This article first appeared in The Edge Malaysia Weekly on March 31, 2025 - April 6, 2025

CITING “manageable” inflation and the strength of domestic demand in affirming Malaysia’s 2025 official economic growth forecast of 4.5% to 5.5% when releasing its annual flagship publications last week, Bank Negara Malaysia doused traders’ side talk of an overnight policy rate (OPR) cut this year amid concerns over US tariffs torpedoing global growth.

While the central bank appears to have pencilled in Malaysia’s 2025 GDP growth at about 4.9%, moderating from 5.1% in 2024, according to our back-of-the-envelope workings based on appended data, observers agree that even a 4.5% year-on-year (y-o-y) growth this year is still very decent amid global policy uncertainties, and may even be at par with China. After all, most economists think China’s economic growth, despite a slew of upgrades following a robust showing in early 2025, will be shy of the official target of “around 5%”.

“The materialisation of [heightened external risks such as those from restrictive and retaliatory trade policies, geopolitics and commodity price disruptions] will determine where we end up in our forecast range of 4.5% to 5.5%,” Bank Negara Malaysia governor Datuk Seri Abdul Rasheed Ghaffour said when releasing the central bank’s Annual Report 2024 (AR2024), the Economic and Monetary Review 2024 (EMR2024) and the Financial Stability Review for the second half of 2024 (FSR 2H2024) on March 24.

“While [an OPR cut] cannot be ruled out, especially if tariff disruption weighs heavily on global growth, the chances for a pre-emptive cut by Bank Negara may not be high for the time being,” Maybank Investment Banking Group head of fixed income Winson Phoon tells clients in a note dated March 27, which mentioned a “modest increase in chatters for a potential OPR cut of late”.

In short, Phoon says policymakers can typically tolerate transitory supply shocks — unless such shocks are multiple and persistent, or accompanied by demand-pull pressures, which may trigger second-round effects or de-anchor inflation expectations, thereby altering price-setting behaviour. “We believe the current global and domestic [environment] poses two-sided risks — downside to growth and upside to inflation — [warranting] Bank Negara to stay the course until destabilising signs emerge,” Phoon adds.

Indeed, based on the policy stance and analysis across several boxed articles in its annual, economic and monetary reports, Bank Negara is likely to keep its OPR unchanged at 3% this year, unless growth weakens substantially or should inflation prove sticky and not transitory.

Bank Negara, which unwound pandemic-time monetary policy accommodation with a cumulative 125 basis-point OPR increase between May 2022 and May 2023 — without tightening to the 3.25% OPR level kept between January 2018 and May 2019 even as the US Federal Reserve hiked rates by 500 basis points from March 2022 to July 2023 (before trimming rates by 100bps between September and December 2024) — deems the current 3% OPR rate as one that is “appropriate and supportive” of [Malaysia’s] economy”.

Most economists continue to see Bank Negara keeping the OPR unchanged this year, despite headline inflation potentially rising beyond the longer-term average of 2%.

“Given the upside risks to inflation while the external outlook is subject to potential pitfalls owing to heightened uncertainties surrounding global trade policies, we expect the OPR to remain unchanged at 3% for now. Bank Negara reiterated that domestic demand remains supported by a healthy labour market, robust investments and supportive fiscal policy, which will continue to keep the output gap positive for the second straight year in 2025,” UOB Bank Malaysia senior economist Julia Goh writes in a March 25 note.

“With Bank Negara projecting steady growth and manageable inflation, we continue to expect the Monetary Policy Committee (MPC) to remain patient and keep the OPR at 3% in 2025, adopting a wait-and-see stance amid an uncertain global environment,” HLIB Research economist Felicia Ling writes in a March 25 note.

Inflation higher but contained

What could Bank Negara be looking out for? Persistent signs of higher inflation, says Maybank’s chief economist Suhaimi Ilias, who also expects the OPR to be kept at 3%, while noting that Bank Negara had not found it necessary to adjust monetary policy in direct response to transitory shocks such as during past adjustments of domestic fuel prices.

