Leonard Ariff: As we introduce new products to our portfolio, we will also try to rationalise older and underperforming products, that is, potentially stop marketing some of the older products. Refreshing our portfolio is a priority for us. (Photo by Suhaimi Yusuf/The Edge)

This article first appeared in The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

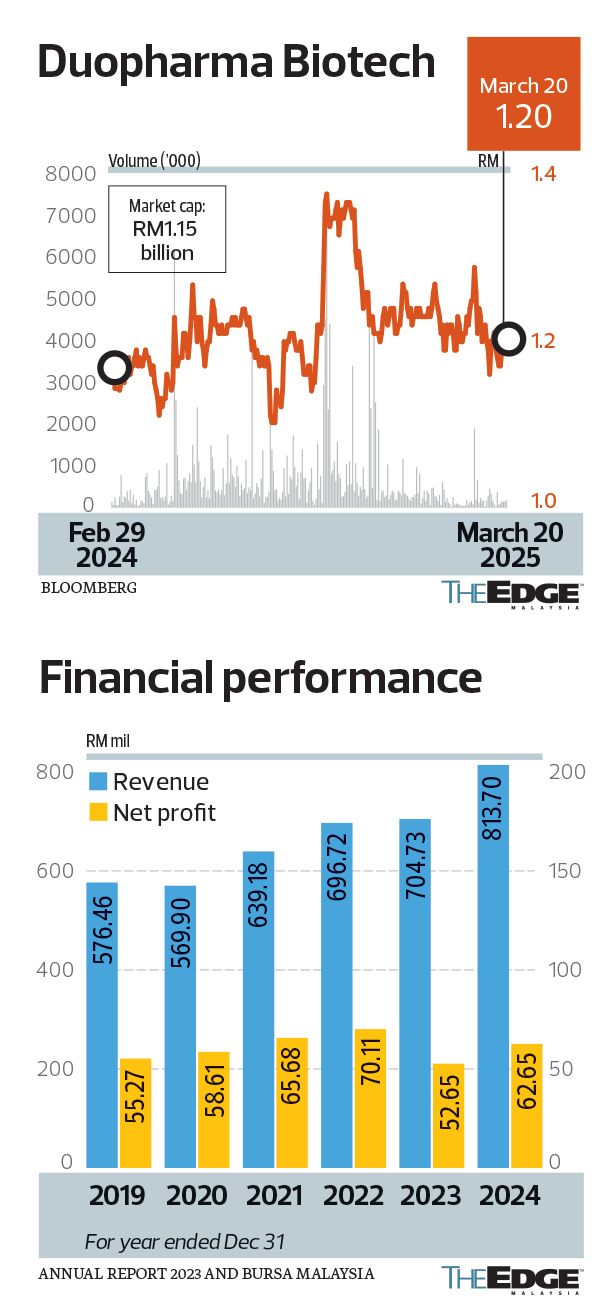

A focus on growing revenue has paid off for Duopharma Biotech Bhd (KL:DPHARMA), which reported its highest annual revenue on record last year.

After rising costs and softer demand sent its net profit down 25% in 2023, the country’s largest generic drug manufacturer by market share is back on a growth path. It posted a net profit of RM62.65 million in the financial year ended Dec 31, 2024 (FY2024), up 19% from RM52.65 million in the previous year. The profit boost came amid a 15% year-on-year (y-o-y) rise in revenue to RM813.7 million in FY2024, a record performance.

According to its group managing director (MD) Leonard Ariff Abdul Shatar, the profit rebound was expected and the group is gearing up for another good year in FY2025.

“We had a ‘perfect storm’ thrown at us and we rode it out,” he says, describing the fall in earnings in FY2023 as a “blip”. A variety of factors — from increased borrowing costs to a weakening ringgit, surging electricity prices, an increase in prices of raw materials for essential drugs called active pharmaceutical ingredients (APIs) and weaker-than-expected sales from its consumer healthcare division — had created the “perfect storm” in FY2023.

