The Jakarta skyline: Since 4Q2024, emerging markets have been experiencing a continuous outflow of foreign funds. (Photo by 123RF.Com)

This article first appeared in Capital, The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

GLOBAL financial markets have not been in a good shape since the start of the year. And for more than five months now, foreigners have been net sellers of equities on Asian emerging markets. Last week, a sudden sharp fall in Indonesian stocks raised the alarm about the faltering economic outlook for this region.

Analysts believe the pullout of foreign funds from the region’s markets may continue for some time, although low foreign shareholdings in Malaysian equities could absorb some of the impact.

According to Malacca Securities head of research Loui Low Ley Yee, “foreign funds have more to sell in Thailand and Indonesia” as their foreign shareholdings were higher at between 30% and 40% compared with about 20% for Malaysia prior to the market sell-off.

“The ongoing full-blown effect of the trade war is not fully felt yet. I think there will be further downside risks to the regional markets. Perhaps in the second quarter, we can see light at the end of the tunnel,” he tells The Edge, adding that Malaysian stocks are supported by healthy economic activity with manageable inflationary pressures.

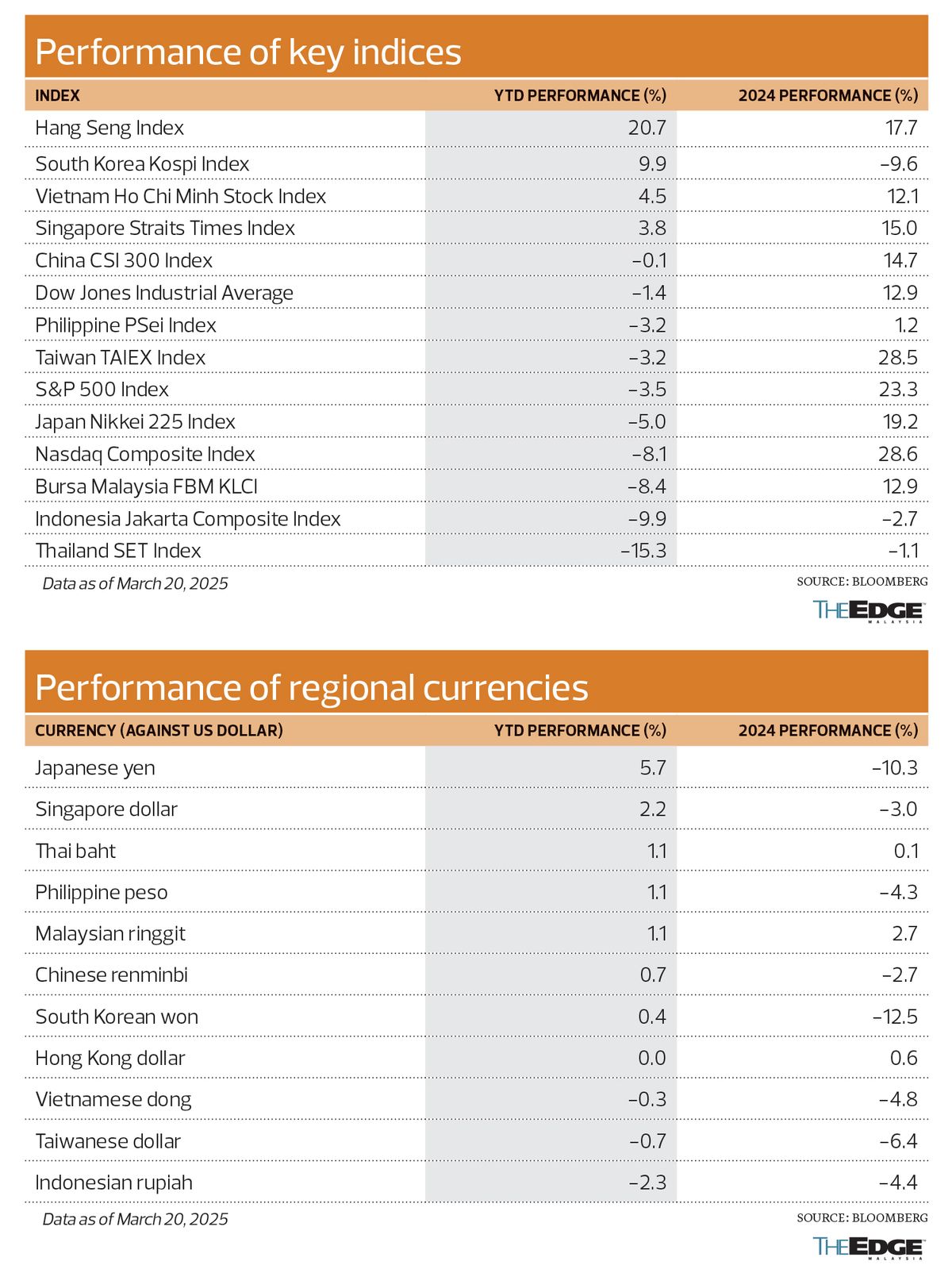

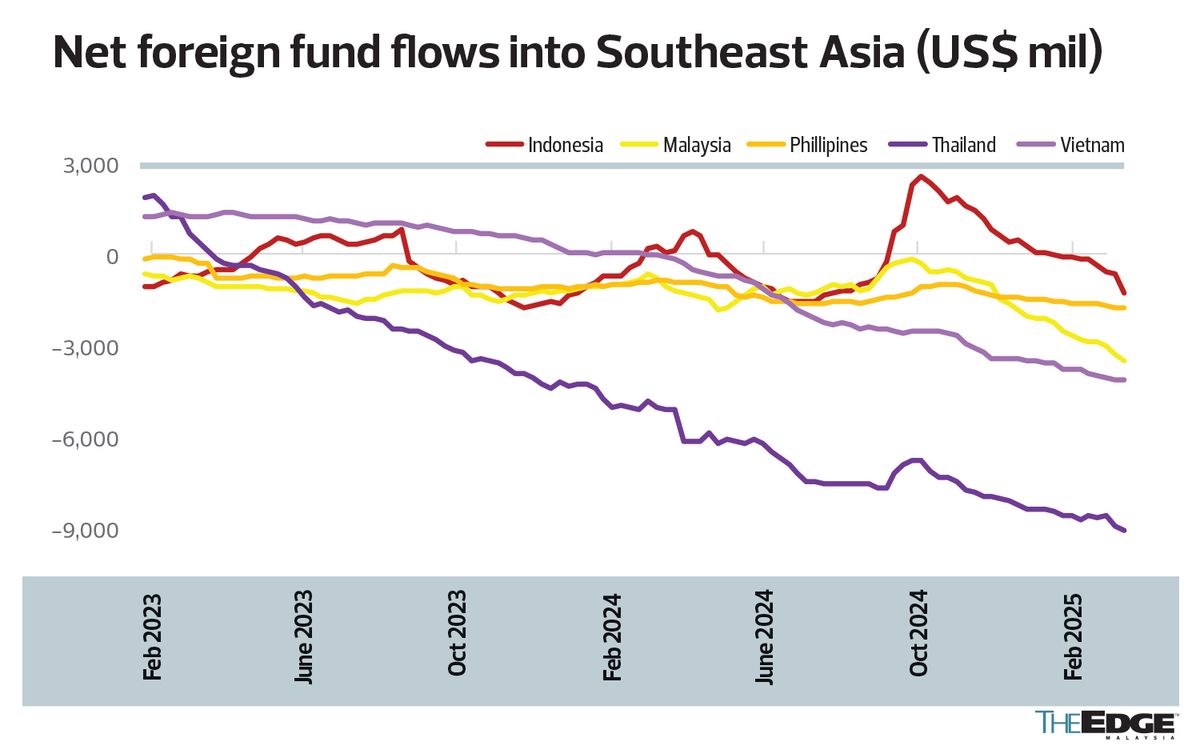

Since the last quarter of 2024, emerging markets have been experiencing a continuous outflow of foreign funds. Foreigners net-sold US$3.65 billion (RM16.1 billion) worth of Indonesian equities during this period.

Malaysia, Thailand and Vietnam have also suffered a net foreign fund outflow worth US$3.43 billion, US$2.45 billion and US$1.68 billion respectively. Foreign funds have been net sellers of Malaysian equities for the past 21 weeks.

