This article first appeared in The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

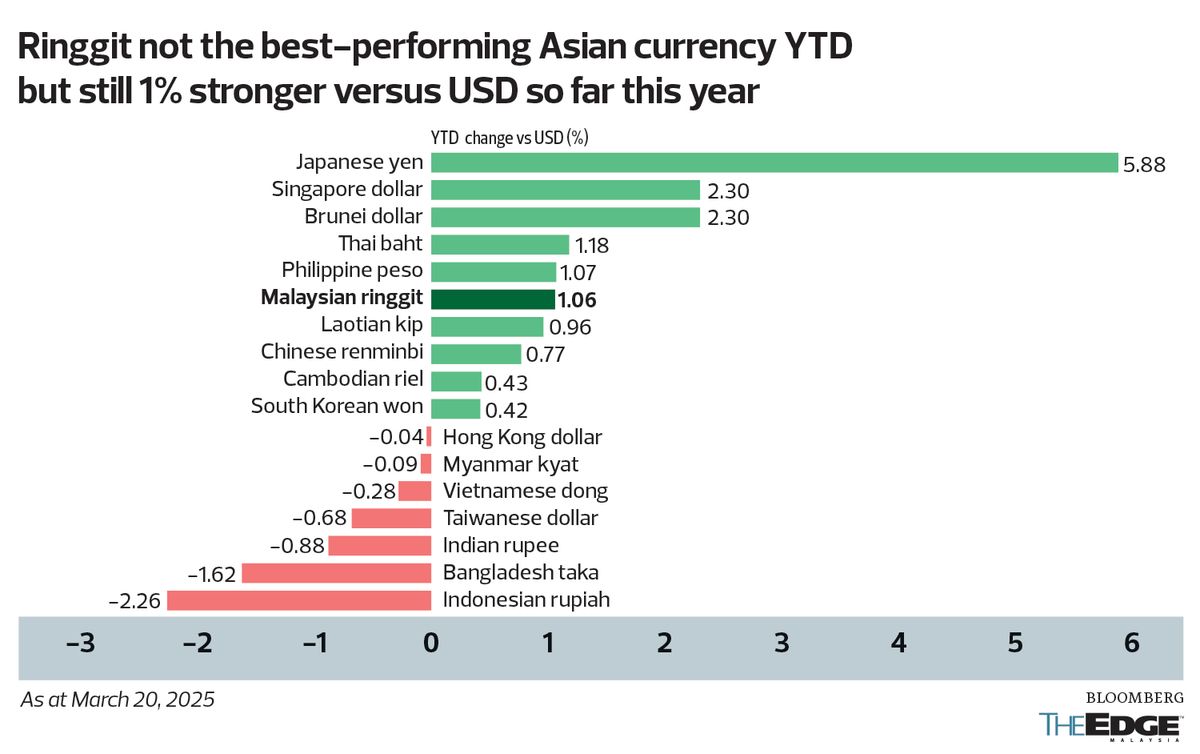

THE ringgit’s outperformance among Asian currencies last year may be harder to repeat this year, with some currency traders weighing the possibility of Bank Negara Malaysia trimming interest rates to bolster growth dragged lower by US-led retaliatory tariffs. That is despite a consensus still firmly for Bank Negara to keep its overnight policy rate (OPR) at 3% throughout 2025.

“Contributing to the relative weakness of the ringgit are traders pricing in a rate cut of 25 basis points (bps) by Bank Negara in the next 12 months and larger foreign portfolio outflows, which have widened to RM3.3 billion in February from RM2 billion in January. In the near term, external uncertainties, particularly that of [US President Donald] Trump’s tariff policy, will continue to weigh on the ringgit and other Asian currencies. Despite resilient domestic fundamentals, the ringgit’s close correlation to the renminbi may accentuate the spillover effect if Trump escalates trade tariffs against China,” says an economist with UOB Bank Singapore.

UOB economists see the ringgit — which still had gains against the greenback year to date, as it closed at 4.4243 against the US dollar on March 20 — weakening to 4.55 in the second quarter of 2025 (2Q2025) and 4.65 in 3Q2025, before retracing ground to 4.55 in 4Q2025 and 4.50 in 1Q2026.

UOB’s ringgit forecast is more bearish compared with the median of 4.5 in 2Q2025, 4.49 in 3Q2025, 4.46 in 4Q2025 and 4.41 in 1Q2026 from Bloomberg’s compilation of 14 contributors.

Nonetheless, UOB’s forecasts are more sanguine compared with Credit Agricole and Maybank Singapore’s expectations of the ringgit sliding to 4.60 versus the greenback by 2Q2025. The most bearish forecast is Capital Economics’ forecast of the ringgit touching 4.70 by year end, Bloomberg data shows at the time of writing. This is still stronger than the 4.7987 that the ringgit had skidded to against the greenback in February 2024.

Those expecting the ringgit to retrace some ground against the US dollar towards the end of the year and early next year may well back more US rate cuts finally materialising after the Federal Open Market Committee (FOMC) paused cuts in January 2025 (having already lowered rates by a full percentage point in late 2024).

Is OPR cut on the table?

