This article first appeared in Capital, The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

EXCHANGE-traded funds (ETFs) have garnered widespread popularity in developed markets like the US and Europe, thanks to their cost-effectiveness, liquidity and diversification benefits.

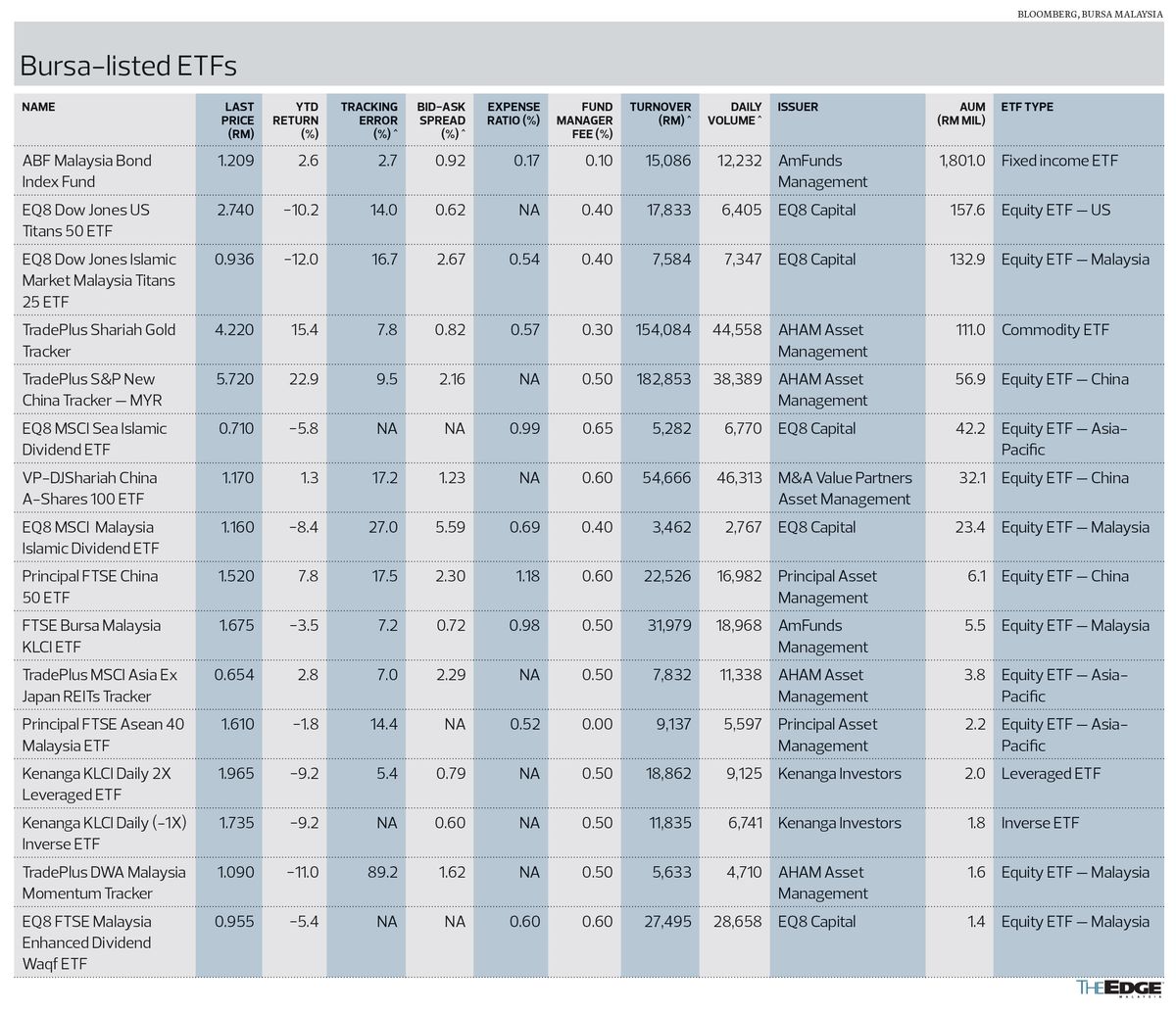

In Malaysia, ETFs are still a relatively underutilised investment option. The first ETF listed on Bursa Malaysia was the ABF Malaysia Bond Index Fund, a bond ETF, in July 2005. This was followed by the launch of the first equity ETF, the FBM KLCI ETF — formerly known as the FBM30ETF — in 2007, which tracks the local benchmark.

Despite being introduced in 2005, ETFs have yet to gain significant traction among retail and institutional investors in Malaysia. Currently, the 17 ETFs listed on Bursa Malaysia collectively manage about RM2.4 billion in assets — a small fraction compared to the total assets under management (AUM) of Malaysian unit trust funds of RM546.08 billion.

