This article first appeared in Capital, The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

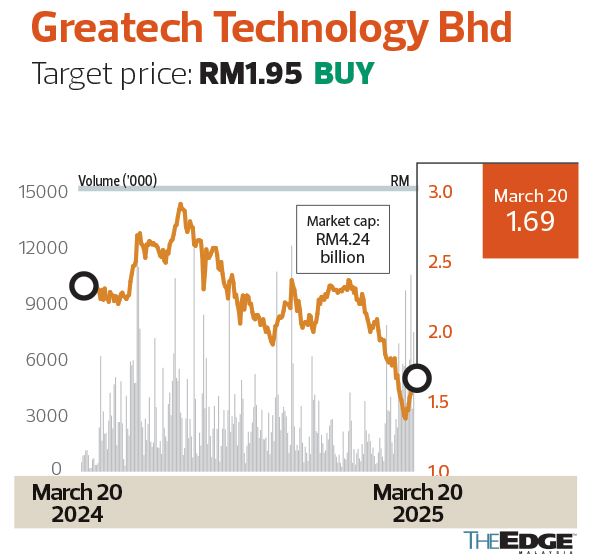

Greatech Technology Bhd

Target price: RM1.95 BUY

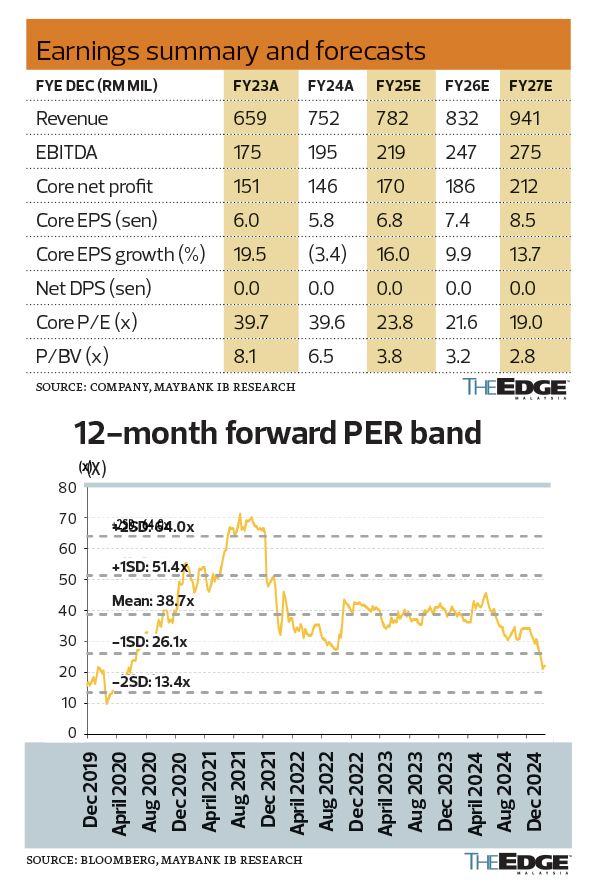

MAYBANK INVESTMENT BANK RESEARCH (MARCH 20): We opine that Greatech Technology Bhd’s (KL:GREATEC) recent acquisition has the potential to accrete long-run value as it diversifies exposure towards higher value-add process automation. With a weaker outlook from US tariff tiff uncertainties largely priced in, we upgrade our call on Greatech to a “buy” from “hold”. Our target price of RM1.95 (FY26F PER of 26 times, at -1 standard deviation to five-year mean) and FY25-FY27F earnings are unchanged.

As its fundamentals remain largely intact, Greatech is well positioned to capitalise on global IR 4.0 (Fourth Industrial Revolution) and factory automation trends.

On Feb 28, Greatech announced it had entered into a sale and purchase agreement for the purchase of 100% equity interest in Manz Slovakia SRO (MSSRO) — a contract manufacturer of standardised/custom equipment — for €1 million (RM4.79 million). MSSRO is a wholly-owned subsidiary of Manz AG in Germany which filed for insolvency on Dec 20, 2024.

