This article first appeared in City & Country, The Edge Malaysia Weekly on March 24, 2025 - March 30, 2025

In the last quarter of 2024, the Klang Valley residential property market saw mixed trends, says Savills Malaysia director of research and consultancy Fong Kean Hwa in presenting The Edge Malaysia | Savills Klang Valley Residential Property Monitor 4Q2024.

“Selangor saw improvements, supported by higher demand and transaction volume, and a decline in unsold inventory. While Kuala Lumpur saw a greater improvement in transaction volume and value than Selangor, the number of its overhang units remained slightly higher than a year ago,” Fong says.

“This is probably due to their distinct development patterns and focus. Kuala Lumpur is dominated by high-rise properties, while landed housing remains the primary focus in Selangor.”

Citing data from the National Property Information Centre (Napic), he notes that total residential property transactions in Kuala Lumpur increased by 5.5% to 18,913 units in 2024 compared to 17,928 units in 2023. Similarly, the total transaction value rose 16.6% y-o-y to RM17.46 billion, from RM14.97 billion.

In Selangor, transaction activity rose from 59,078 units in 2023 to 60,703 in 2024, up 2.8% y-o-y. The total transaction value grew 5% y-o-y to RM33.99 billion, from RM32.35 billion.

The number of overhang units in Kuala Lumpur was 9,081 units as at 4Q2024, relatively stagnant compared to 9,050 units a year ago. “Serviced apartments and SoHo (small office home office) units accounted for the highest number of overhang units at 4,847, comprising 53% of total overhang units as at 4Q2024. Of the 4,847 units, 1,874 units, or 39%, are priced above RM1 million each,” Fong notes.

In Selangor, the number of overhang units fell 11.8% y-o-y from 5,899 units as at 4Q2023 to 5,203 units in 4Q2024. About 60%, or 3,128 units, of the 5,203 units are serviced apartments and SoHos, of which 1,286 units, or 41%, are priced in the range of RM500,000 to RM600,000.

In terms of supply in 2024, 19,643 new units were completed in Kuala Lumpur, including serviced apartments and SoHos. This was 9.9% lower than the 21,811 new units recorded in 2023. Incoming supply shrank, however, to 99,095 units as at 4Q2024, down 8.6% y-o-y from 108,454 units.

“This suggests that Kuala Lumpur’s residential market could expect a substantial impending supply in the next three years,” Fong says.

Selangor also saw an increase in new residential completions, with 32,698 units delivered in 2024, up 8.6% y-o-y from 30,112 units. Incoming supply dropped to 158,326 units as at 4Q2024, down 3.7% y-o-y from 164,384 units.

Market confidence to sustain momentum

Despite the mixed performance, Fong believes favourable economic factors, government initiatives and catalytic developments will sustain market sentiment and momentum across the broader residential property sector in the Klang Valley.

“The continued growth of Malaysia’s economy, charted at 5.1% GDP (gross domestic product) growth in 2024, is driven by strong domestic demand and investment activity. Household spending also remained stable, supported by the favourable labour market and policy measures,” he says.

“Government policies, such as implementing 23 new affordable housing projects under the People’s Housing Programme (PPR) and a RM10 billion Housing Credit Guarantee Scheme, will drive demand for affordable residential properties.

“There is also tax relief on housing loans given to first-time homebuyers, where tax relief of up to RM7,000 for residential homes priced at up to RM500,000 and tax relief of up to RM5,000 for residential homes priced from RM500,000 to RM750,000 will benefit the mid-range residential market in 2025.”

The revision of the Malaysia My Second Home (MM2H) programme in October 2024 continues to boost foreign investment in the property market, Fong says. “It was disclosed that about 782 approvals had been made under the new MM2H guidelines since June 2023. As at end-2024, the total number of MM2H approvals had reached 58,468 since its inception.”

According to Fong, the number of housing loan applicants have continued to increase, supported by the accommodated loan rate. “A total of RM448.3 billion in loan applications was recorded in 2024, higher than RM436.8 billion in 2023. This trend is expected to continue in 2025.”

He also expects infrastructure projects to continue to be the catalyst for residential market performance.

“The LRT3 line, which is expected to be ready by 2H2025, the ongoing expansion of the West Coast Expressway (WCE) and the East Klang Valley Expressway, which is expected to be completed by end-2025, are likely to have a positive spillover effect on surrounding neighbourhoods. These developments will improve connectivity, particularly in suburban areas, potentially driving demand for housing in well-connected locations.”

He adds that the southern part of Selangor is also an emerging hotspot, following the state government’s implementation of the Integrated Development Region in South Selangor (IDRISS).

“IDRISS will house a managed industrial park — NCT Smart Industrial Park — Selangor Aerospace and seven other projects approved in Sepang and Kuala Langat, covering the industrial, logistics, warehouse, education and housing sectors.