Whether ringgit bears are justified may well boil down to the severity of US tariffs and the degree of global retaliation, and if other pressures on the Malaysian economy are severe enough to warrant an OPR cut by Bank Negara.

While acknowledging uncertainties surrounding the US’ reciprocal tariffs that may take effect when unveiled on April 2, most economists do not see Bank Negara trimming the OPR this year.

Only two of the 28 forecasters expect the OPR to be lowered from the current 3%, according to Bloomberg data at the time of writing, with Barclays PLC pencilling in a cut of 25bps to 2.75% by 2Q2025 and Morgan Stanley expecting a reduction of up to 50bps to 2.5% by 3Q2025.

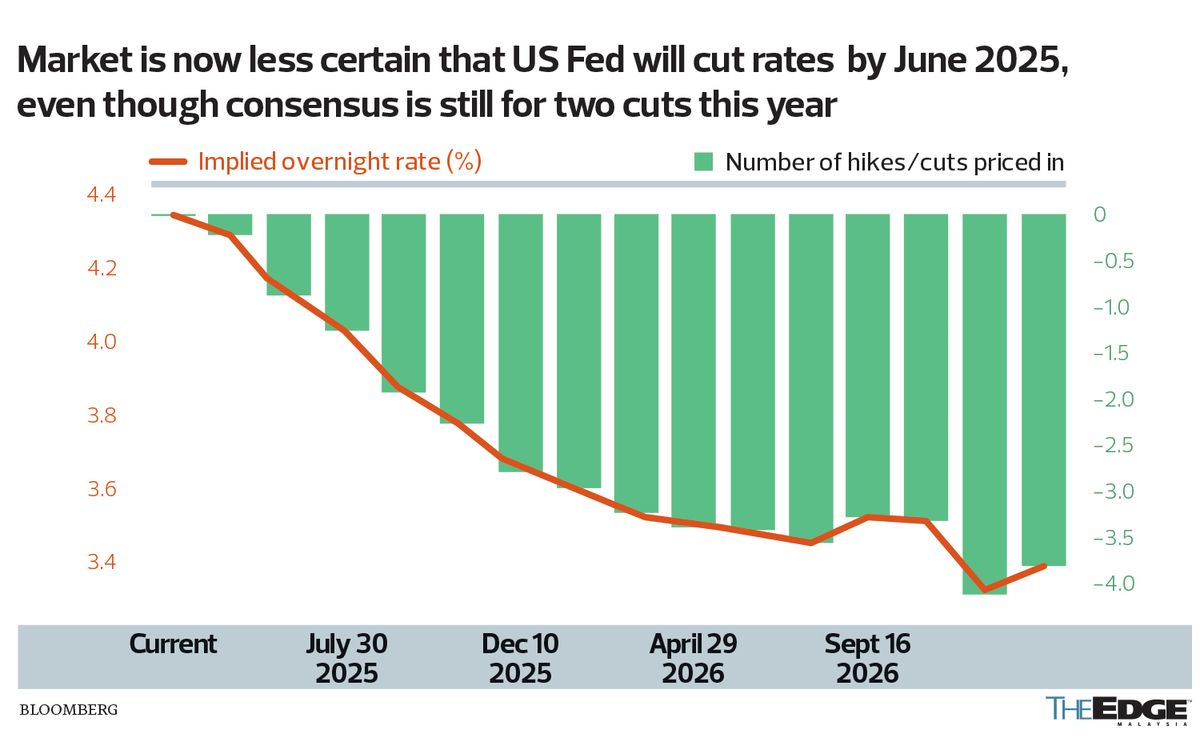

If an OPR rate cut materialises in 2025, there will be no net benefit of narrowing interest rate differentials for the ringgit should the FOMC decide to trim its benchmark federal funds rate (FFR) by quarter percentage points twice from as early as June, from the current 4.25% to the 4.5% range as per the current consensus. That would be a drag on the ringgit against the US dollar.

What if the Fed pauses longer?

There is more. If the latest FOMC “dot plot” is any indication, an OPR rate cut, if it materialises, would be a bigger drag on the ringgit should the US Federal Reserve see no reason from the data it monitors to trim interest rates by June, July or even September.

To be sure, the ringgit might still see some near-term weakness — even if there is no OPR cut — should the FOMC trim rates less than expected this year.