MIDF Research head Imran Yassin Md Yusof says, “I think there’s a lot of uncertainty at the moment for the foreigners to reverse back. It’s so hard to see a clear picture of the direction of the global economy, especially with regard to the impact of tariffs, which have caused a lot of confusion.”

When the valuations of local equities become more appealing, he says foreign funds may start coming back to the emerging markets.

“Of course, there might be some rotational play because the European and North Asian markets have performed so well,” he adds.

Acknowledging that market sentiment could be affected in the near term, Imran stresses that prospects for this region are pretty much the same and will continue to be driven by healthy economic conditions.

“When we boil down to earnings and valuations, there shouldn’t be any major impact,” Imran opines.

Similarly, Kenanga Research does not see a material contagion risk from the Indonesian market sell-off following the downgrading of its stock market rating by two global investment banks arising from the fiscal risk and a slowdown in the domestic cyclical sector.

“This comes amid Indonesia’s policies and initiatives being assessed for impact by investors. These include a free nutritious meal programme, efficacy of the investment management agency BP Danantara as a planned superholding agency and a social housing programme (with central bank support via bond purchase).

“Thus, it appears to us that an Indonesia-specific risk that renders material contagion to the FBM KLCI is unlikely, although on a year-to-date (YTD) basis, according to Bloomberg data (US dollar terms), foreign net outflow for Malaysia of US$1.7 billion is only slightly behind that of Indonesia,” the research house explains.

The strategic policies resulted in Goldman Sachs raising concerns about Indonesia’s weaker domestic economy, thus revising downwards its stock rating to “market weight” from “overweight”, alongside the downgrading of its 10-year to 20-year government bonds to “neutral” on the back of rising fiscal risks.