To compound the challenges, AHAM Asset Management Bhd recently announced the closure of two ETFs — TradePlus DWA Malaysia Momentum Tracker and TradePlus MSCI Ex Japan REITs Tracker. Both ETFs, launched nearly five years ago, were shut down due to their small fund sizes and high ongoing expenses, which led to disproportionately high expense ratios.

Several factors contribute to the limited popularity of ETFs in Malaysia. One major challenge, as cited by ETF operators, lies in distribution. Unlike unit trusts, which benefit from active promotion by commission-earning agents, ETFs are traded like stocks and lack similar marketing efforts. This has resulted in low awareness and persistent misconceptions about ETFs, with many investors erroneously associating low trading volumes with illiquidity, unaware that market makers continuously provide liquidity for ETFs.

According to Tradeview Research director of investment advice Nurazlin A Samad, low trading activity in ETFs in Malaysia diminishes their appeal to investors who prioritise liquidity. Many local ETFs face low trading volumes, which pose challenges for investors attempting to execute large orders without influencing market prices. The limited number of market participants to take the opposite side of trades often leads to wider bid-ask spreads and greater slippage.

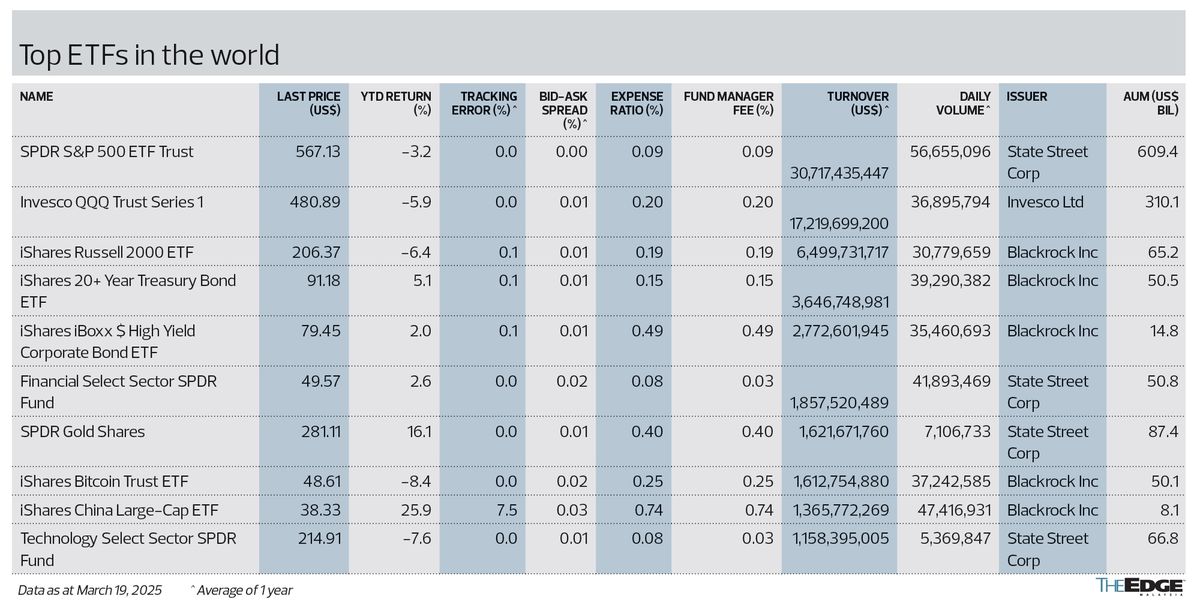

This contrasts sharply with the US ETF market, which is highly liquid, boasting substantial trading volumes and tight bid-ask spreads.

For example, the SPDR S&P 500 ETF Trust (SPY), launched in 1993 to track the S&P 500 index, was the first ETF listed in the US. Today, it stands as the most traded and liquid ETF globally, with an average daily turnover exceeding US$30 billion (RM133 billion). In stark contrast, the FBM KLCI ETF in Malaysia reports a daily turnover of just RM32,000. The significant trading activity in SPY ensures a negligible bid-ask spread, while its Malaysian counterpart struggles with nearly 70 basis points of slippage.

While Nurazlin acknowledges that liquidity must start somewhere, she highlights the limited attention from major buyers of shares in the Malaysian market — government-linked investment companies (GLICs). “As key players with direct stakes in numerous stocks, their involvement is crucial. Without their participation, it becomes even more challenging to expect other local investors to step in,” she says.

Another factor is the structure of Malaysia’s stock market. Unlike the US, Malaysia is a relatively low-beta market rather than an alpha-driven one, lacking the high-growth and high-volatility traits that appeal to aggressive traders. Additionally, the smaller size and less diversified nature of Malaysia’s stock market reduces the effectiveness of ETFs in providing broad market exposure. These limitations discourage foreign investors from engaging in passive investments like ETFs, further restricting market liquidity and fund inflows.

