This article first appeared in The Edge Malaysia Weekly on March 31, 2025 - April 6, 2025

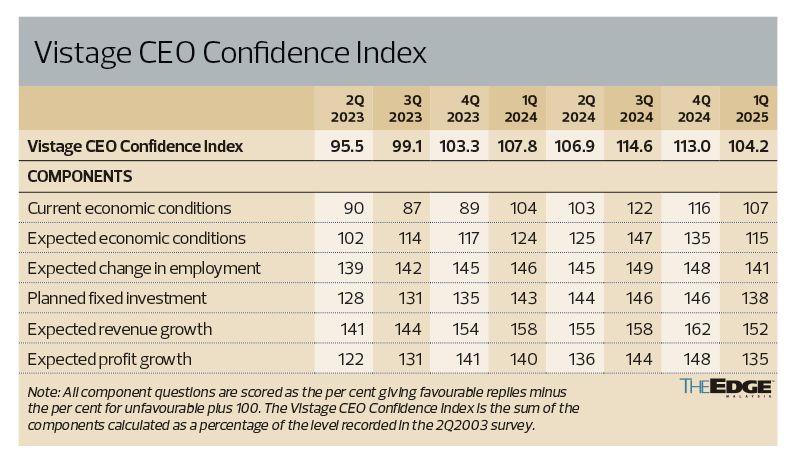

THE latest data signals continued muted trends across the Vistage CEO Confidence Index at the end of 2024. The index dropped to 104.2 in 1Q2025, down from 113.0 in 4Q2024, reflecting a quarter-on-quarter decline of 8.8 points. On a year-on-year basis, the index also fell from 107.8 in 1Q2024. Despite the softened confidence levels, Malaysia’s GDP grew by 5.0% in 1Q2025, slightly below the 5.4% recorded in 4Q2024. This moderation in GDP growth aligns with the decline in CEO confidence, as businesses face mounting cost pressures and heightened uncertainty.

