselves to buy blue-chip stocks that have been battered down in order to ride on the recovery.

Among his favourite picks are Duopharma Biotech Bhd (KL:DPHARMA) for rising government budget allocation for the healthcare sector, lower raw material costs and the stabilisation of the ringgit against the US dollar. In the retail discretionary sector, he favours CCK Consolidated Holdings Bhd (KL:CCK), a fully integrated poultry player.

Petronas Dagangan Bhd (KL:PETDAG) is also favoured after a nearly 10% drop in its share price in the past month.

In the banking sector, Public Bank Bhd (KL:PBBANK) is a top pick as the barometer of the domestic economy, and also because it has a lower foreign shareholding than other banks, thus limiting its downside potential. Ng also likes Public Bank’s 44.5%-owned insurer LPI Capital Bhd (KL:LPI), partly for its dividend outlook. Another insurance pick is Syarikat Takaful Malaysia Keluarga Bhd (KL:TAKAFUL), whose share price has rebounded of late.

Although valuations of Malaysia stocks are undemanding — the FBM KLCI is trading at 14.3 times its price-earnings ratio, which is lower than the 10-year average of 16 times — Inter-Pacific Securities’ Wan says the Indonesian and Thai markets may look even more attractive after the heavy selling pressure of the past months. He expects the broader market’s corporate earnings to be lower this year, particularly for export-reliant and electronics firms, but telecommunications, banking and construction firms are likely to see better growth.

MIDF Research notes that market consensus for the FBM KLCI is to register a healthy 6.7% year-on-year (y-o-y) earnings growth in 2025. This compares with the aggregate normalised quarterly earnings growth of 17.7% y-o-y and 4.3% quarter on quarter in 4Q2024.

“Expectation of further rate cuts by major central banks, together with additional stimulus, should be overall positive for the world’s financial liquidity situation in 2025. We believe, however, that the externally driven downside risks to the 2025 outlook are burgeoning. Foremost are uncertainties engendered by US tariff policy, as well as recent underperformance of the US economy,” MIDF says in a March 26 note.

MIDF expects the market will remain volatile in 2Q, but may see some moderating or tailwinds, such as the expectation of US rate cuts, which should result in a weaker US dollar, perhaps then enticing foreigners to return to the Malaysian market. Having said that, foreign fund flows are expected to reverse only when there is more clarity in US trade and tariff policies, it says.

Phillip Capital believes the outlook for the local bourse will be supported by the projected 6% core earnings growth for the FBM KLCI this year, expectations of a stronger ringgit at RM4.30 against the greenback, a robust economic outlook and confidence in government policy execution.

“We reiterate our ‘neutral’ stance on the Malaysian market but lower our KLCI year-end target to 1,700 points (from 1,750 points) based on a target 16 times price-earnings multiple,” it says.

For 2Q, MIDF favours sectors that provide good dividend yields and potential laggards. “We believe banking and REITs (real estate investment trusts) will be a beneficiary of Malaysia’s economy, which is expected to continue growing [albeit at a more normalised pace]. Banks’ loans book are expected to continue growing while asset quality remains stable and improving. [Likewise] with REITs, where the earnings outlook is expected to remain stable, which will be supported mainly by organic growth. In addition, as rates are expected to soften, we expect investors may be looking for assets that will provide them with similar or higher yields.”

Given the defensive approach, the research house also likes the utilities and healthcare sectors, which would provide some stability to earnings. “Furthermore, these sectors are more domestic-focused, which would moderate the downside risks from the external sector,” it adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.