“However, when the shocks have a more enduring and broader impact on inflation with spillovers on inflation expectations, monetary policy will be adjusted accordingly, for instance, during the post-pandemic period between January 2022 and December 2023 when the OPR was raised from the record-low during the pandemic shock as a result of global supply disruption coupled with a shift in domestic demand that drove inflationary pressures higher and [was] more persistent,” Suhaimi tells clients in a note, acknowledging that the downside bias to economic growth on external factors and the upside risk to inflation “poses a challenge” to Bank Negara’s dual mandates of sustainable growth and price stability.

Primarily a “blunt” demand management tool, which Bank Negara says works with up to a two-year lag, the OPR is pre-emptively adjusted to ensure that inflation expectations remain well-anchored in the face of demand-pull inflation, potential wage-price spirals and second-round effects from supply shocks.

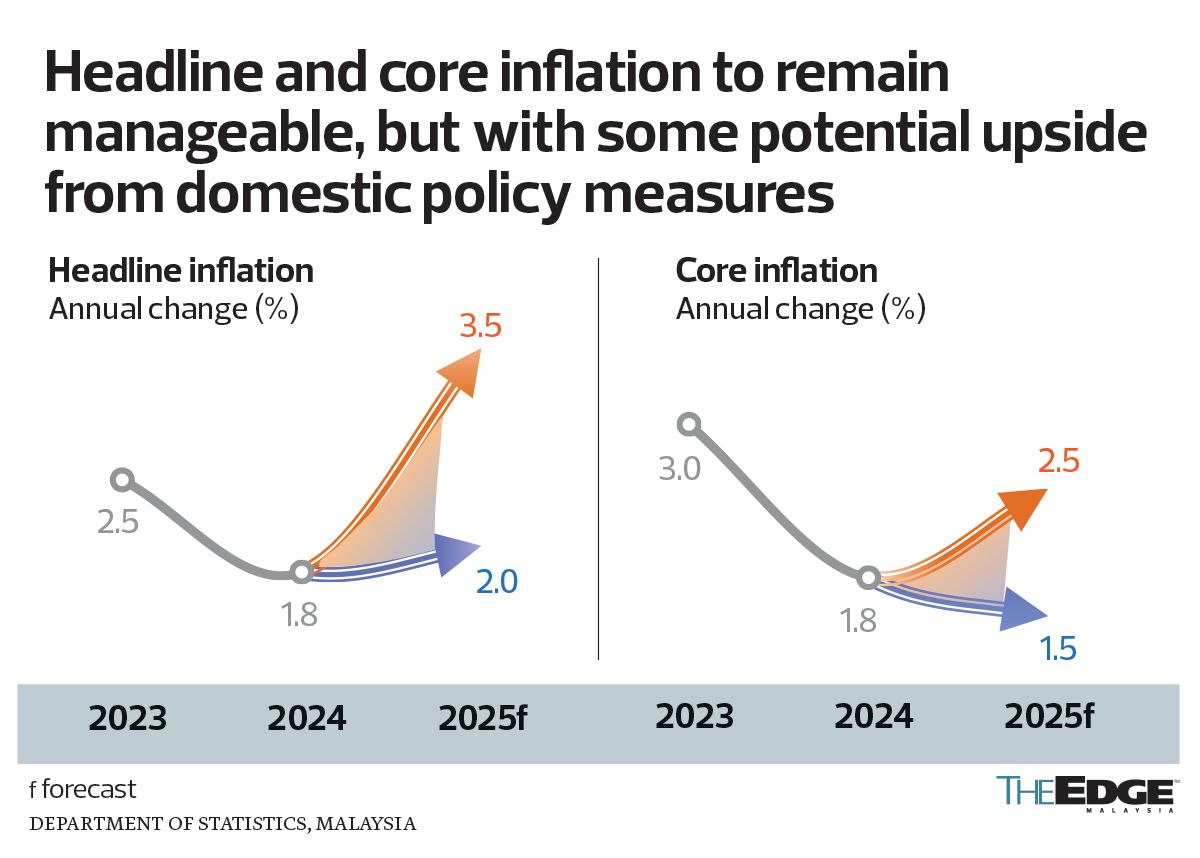

Inflation remains contained for now. Headline inflation eased from 1.7% in January to 1.5% in February 2025 while core inflation (which excludes volatile items like fresh food) inched higher to 1.9% in February 2025 compared with 1.8% in January. This remains below the longer-term average of 2%.

Compared with 1.8% (both core and headline) in 2024, Bank Negara expects core inflation to range between 1.5% and 2.5% in 2025 and headline inflation to range between 2% and 3.5%.

“Going into 2025, we expect inflation to remain manageable. While domestic policy measures such as fuel subsidy rationalisation may introduce some upward price pressures, these are expected to remain contained given the broader environment of moderating global costs and the absence of excessive demand-driven inflation,” said Abdul Rasheed, who also notes that cost-of-living concerns persist despite the moderation in overall inflation.

Not for solving cost-of-living issues

“Since 2019, nominal wage growth has lagged behind the price increases, eroding purchasing power, particularly for essential goods such as food. This impact is most pronounced among lower-income households, which allocate a larger and increasing share of their income to basic necessities like food and housing. Put simply, for every RM100 the B40 earned in 2022, RM52 was channelled towards basic needs, affecting their ability to spend on important services such as insurance and financial services, as well as on discretionary items,” Abdul Rasheed said.