While these headwinds continued into FY2024, Duopharma Biotech was able to cushion that pressure through a shift in focus to the public sector to drive revenue growth. This was driven by a new approved products purchase list (APPL) contract secured with the government in the second quarter of 2024, which gives it earnings visibility until end-2026. As a result, the group saw revenue contribution from the public sector rise to 50% in FY2024, compared with 44% in FY2023.

It also benefited from the ringgit’s strengthening against the US dollar in the second half of 2024. “Today, the ringgit has more or less stabilised to reach a level of 4.4 to 4.45 against the greenback,” Leonard Ariff says. This is good news for Malaysia’s pharmaceutical industry, which remains heavily dependent on imported raw materials that are predominantly US dollar-denominated.

He notes that the prices of APIs have also declined to pre-Covid-19 pandemic levels last year, boosting the margins of pharmaceutical companies like Duopharma Biotech. In a March 17 report, TA Securities said API prices have dropped by at least 10% y-o-y.

While Leonard Ariff does not think API prices will fall any further,there is a time lag effect before Duopharma Biotech is able to benefit from the lower raw material prices as it holds between three and six months’ worth of stock.

“Even though API prices have started falling since last year, we expect the impact on our financials will be more pronounced in 2025 relative to 2024 due to the lag effect, given that it takes time to exhaust the old raw material inventory,” he tells The Edge in an interview.

Leonard Ariff, who turns 61 this year, says he will not pursue an extension of his term once it concludes at year end.

He says that in September last year, Duopharma Biotech’s board of directors had extended his tenure as group MD for another year “to see through a succession plan that we had planned in the last five years”. The group is also looking for a successor to chief financial officer Chek Wu Kong, who will retire from the group at the end of January next year.

“I have been in this role (group MD) of a government-linked company for 18 years. I think it is time for fresh leadership. We have already laid down the groundwork for the next 10 years as pharmaceuticals is not a short-term business,” Leonard Ariff says.

Permodalan Nasional Bhd is the largest shareholder in Duopharma Biotech, owning 44.1% equity interest, followed by the Employees Provident Fund Board with an 8.74% stake.

Upbeat about FY2025

Leonard Ariff provides an upbeat outlook for 2025 due to a combination of factors, including higher revenue contribution from the public sector. This is on the back of a first full-year earnings contribution from the renewal of the government’s APPL contract, compared with just three quarters of contribution in FY2024.

“This leads us to be reasonably optimistic that revenue will be maintained, if not improved. The [higher sales from the public sector] is sufficient to manage some of the cost pressures that we are under at the moment,” he says, adding that the public sector’s revenue contribution is likely to exceed 50% this year.

As a result, the private sector’s revenue contribution, including the export segment, may shrink. He points out that this is not because the company is selling fewer products to the private sector but rather that it is growing that sector “at a slower pace” than the public sector.

Despite the increasing dominance of the public sector in the group’s revenue, there is no fear of a concentration risk, says Leonard Ariff.

“The government’s consumption of generic medicines is about 60% of the total market. The public sector accounts for half of our portfolio. So you can argue that we remain under-represented in the government sector. We’re quite comfortable with the current 50% revenue contribution from that sector,” he explains.

However, the group aims to reduce its reliance on the domestic market and is actively expanding its market presence regionally, especially in Indonesia and the Philippines. At present, the export business contributes 7% to Duopharma Biotech’s overall revenue. “We export to about 30 countries, mostly to Asean,” Leonard Ariff says.

Raising the share of the export market also helps create a natural hedge to the US dollar as almost 70% of the group’s raw material costs are denominated in the greenback.

The group is on the lookout for inorganic growth opportunities to expand its export business. This could include the acquisition of peers or health-related companies.

“Our ethical classic (prescription pharmaceutical) products are sold to general practitioners and pharmacies, while the ethical speciality business looks at therapeutic groups such as oncology and renal. We don’t mind looking at acquisitions that fall within these groups. For instance, they could be medical device makers in the oncology area or software companies in the renal area, which will enable us to offer a total solution to our customers,” he says.

There are certain criteria that must be met for any acquisition to happen. For one, the target entity must be able to boost Duopharma Biotech’s top and bottom line growth, says Leonard Ariff.