MSSRO is profitable (FY24: €744,000) and with an acquisition multiple of just 1.3 times FY24 earnings, we view the acquisition favourably. The acquisition has the potential to drive synergies for Greatech’s move up the value chain from factory automation to process automation and mechatronics, with MSSRO acting as a foreign outpost for EU-based customers. Greatech’s last acquisition (100% equity in Ireland-based Allied Automation for €1 million in 4Q23) was a success, contributing €7 million to its top line in FY24.

Greatech had a healthy outstanding order book of RM785 million as at Feb 13, sufficient to comfortably last four quarters. Despite falling short of its own internal order book target in FY24, management targets to secure RM900 million worth of new orders in FY25, primarily from the solar and e-mobility segments. The medical segment is expected to post revenue growth of more than 50% in FY25.

We believe value has emerged following the sentiment-driven correction afflicting the tech sector that has seen Greatech’s share price retrace 30% YTD. Current valuations are attractive at an FY26 PER of 21 times (five-year forward mean: 39 times). Accounting for the potential imposition of blanket tariffs on Malaysia, we take comfort that Greatech may be able to pass on near- to medium-term marginal cost increases to its customers, owing to force majeure caveats.

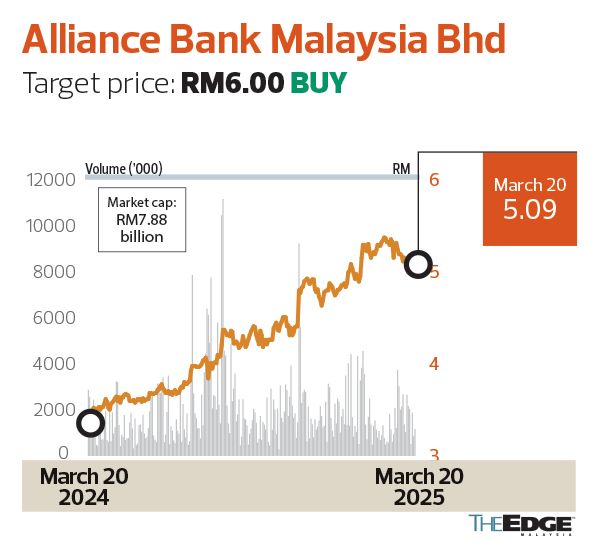

Alliance Bank Malaysia Bhd

Target price: RM6.00 BUY

CIMB SECURITIES (MARCH 20): We get the sense that Alliance Bank Malaysia Bhd (KL:ABMB) will likely experience decent enhancement to Common Equity Tier-1 (CET-1) capital ratio from Basel III changes, while it continues to see robust momentum from new small and medium enterprise (SME) and individual customers. The estimated net impact from Basel III changes will likely be an increase of 20 to 30 basis points to its CET-1 ratio. The group’s CET-1 ratio stood at 12.4% at end-2024.

We expect overall loan growth to slow down from the robust annualised rates of 12.5% in 3QFY25 and 12% in 2QFY25. The final quarter of Alliance Bank’s financial year ending March is usually quieter owing to several seasonal holidays. Looking ahead, the company’s growth is likely to taper down to its targeted 8% to 10% level for the next financial year (FY25), partly owing to the higher-base effect. Growth is expected to continue to be driven by the residential mortgage, non-residential mortgage and SME segments.

We maintain our “buy” call and target price of RM6, based on a fair P/BV of 1.2 times.

Kuala Lumpur Kepong Bhd

Target price: RM25.40 BUY

RHB RESEARCH (MARCH 19): We remain upbeat on Kuala Lumpur Kepong’s (KL:KLK) prospects after meeting with its management. FY25 (ended Sept 30) should bring stronger earnings, as fresh fruit bunch output from Indonesia is set to recover while costs will likely moderate further. However, negative refining margins remain a sore point.