Passive investment is a long-term investment strategy that aims to maximise returns by minimising buying and selling activity. Instead of actively selecting individual stocks or frequently adjusting portfolios, passive investors typically seek to mirror the performance of a broad market index.

UOB Kay Hian head of strategy Vincent Khoo observes that many retail investors in Malaysia already favour direct investment in US equities or US ETFs over domestic equities. This preference is driven by the higher prospective returns and superior trading liquidity offered by US markets.

The recent introduction of online trading platforms like Moomoo Securities and Webull Malaysia, known for their low commission fees, has lowered the barriers to trading foreign stocks and ETFs. The option to trade fractional shares of US stocks and ETFs has further captivated Malaysian retail investors, drawing attention away from Bursa-listed ETFs.

Moomoo’s parent company, Futu Holdings Ltd, is a Hong Kong-based firm listed on Nasdaq. Webull, with Chinese ties, was founded by Wang Anquan, a Chinese entrepreneur and former Alibaba Group employee. The company is currently seeking a Nasdaq listing through a special-purpose acquisition company (SPAC).

In addition to liquidity issues, Nurazlin highlights that some Malaysian ETFs suffer from high tracking errors, which hinder their ability to accurately replicate their benchmarks. Their expense ratios — fees charged to investors to cover operating costs such as management fees, administrative expenses and legal costs — are also less competitive compared to those of their US counterparts.

For example, several Bursa-listed ETFs have tracking errors exceeding 5%, a rarity among US-listed ETFs. Additionally, some local ETFs impose annual management fees exceeding 0.5%, while US ETFs often maintain expense ratios below 0.2%.

The limited selection of ETFs in Malaysia further diminishes their appeal to investors. There are few sector-specific or thematic options, in contrast to the US, where the ETF market features a wide range of themes, from artificial intelligence to clean energy.

In the US, ETFs provide fund managers with broad market exposure through a single trade. For example, an S&P 500 ETF grants access to the top 500 US companies, reducing the risks associated with individual stock selection. In addition, ETFs are also widely used as a hedge against market downturns. Inverse or volatility-based ETFs, for instance, can help mitigate risks during periods of declining market conditions.

It is common for fund managers to include ETFs when constructing their investment portfolios. For example, Ray Dalio’s Bridgewater Associates holds about 22.12% of its portfolio in SPY, while Joel Greenblatt’s Gotham Asset Management allocates around 13.26% to SPY.

Meanwhile, Warren Buffett’s Berkshire Hathaway, which previously held SPY and Vanguard S&P 500 ETF (VOO) in its portfolio, has since sold its entire position in the two market-tracking ETFs.

Back home, domestic institutional investors have been slow to adopt ETFs due to regulatory constraints, investment mandates and a preference for actively managed strategies.

Nurazlin points out that many Bursa-listed ETFs have low AUM, making them unattractive to institutional investors who require scale. Additionally, fund managers often view ETFs as a niche product rather than a core component of portfolio construction.

Apart from the ABF Malaysia Bond ETF, which boasts an AUM of about RM1.8 billion, other Bursa-listed ETFs have AUMs below RM160 million, with some even under RM10 million. This lack of scale poses challenges for institutional investors seeking to navigate these funds. In contrast, US ETFs operate on a much larger scale, with assets reaching hundreds of billions of dollars.

In addition, Nurazlin says the US ETF market benefits from structures that are highly tax-efficient and easy to trade. In contrast, Malaysia’s tax environment and market mechanics lack these advantages. “Supportive incentives in US tax laws and regulations make ETFs an appealing option, particularly because of tax deferral benefits,” she adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- TSMC could face US$1b fine or more from US probe — Reuters

- Massive US tariffs likely to neutralise ringgit's weakness as export aid, say economists

- Musk calls Navarro a ‘moron’ as Trump tariff spat gets messy

- AEON Credit, Matrix Concepts, Fajarbaru, S P Setia, Yong Tai, Taghill, LSH, KNM, Northern Solar, PetGas, Panasonic Malaysia, Subur Tiasa

- Asian stocks drop as Trump’s tariff deadline nears

- SumiSaujana slumps on ACE Market, on course to be worst IPO debut

- Malaysian stocks broadly lower as Asian investors brace for Trump tariffs

- US tariffs, China slowdown cloud developing Asia's growth outlook, says ADB

- Malaysia discusses new initiatives with EU- and US-Asean business councils to boost trade, investments

- PN announces Tapah chairman Abd Muhaimin Malek as Ayer Kuning by-election candidate