“We are not prepared to buy a loss-making [entity] because I don’t think our balance sheet can take that. Last year, we looked at 22 potential candidates, both local and regional, and only two went to the stage where we did more detailed analysis,” he reveals.

The group had to abandon its pursuit of the two companies because one was overpriced and the other was only prepared to sell a minority stake, he says. “We will only take a minority stake in a company if it is for technology access but, for purposes of a merger and acquisition, we must have a controlling interest in the company to be able to consolidate its financial results.”

Duopharma Biotech’s cash and equivalents stood at RM264.55 million at end-2024, while borrowings totalled RM512.52 million, leading to a net debt of RM247.97 million. It has a net gearing ratio of 0.35 times.

Leonard Ariff’s upbeat view of the group’s growth prospects in FY2025 also stems from the bottoming out of the slide in its consumer healthcare segment last year.

“During the pandemic, sales from our consumer healthcare segment shot through the roof due to the high demand for our popular vitamin C brands, Champs and Flavettes. This resulted in us building up our vitamin C stock. Then the country shifted to the endemic phase, which caused the demand for vitamin C to drop substantially and we suddenly ended up with a lot of stock,” he recalls.

Nevertheless, 2025 is set to be a year of normalisation for the consumer healthcare segment, with the group having completed a destocking of its Vitamin C last year, he says.

“This year would be a much better year for the consumer healthcare segment in the sense that my stock balance is now well-balanced against my sales and thus there will be less price discounting. Therefore, we’re anticipating both margin and volume growth in consumer healthcare. In fact, we’re looking at price increases for some of our consumer healthcare products.”

SKU rationalisation

Duopharma Biotech plans to unveil five to six new products this year, adding to its product portfolio of 250 stock-keeping units (SKUs).

“The idea is, as we introduce new products to our portfolio, we will also try to rationalise older and underperforming products, that is, potentially stop marketing some of the older products. Refreshing our portfolio is a priority for us. Having said that, we are also cognisant of the fact that the Ministry of Health (MoH) wants Malaysia to have some level of self-sufficiency. So, while some products may be old, it may be products that MoH still wants to use on a continuous basis. As such, we won’t be retiring those products,” says Leonard Ariff.

He adds: “There are some products that MoH and the private sector are not consuming very much and [these] don’t have a major impact on the group, but they consume manufacturing capacity. We will decommission these products. We have been undertaking this [exercise] over the last seven years. So every time you hear about Duopharma Biotech launching five or six products, chances are we have also rationalised five or six products from our portfolio.”

The pandemic has taught the group to diversify its consumer healthcare product portfolio to ensure sustained growth. For starters, it has increased its advertising and promotional spending on its analgesic (pain reliever) brand Uphamol.

“However, we don’t think these two products (vitamin C and analgesic) are sufficient. We need more product ranges. We are also looking at producing energy bars and functional gels as we notice that young people are moving towards healthier lifestyles and food,” Leonard Ariff says.

Meanwhile, he says Duopharma Biotech has no plan to roll out a dividend policy but has consistently paid out a third of its net profit as dividends. The group declared a total dividend of 3 sen per share, equivalent to RM28.86 million, in FY2024 — an increase of 30.4% compared with RM22.13 million in FY2023.

“We don’t have a dividend payout policy but we have a practice of paying out a minimum of 30% of our net profit [as dividends]. That’s because in pharmaceuticals, we have requirements for large capital expenditures every so often. So it’s very difficult to have a fixed policy.”

Amid market uncertainties, analysts see bright spots in pharmaceutical stocks

With shifting trade policies in the US, tariff concerns and geopolitical tensions continuing to weigh on markets, analysts are favouring defensive sectors such as healthcare for their resilience in this uncertain environment.

The uncertainties have taken a toll on the stock market’s benchmark FBM KLCI, which was down 8% this year as at its close of 1,504.16 points last Thursday (March 20). PublicInvest Research believes there could be more downside to the KLCI in the short term. It has revised its year-end 2025 KLCI target down to 1,630 points (based on 13.5 times the 2026 forward price-to-earnings ratio [PER]) from 1,700 points (based on 14.5 times the 2026 forward PER), in view of the uncertainties globally that could affect investor appetite and stock valuations.