KLK expects costs for FY25 to remain below RM2,000 per tonne, on the back of lower fertiliser costs. Fertiliser requirements in 1H25 were secured at prices that were 15% to 20% lower y-o-y. Management expects labour cost to slightly increase, from the minimum wage hike and 2% Employees Provident Fund contribution for foreign workers. These will impact less than 2% of KLK’s bottom line. We cut cost assumptions to reflect the lower fertiliser costs for FY25.

KLK’s 2,500 acres of land in Kulai, Johor, has been earmarked for an industrial park development, and it is currently in the process of locking in potential joint venture partners, which will benefit the company in terms of land sale gains and property development profits. We maintain our “buy” call and raise our target price from RM24.80. KLK’s shares are trading at a reasonable 2025F PER of 19 times, versus its peers’ range of 18 to 23 times.

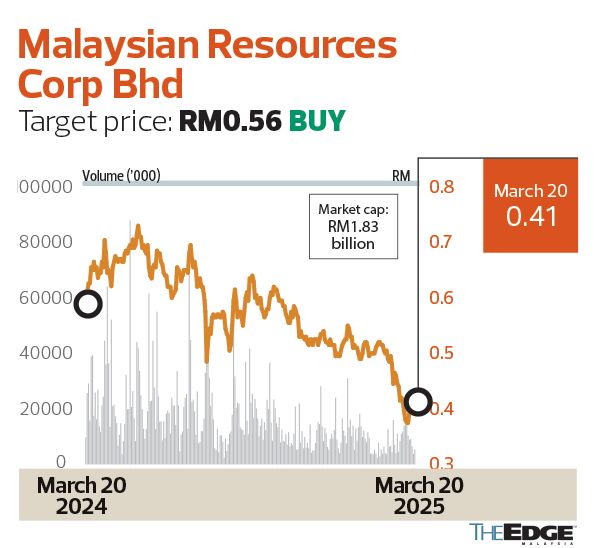

Malaysian Resources Corp Bhd

Target price: RM0.56 BUY

MIDF RESEARCH (MARCH 19): Malaysian Resources Corp Bhd (MRCB) (KL:MRCB) announced on March 17 a strategic land swap deal involving its subsidiaries and Cyberview Sdn Bhd, which is majority owned by the Ministry of Finance (92.24%). The strategic swap will allow MRCB to consolidate its land ownership in the prime development zone of Cyberjaya.

The new acquisitions represent significant opportunities for MRCB, providing strategic land bank enhancement and underpinning its long-term growth potential in integrated developments. The acquired parcels are well positioned with connectivity to Putrajaya and Kuala Lumpur, ensuring strong demand potential for future developments.

There is minimal immediate financial impact from the transactions apart from the disposal gain of RM22 million in FY25. The actual effects of the proposed acquisitions on earnings and consequently EPS of the group for subsequent financial years will depend on earnings contribution from the development of the project land.

We maintain our earnings estimates following our previous downward revision of earnings for FY25E/FY25F by 18.4% post-4QFY24 results, as the recent land disposal and acquisition agreements align with MRCB’s long-term strategic initiatives and are within expectations.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia hit with 24% US reciprocal tariff effective April 9

- CIDB issues apology, retracts statement on devastating gas pipeline inferno

- Apple production hubs, including Malaysia, hit by tariffs

- Malaysian stocks decline following Trump reciprocal tariff

- Global companies face a new reality of Trump tariff chaos

- Nike falls as Trump’s reciprocal tariff plan sinks retailers

- China services growth picks up with economy pressured by tariffs

- OCBC aims to fund S$17b over five years to support FDI into United Kingdom

- Australia says US tariffs 'not act of a friend' but rules out reciprocal move

- Amazon adds 11th hour intrigue to TikTok acquisition drama