Key indicators

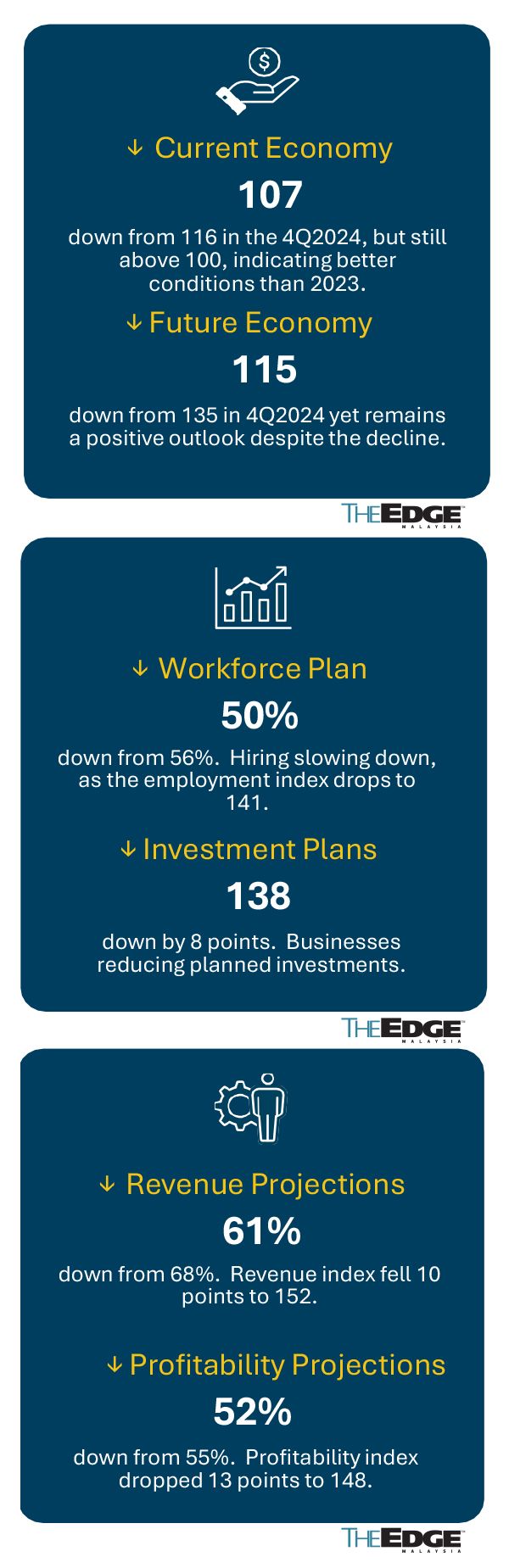

The survey for 1Q2025 indicates a decline in current economic conditions, with the index falling to 107, down from 116 in the previous quarter. Despite this drop, the index remains above 100, indicating a better business environment compared to 2023, when it consistently stayed below 100. This suggests that while business sentiment has softened from its peak of 122 in 3Q2024, it remains more positive than the challenging conditions of 2023.

Expected economic conditions also decreased to 115 in 1Q2025, down from 135 in 4Q2024. Although lower, this figure indicates that businesses still hold a positive outlook for future economic performance.

Over the next 12 months, the employment index for 1Q2025 dropped by seven points from 4Q2024, reaching 141, suggesting a slight slowdown in hiring. The percentage of CEOs planning to increase their workforce fell to 50%, down from 56%. Similarly, businesses are reducing their investment plans, with the planned fixed investment index declining by eight points to 138.

The expected revenue index fell by 10 points to 152, with 61% of CEOs anticipating higher revenues, down from 68% in 4Q2024. Profitability expectations also weakened, as the expected profits index dropped 13 points to 148, with 52% of CEOs expecting higher profits, a slight decrease from 55% in the previous quarter.