Nevertheless, Duopharma Biotech Bhd (KL:DPHARMA) group managing director Leonard Ariff Abdul Shatar is upbeat about the local pharmaceutical industry’s prospects, having had a positive start to the year.

He observes a sharp pickup in flu-related medication in the first quarter of 2025 because of a rise in influenza cases. “Whether it is a seasonal or a permanent change in demand remains to be seen,” he tells The Edge in an interview.

He notes that one thing that has remained constant despite the multiple changes of government in the past few years is the rise in the country’s annual healthcare allocation.

“This indicates a recognition by the government in terms of funding better healthcare for the public. However, the issue falls back on affordability in the longer term. The problem with our public healthcare system is that it is a one-size-fits-all. You can be the richest man or the poorest man in the country; both go to the government hospitals and clinics and pay the same RM1 bill (for outpatient care). But I believe some form of user-pay model should come into the picture in the longer term,” he says.

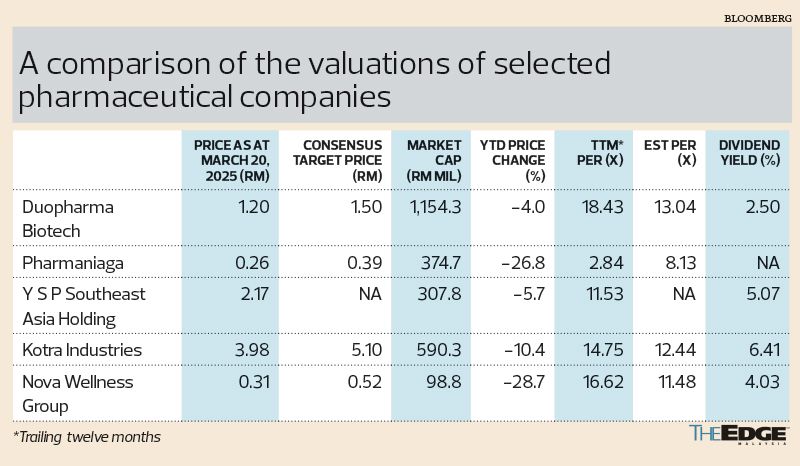

Kenanga Research has an “overweight” rating on the healthcare sector, with an “outperform” call on Kotra Industries Bhd (KL:KOTRA) and a target price of RM5.10, which indicates a potential upside of 28% from last Thursday’s closing price of RM3.98.

Kenanga Research says Kotra’s 1HFY2025 margin shows marked improvement on sales of higher-margin products although its earnings missed the research firm’s expectation. Kotra’s net profit fell 18% to RM20.7 million for the six months ended Dec 31, 2024 (1HFY2025) from RM25.28 million a year earlier, on higher advertising and promotion expenses and foreign exchange loss. However, its 2QFY2025 earnings managed to grow 13% quarter on quarter to RM10.96 million.

“We remain upbeat on Kotra backed by recovering consumer spending, drawing encouragement from sales momentum,” Kenanga Research says in a March 14 report.

It adds: “Independent market researcher The Statista Consumer Market Outlook projects the over-the-counter (OTC) pharmaceutical market in Malaysia to grow at a compound annual growth rate of 6% to an estimated US$715 million (RM3.2 billion) by 2027 as consumers take a more proactive stance towards their health and well-being (including taking health supplements regularly), especially in the aftermath of the Covid-19 pandemic.”

Kenanga Research goes on to say that the trend augurs well for Kotra, which manufactures and sells OTC supplements and nutritional and pharmaceutical products under brands such as Appeton, Axcel and Vaxcel.

Additionally, the research firm likes Kotra for its integrated business model encompassing the entire spectrum of the pharmaceutical value chain from research and development (R&D) and product conceptualisation to manufacturing and sales; and the superior margins of its original brand manufacturing business model versus low-margin contract manufacturing.