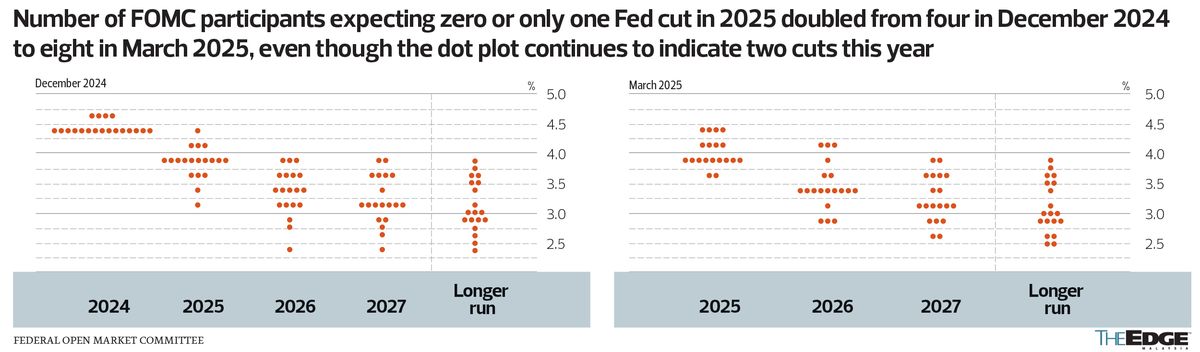

Like the December 2024 FOMC dot plot, the latest dot plot for March 2025 indicates two cuts of 25bps each in 2025 for the FFR to end the year at 3.9%. However, only nine out of 19 FOMC members now expect two cuts this year, down from 10 three months ago. Instead of three, there are now four FOMC participants expecting only one rate cut in 2025 — twice as many as the two expecting three rate cuts this year.

And instead of just one outlier, now four FOMC participants expect no rate cuts in 2025 — despite Trump’s social media post on March 19 that “The Fed would be MUCH better off CUTTING RATES as US tariffs start to transition (ease!) their way into the economy”.

UOB economists are among those forecasting only one Fed rate cut this year, despite the dot plot still indicating two. “While we acknowledge the downside risk to growth has increased, we continue to err on the more cautious side towards inflation risk. The combination of elevated inflation, (potentially) slower growth and ‘high uncertainties’ surrounding tariffs does not make it easy for the Fed to cut rates in 2025.

“Additionally, while the clear majority [of the FOMC participants] (15 of 19) are still looking at further cuts in 2025, the number of cuts (based on individual projections) has been pared back. Therefore, in our view, if asked to give the probability of rate cuts going to zero versus going to three cuts, we think the Fed will err on the side of caution, and [maintain a] wait-and-see approach,” the UOB economists added.

Still cautiously optimistic

Winson Phoon, head of fixed income at Maybank Investment Banking Group in Singapore, also acknowledges a seemingly more hawkish FOMC dot plot in March 2025 versus December 2024, whereby the number of FOMC participants expecting zero or only one Fed rate cut in 2025 has doubled from four to eight. “However, we believe the Fed will cut rates by 50bps in total this year, as the current US monetary policy remains restrictive, economic growth is expected to slow and labour market conditions have softened,” he tells The Edge.

Conditions in the US labour market have indeed cooled from the post-pandemic tightness that saw the unemployment rate reducing to its lowest in more than 50 years of 3.4% in early 2023 to about 4.1% currently — an unemployment rate that was still described by US Federal Reserve chairman Jerome Powell as “low” last Wednesday. Powell also sees tariff-induced inflation as “transitory”.

Phoon says bids on ringgit bonds increased last week, “with buying interest seen across the curve, including long durations”. “MGS yields are down 3bps to 5bps week to date and look set to post their best week in 2025. The supply and demand profiles for both ringgit government and credit bonds remain favourable,” Phoon replies when asked on the ripples from the recent Indonesian market sell-off.

Christopher Wong, FX strategist at OCBC Bank, says “markets are pricing in 68bps of cuts for this year versus 59bps before FOMC’s March 19 decision” and that its base case continues to be cuts of 75bps this year.

“Our projection for USD/MYR is mildly skewed to the upside this year (4.48 end-2025) as we take into consideration the potential risk of tariff implementation, inflation risks (for the US) and a risk that Fed cuts may slow. The broadening of trade war can further undermine sentiments and provide a boost to the broad US dollar. But at the same time, Malaysia’s domestic fundamentals remain sound, supported by robust macroeconomics, investment upcycle, current account surplus, fiscal improvements, FDI (foreign direct investment) inflows and relative domestic stability,” says Wong.

The ringgit, he says, “is likely to strengthen beyond our projection” should stronger-than-expected growth in China and Europe help shore up global growth, if there is a rebound in confidence in Chinese assets riding on a re-rating of Chinese tech stocks, or the US dollar somehow sees an extended decline.

On the flipside, the ringgit may end up weakening should a broadening tariff war weigh on global growth and trade, if the US turns hawkish from worsening liquidity conditions or runaway inflation and should China’s economic recovery momentum falter.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- TSMC could face US$1b fine or more from US probe — Reuters

- Massive US tariffs likely to neutralise ringgit's weakness as export aid, say economists

- Musk calls Navarro a ‘moron’ as Trump tariff spat gets messy

- AEON Credit, Matrix Concepts, Fajarbaru, S P Setia, Yong Tai, Taghill, LSH, KNM, Northern Solar, PetGas, Panasonic Malaysia, Subur Tiasa

- Asian stocks drop as Trump’s tariff deadline nears

- SumiSaujana slumps on ACE Market, on course to be worst IPO debut

- Malaysian stocks broadly lower as Asian investors brace for Trump tariffs

- US tariffs, China slowdown cloud developing Asia's growth outlook, says ADB

- Malaysia discusses new initiatives with EU- and US-Asean business councils to boost trade, investments

- PN announces Tapah chairman Abd Muhaimin Malek as Ayer Kuning by-election candidate