Growth in orders and selling prices

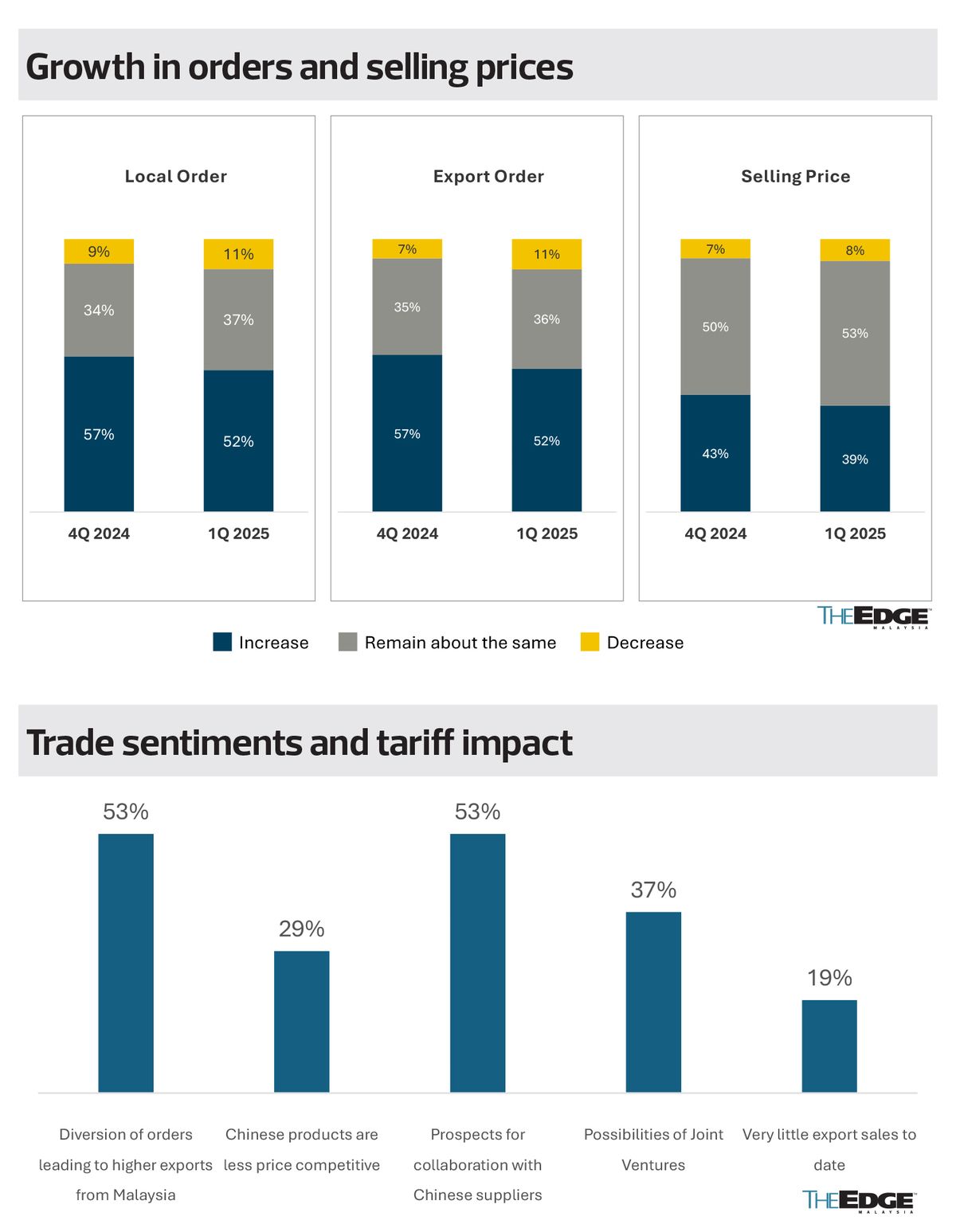

Recent trends show declines in both local and export orders, suggesting a potential slow down in domestic and external demand. In 1Q2025, 52% of CEOs expect an increase in local and export orders. Meanwhile, local selling prices have lightly decreased compared to the previous quarter, with 53% of CEOs keeping their prices unchanged and 8% expecting a reduction.