While acknowledging cost-of-living pressures felt by households whose incomes have not risen as fast as prices, especially food inflation among vulnerable low-income households, Bank Negara nonetheless reiterated in its 2024 annual report that monetary policy “is not sufficient on its own to fully address the issue” apart from ensuring that inflation remains low and stable as inflation is also driven by factors beyond demand. The latter include regulatory changes such as new taxes, tariffs or stricter environmental policies that can increase production cost as well as supply shocks that can be caused by a disruption in supply of input, factory closures or export restrictions in key commodities such as that stemming from the Russia-Ukraine conflict that drove up prices in 2022.

“Unlike monetary policy, which is a blunt tool, fiscal policy can be more targeted to help reduce living costs for specific groups. For example, the government can help to manage these rising expenses by providing targeted subsidies or tax breaks to households. Furthermore, when supply disruptions from events such as adverse weather cause general prices to increase, the government can give cash assistance to affected households to supplement their income. Alternatively, financial assistance or subsidies can be provided to businesses to help them manage the higher production costs from the supply shocks, which could lower the extent of cost pass-through and the eventual price increases to consumers.

“However, this would increase fiscal burden and limit investments in other critical areas such as health, education and infrastructure. Therefore, this approach should be done judiciously and as a temporary measure as it only addresses the symptoms rather than the root cause of cost-of-living concerns,” the central bank added, noting that fiscal policy can also be used to raise the economy’s productive capacity by encouraging investments via favourable tax policies for specific sectors like high-growth-high-value (HGHV) industries and promoting research and development (R&D) initiatives.

The central bank also acknowledged that price ceilings on certain essential items can help make goods more affordable for the lower-income bracket, but said price controls “should not be applied for too long because they distort the determination of prices by market”.

Calling for structural reforms that address the root causes of price pressures and help households better tackle future cost-of-living challenges, Bank Negara noted that extended periods of price controls “could promote excessive consumption and wasteful behaviour, which can lead to supply constraints” on top of being an inefficient allocation of resources.

“By aligning monetary and fiscal policies with structural reforms, policymakers can create a cohesive framework that keeps inflation low and stable, and ensures the cost of living remains manageable.”

Not a ringgit boost

An OPR hike is also not expected at the current juncture, even though Abdul Rasheed acknowledged last week that “downside risks arising from fewer US Fed rate cuts and uncertainties over the impact of US trade policies could weigh down the ringgit”.