Last month, Morgan Stanley downgraded Indonesia’s MSCI rating from “equal weight” to “underweight”, citing a downtrend trend in the country’s return on equity on the back of the slowdown in the domestic cyclical sector.

Last year, Indonesia’s economy expanded by 5.03% — its slowest pace in three years and far behind new president Prabowo Subianto’s target of 8%. Weak global demand and disruptions due to the US tariffs prompted Bank Indonesia to cut its 2025 growth forecast to between 4.7% and 5.5% from 4.8%-5.6% previously.

YTD, Indonesia’s Jakarta Composite Index has slipped 9.9% with the stock market being one of the worst-performing in the region. Compared to its peak hit last September, the index is down 20%.

The heavy selling pressure on Indonesian stocks has also been partly attributed to the 30% drop in its tax receipts, as well as the nearly 20% decline in total revenue in the first two months of the year. DBS Research says in a note released last week that Indonesia’s 2025 fiscal deficit of 2.5% of gross domestic product (GDP) might need to be revised higher by 30 to 40 basis points if the weak revenue trend persists.

It was also reported that rumours about the resignation of Indonesian Finance Minister Sri Mulyani Indrawati contributed to declining investor confidence in the stock market, given that she is a highly respected technocrat. Nonetheless, she was quick to dispel the speculation, saying that she will stay on.

Apart from Indonesia, Thailand is another battered-down market, with its benchmark SET Index declining 15.3% since the start of the year to trade at the lowest level since the Covid-19 pandemic.

The Thai economy expanded 2.5% in 2024, but lagged regional peers due to high household debt and borrowing costs, as well as sluggish demand from China, which is a key tourism market for the country. The growth forecast for this year is unchanged at a range of 2.3% to 3.3%.

Recently, the Thai government announced a US$4.4 billion cash handout plan to stimulate the country’s growth while ramping up infrastructure investments and proposing to legalise casinos.

At home, the FBM KLCI, which is trading at an undemanding valuation of about 14 times price-earnings ratio, is down 8.4% YTD. Malaysia wrapped up 2024 with a decent economic growth of 5.1%, which was at the higher end of official projections of between 4.8% and 5.3%.

Malacca Securities’ Low says while Malaysian firms will not be spared should the US economy experience a slowdown, a potential China recovery could act as a stabilising factor, especially for companies that trade with the Chinese.

As Malaysia is part of the global supply chain, MIDF’s Imran says it remains to be seen what the impact would be as a result of the ongoing trade war. However, he believes Malaysian corporate earnings are expected to remain robust this year. “It will take some time for tariffs to have an impact in terms of demand. So from what we have seen in the fourth-quarter earnings, corporate earnings expectations remain intact for this year and no change [in our forecasts] at the moment.”

In view of the heightened volatility, Imran maintains a defensive play on Malaysian equities this year.

“Since December last year, we have been recommending a defensive strategy for 2025. We make no change to our view. We continue to recommend banking stocks for strong dividend yields of between 4% and 7%. Our economic fundamentals are still quite solid, and the banking sector is very much tied to the economy, with Malayan Banking Bhd (KL:MAYBANK) being our top pick,” he adds.

Imran also favours the real estate investment trust (REIT) sector, which offers dividend yields of 4% to 6%, as well as the utilities sector. “Defensive names seem to be outperforming the growth names.”

Low sees buying opportunities in oversold sectors such as energy and technology with construction seeing some recovery going forward.

“I think we just have to hang on to the heavyweights with stable order books. Investors are pricing in lower price-earnings multiples for companies related to data centres, but earnings are actually quite intact, so we just have to rely on stable earnings. Once the price-earnings multiples are revised higher, then perhaps the share prices will also rally,” he adds.

Kenanga cautions that names more exposed to the domestic Indonesian economy that may bear watching for knee-jerk reactions include CIMB Group Holdings Bhd (KL:CIMB), which derives 25% of its profit before tax (PBT) and 15% of loans from its Indonesian operation.

To a lesser extent, Indonesian business accounts for 3% and 5% of Maybank’s PBT and loans.

For Axiata Group Bhd (KL:AXIATA), its Indonesian unit PT XL Axiata Tbk forms 19% of the group’s enterprise value.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Malaysia won’t retaliate, will negotiate with US on tariffs — Miti

- Glovemakers rebound as investors see competitive advantages

- Thailand’s richest man picks bad day to debut flagship firm

- Malaysia's semicon firms brace for future US action after dodging tariffs

- Vietnam in the eye of US tariff storm; Asian markets tumble

- Opec+ unexpectedly speeds up oil output hikes, oil drops

- Trump gives China’s Xi a chance to win over world hit by tariffs

- Malaysian manufacturers sound alarm over US tariff, call for strategic govt action

- ICC prosecutor Karim Khan accused of retaliation for sexual misconduct allegation — Reuters

- Mayu Global executive director Tan Kim Hee detained by police