Cybersecurity awareness and minimum wage impact in 2025

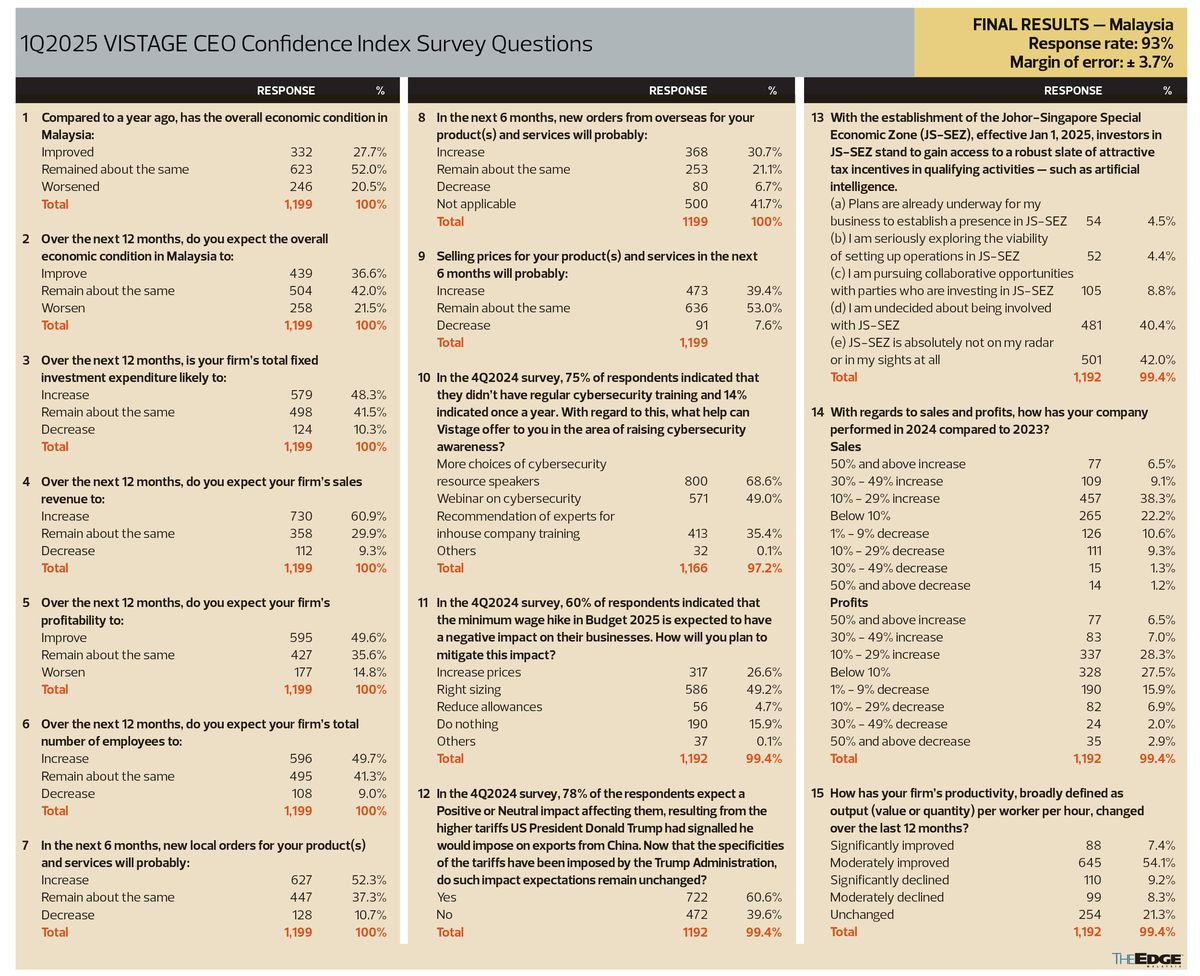

In the 4Q2024 survey, 75% of respondents indicated they do not receive regular cybersecurity training, while 14% reported having it once a year, revealing a significant gap in cybersecurity awareness. However, there are signs of growing interest in addressing this issue. Nearly 70% of CEOs expressed a desire for more cybersecurity resource speakers to improve their understanding. Additionally, between 35% and 50% of CEOs are interested in cybersecurity webinars and expert recommendations for in-house training, indicating a proactive approach to strengthening cybersecurity practices within their organisations.

Sixty per cent of respondents indicated that the minimum wage hike featured in Budget 2025 is expected to have a negative impact on their business. To mitigate these effects, 49% of CEOs plan to implement right-sizing measures, making it the most common strategy. Twenty-seven per cent of CEOs intend to increase prices to offset rising labour costs, while 5% are considering reducing employee allowances. Meanwhile, 16% of CEOs reported that they will take no action in response to the wage increase. This suggests that while most businesses are preparing to adjust their operations, a small portion remains confident in maintaining their current strategies despite the anticipated challenges arising from such a wage hike.

Reasons for continuing trade sentiments

Since the Trump Administration imposed higher tariffs on Chinese exports, 60% of CEOs have maintained their expectations about the impact on their businesses, while 40% have adjusted their views.

Among those who maintained their outlook, 53% expect order diversion to drive higher exports from Malaysia, and an equal 53% foresee collaboration opportunities with Chinese suppliers. Additionally, 37% believe the tariffs could open doors for joint ventures, while 29% view Chinese products as becoming less price competitive. Nineteen per cent of CEOs reported limited export sales, suggesting that the direct benefits from the tariff changes remain modest for some.

These findings highlight a mixed response, with many businesses identifying growth opportunities through increased exports and partnerships, while others remain cautious about the broader implications.

Johor-Singapore Special Economic Zone (JS-SEZ)

The Johor-Singapore Special Economic Zone (JS-SEZ), launched on Jan 1, 2025, has generated mixed reactions. While the initiative offers attractive tax incentives across key sectors such as AI, supply chain, medical devices and aerospace manufacturing, 82% of CEOs remain undecided or uninterested. Fewer than 5% have started plans to establish a presence or are actively evaluating opportunities. Only 9% are seeking collaborative opportunities with parties investing in JS-SEZ.

For those considering participation, the target industries closely align with the JS-SEZ’s key focus areas. CEOs exploring opportunities within the zone are primarily interested in sectors such as artificial intelligence (AI), construction, property development, healthcare, digital services and manufacturing. These industries reflect the zone’s emphasis on fostering innovation and enhancing cross-border collaboration between Johor and Singapore. Additionally, CEOs view JS-SEZ as a strategic gateway to expand their market reach, strengthen supply chains and leverage advanced technological capabilities.