Kenanga Research also likes health and nutrition company Nova Wellness Group Bhd (KL:NOVA) for its business model, which encompasses the entire spectrum of the value chain, from product conceptualisation starting with R&D to manufacturing. It has a “market perform” call on Nova, with a target price of 41 sen. The stock closed at 31 sen on Thursday.

RHB Research has an “overweight” stance on the healthcare facilities and services sector.

It is of the view that the pharmaceutical company under its coverage — Duopharma Biotech — should continue to see robust sales pick-up in 1H2025, underpinned by a sustained sales outlook from the ethical speciality segment, higher government budget allocation for the Ministry of Health (MoH) and the extension of the approved products purchase list (APPL).

Duopharma Biotech’s margin should improve sequentially, aided by the normalisation of the active pharmaceutical ingredient (API) prices in the latter part of 2024, it says in a March 13 report.

Today, Duopharma Biotech leads the generic segment of the pharmaceutical industry in Malaysia with a market share of more than 20%. However, it has a low 3% to 5% share of the total pharmaceutical market.

“The group is in a good stead at the moment,” Leonard Ariff says, noting that Duopharma Biotech reported a 19% rise in net profit to RM62.65 million in the financial year ended Dec 31, 2024 (FY2024) compared with RM52.65 million in the previous year.

“The major initiatives that we have implemented over the last 36 months [include] us entering Bursa Malaysia’s FTSE4-Good Index [in 2021]. We have been putting quite a lot of effort into sustainability. Sustainability of the business is important to me. I would like to think that the business is on a strong footing and the required investments and projects are in place to take us to the next decade, although it should be led by somebody new,” he adds. Turning 61 this year, he says he will not pursue an extension of his term when it concludes at the end of the year.

RHB Research has upgraded Duopharma Biotech’s stock to “buy” from “neutral” after accounting for the government’s higher budget allocations for MoH. It notes that finalisation of a human insulin supply contract by April should provide better earnings visibility ahead. The research firm put a target price of RM1.45 on the stock, 21% above its closing price of RM1.20 on Thursday. Duopharma Biotech’s stock is down 4% year to date, in line with broader market moves.

“Moving forward, Duopharma Biotech’s growth should be underpinned by the recent additional letter of award by MoH for the supply of pharmaceutical products under the APPL contract (bringing its product range to 96 from 86 earlier) and the potential renewal of a human insulin supply contract with MoH (expected to be concluded by 1Q2024) as well as the higher budget allocation to the MoH, which should boost its public sales,” RHB Research writes in a Feb 20 report.

It raised its 2025 and 2026 earnings projections by 7% and 4% respectively, taking into account lower raw material prices. “We expect the net margin to be sustained within 10% in 2025, from 8% in 2024.”

TA Securities, meanwhile, is confident FY2025 will be a year of record-breaking profit for Duopharma Biotech, with earnings anticipated to increase by 41.2% to RM88.4 million.

In a March 17 report, TA Securities says this robust performance is expected to be driven by higher sales of 9.8%; lower API, which has dropped by at least 10% year on year; and cost efficiencies.

“We expect Duopharma Biotech to begin realising the benefits of lower API prices from 1Q2025 onwards as the old raw material inventory depletes. Our sensitivity analysis suggests that [the group] could save approximately RM14 million for every 5% change in API prices,” it says.

It reiterated a “buy” call on the generic drug manufacturer and maintained its target price of RM1.62 per share, based on 16 times forward 2026 earnings per share and a 3% ESG premium.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Berkshire dismisses 'false' reports on Buffett comments after Trump shares video

- Malaysian Highway Authority: 20km traffic jam on KL-Karak Highway as Raya travellers return

- Trump’s TikTok plan upended by Chinese objections over tariffs — Bloomberg

- China’s rare earths curbs put multiple US industries at risk

- LTAT moving forward despite challenges

- Philippines alarmed over China arrest of alleged Filipino spies

- Foxconn reports record 1Q revenue, says it must closely watch global politics

- Putra Heights disaster: King visits victims, provides assistance

- FMM flags significant challenge for 200 businesses amid 20-day gas disruption after Putra Heights fire

- Melaka to host Visit Malaysia 2026 launching ceremony, says Anwar