Even though there are concerns about imported inflation and capital outflow, with the ringgit depreciated about 15% against the US dollar since the 3.80 peg was lifted in 2005 and skidding 2.7% against the greenback in 2024 alone, Bank Negara has repeatedly stated that the ringgit’s weakness is not driven by fundamentals but a reflection of interest rate differentials with the US plus general US dollar strength amid heightened risk.

“Going forward in 2025, foreign inflows following narrower interest rate differentials between Malaysia and the advanced economies are expected to lend support to the ringgit … Despite the continued influence of external factors on the ringgit’s trajectory, Malaysia’s favourable economic prospects and domestic structural reforms are expected to cushion against these external shocks. The ringgit’s value continues to be market determined, and Bank Negara remains committed to ensuring an orderly functioning of the domestic foreign exchange market,” the governor said.

At the time of writing, the ringgit was up about 1% against the US dollar year to date. According to Bank Negara data, the ringgit had depreciated by 0.02% on a nominal effective exchange rate (NEER) basis against Malaysia’s major trading partners year to date (as at March 21), after appreciating 7.5% in 2024.

Current account in surplus, solid domestic demand

Bank Negara expects Malaysia’s current account balance to “sustain a surplus in 2025”, ranging between 1.5% and 2.5% of GDP, “driven by higher goods surplus and lower services deficit following continued improvement in inbound tourism”.

“The government is also proactively considering measures to sustain the current account surplus in 2025, which include enhancing export competitiveness, reducing import reliance and advancing the tourism sector,” the governor said, allaying any concerns among those closely tracking Malaysia’s balance of payments.

To support Bank Negara’s stance on the strength of domestic demand and good fundamentals cushioning against external shocks to sustain growth amid uncertainties, Abdul Rasheed shared several “interesting household consumption patterns” in 2024.

“Car sales made a new all-time high of around 815,000 units. Spending on restaurants and hotels grew 11.8% above the long-term average of 7.1% (2011-2019). Malaysians continue to travel and spend abroad, registering a year-on-year growth of 15.1% (2011-2019, average: 7.7%). In short, household spending has been really forthcoming. In 2025, household spending will continue to be the anchor of growth and is projected to expand at a faster pace of 5.6%,” he elaborated, also noting a historic high labour force participation rate of 70.5%, low unemployment of 3.1% in 2025 as well as better income prospects for at least four million workers benefiting from a higher minimum wage and the civil servant salary increment.

Investments are also projected to expand 9.3%, with investment approvals reaching RM378.5 billion in 2024 compared with RM329.5 billion in 2023.

For 2025, Abdul Rasheed said “monetary policy remains focused on maintaining an environment of price stability conducive to sustainable economic growth in Malaysia”.

“Amid global policy uncertainties, we are following these developments closely and remain vigilant against potential spillover effects on Malaysia’s economy. Going forward, our monetary policy approach will continue to be data-driven amid the evolving economic landscape. Monetary policy will continue to be guided by the balance of risks surrounding the outlook on Malaysia’s inflation and growth.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Yellen says sell-off in Treasuries shows US confidence loss, not dysfunction

- China suppliers mock tariffs with Nike, Lululemon deals on TikTok

- Reach Energy faces trading suspension, possible delisting, as regularisation plan deadline extension rejected

- Reach Energy, Cahaya Mata, Able Global, Pestec, Bina Puri, Jentayu Sustainables

- Malaysia declares state funeral for Tun Abdullah Ahmad Badawi

- Asian stocks set for cautious day as US trade probes sow more anxiety

- South Korea unveils US$23 billion support package for chips amid US tariff uncertainty

- US stocks, bonds climb after week of upheaval

- Tariff-fueled market rout cost Chicago’s pensions $1 billion

- Norinchukin dodges Trump’s market chaos after selling Treasuries