Sales and profits

Company sales and profit performances achieved in 2024 compared to 2023 ranged and varied significantly. The majority saw moderate growth, with 457 companies reporting sales increases of between 10% and 29%, while 337 companies recorded a similar rise in profits. A smaller segment of 77 companies experienced exceptional growth, with both sales and profits increasing by 50% or more. Meanwhile, a group of 14 companies saw sales decline by at least 50%, and 35 companies reported the same level of profit reduction. Additionally, 265 companies recorded minimal sales growth below 10%, while 328 reported little profit improvement.

Across these performance categories, Industrial Markets, Consumer Markets and ICT were the most prominent sectors, reflecting their strong presence in both growth and decline cases. Infrastructure contributed significantly to high-growth companies, whereas construction and property faced notable challenges, particularly in sales performance. Professional services also appeared among the sectors with limited growth, indicating a lower recovery in that industry.

Regionally, businesses in the Klang Valley continued to be the primary drivers of economic activity, with strong contributions from Industrial Markets and ICT. The Southern and Northern Regions showed mixed performances, with some sectors experiencing moderate growth while others faced stagnation. In East Malaysia, infrastructure development played a key role in boosting high-performing companies, though certain industries struggled to maintain stability.

Enhancing business productivity and strategic growth

Over the past 12 months, many firms have experienced positive changes in productivity, with a significant portion reporting moderate improvements (54%). This suggests that businesses are adopting more efficient processes or leveraging technology to enhance output per worker. However, not all firms share this upward trend, and some continue to face productivity challenges, indicating ongoing pressures such as rising costs, labour shortages, or operational inefficiencies. Meanwhile, a substantial 21% of firms reported no change in productivity, suggesting a steady but stagnant performance. These mixed outcomes reflect the varying ability of businesses to adapt to changing market conditions and operational demands.

Many businesses have identified key “Stop/Start/Continue” actions in order to respectively enhance productivity and drive growth. A notable number intend to “Stop” unproductive practices such as complaining, micro managing, procrastinating and wasting resources, reflecting a desire to eliminate barriers that hinder progress. Meanwhile, there is a clear push to “Start” new initiatives, with common themes including the adoption of AI, increased delegation, a stronger emphasis on key performance indicators and diversification. These steps suggest a focus on innovation, efficiency and strategic expansion. At the same time, businesses plan to “Continue” efforts centred on growth, succession planning, business development and overall improvement, demonstrating a commitment to sustaining effective practices. Taken together, these decisions illustrate a balanced approach: eliminating inefficiencies, embracing fresh strategies and building on proven methods to ensure long-term success.

Personal growth and investment

On the personal front. CEOs are also consciously adopting the “Stop/Start/Continue” approach to temper and/or improve some of their behaviours and personal routines. Many aim to eliminate unproductive habits such as complaining, procrastinating and worrying, along with personal health concerns like smoking and excessive eating. To replace these habits, they plan to adopt healthier routines, including regular exercise, meditation, reading and spending more time with family. Additionally, they will maintain beneficial practices such as continuous learning, exercising and maintaining a healthy diet. These personal commitments reflect a holistic approach, reinforcing the notion that self-improvement does align and is congruent with effective business leadership.

In the next six months, CEOs will prioritise traditional and stable investments. Equities and fixed deposits remain the most popular choices, with 48% and 45% of CEOs favouring these options respectively. Local real estate continues to attract interest, with 34% of respondents indicating plans to invest in this sector. Diversified financial products such as unit trusts and mutual funds are gaining traction, with 25% showing interest, while 19% of CEOs consider gold and silver as hedges against market volatility. Cryptocurrency is viewed favorably by 15% of respondents. Other investments such as bonds and foreign assets, remain less favoured.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Asian stocks set for mixed open, US futures dip

- Penang's Mutiara Line LRT project on track and on schedule, says project owner

- Crude palm oil's discount to soybean likely until 3Q, may spur Indian demand — analysts

- First shockwaves of Trump’s tariffs are about to hit the world economy

- Nourishing a healthier world via Malaysian palm oil

- Oil retreats with Ukraine-Russia truce falls apart, US-Iran talks in focus

- Crude palm oil's discount to soybean likely until 3Q, may spur Indian demand — analysts

- AI revolution in Malaysia’s accounting sector: A pathway to digital transformation

- First shockwaves of Trump’s tariffs are about to hit the world economy

- Penang's Mutiara Line LRT project on track and on schedule, says project owner