“As IDRISS attracts businesses and industries, residential demand in nearby areas such as Cyberjaya, Puchong and Putrajaya will continue to rise. Workers and business owners may seek housing options within a reasonable commuting distance, boosting demand for new and existing properties.

“The state government is also committed to enhancing connectivity between south Selangor and adjacent townships. This could drive higher property values in well-connected locations.”

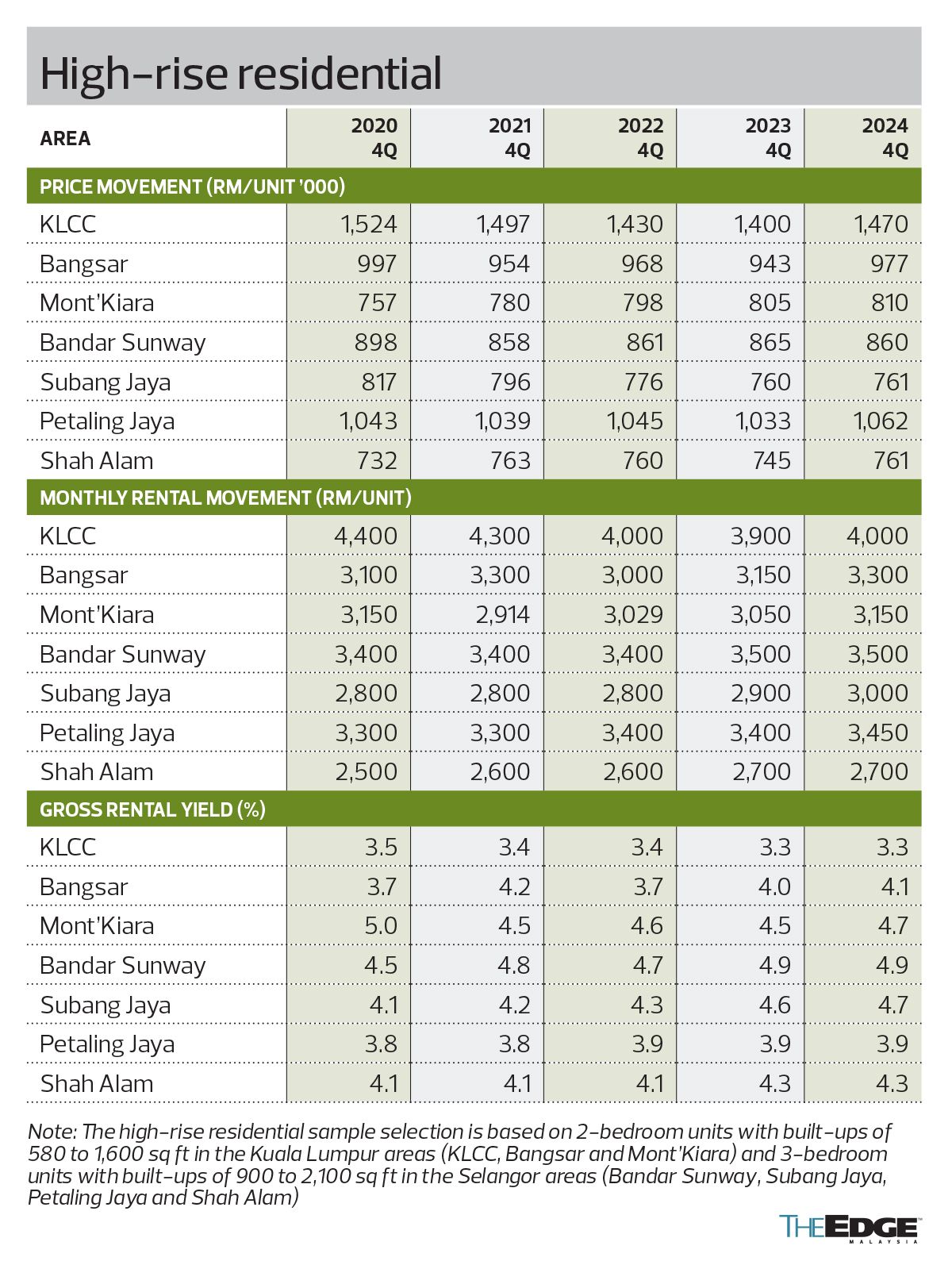

Healthy demand for KL’s high-rise properties

Two-bedroom, high-rise units sampled in the prime KL markets showed healthy demand, with y-o-y improvements in prices and rents in 4Q2024, says Fong.

During the quarter under review, the average transacted unit price in KLCC, Bangsar and Mont’Kiara rose 5%, 3.6% and 0.6% y-o-y to RM1.47 million, RM977,000 and RM810,000 respectively. Average rents for properties in KLCC, Bangsar and Mont’Kiara also grew 2.6%, 4.8% and 3.3% y-o-y respectively.

“Mont’Kiara offered better rental yields than both KLCC and Bangsar. KLCC’s high-rise residential market performance is expected to be sustained by demand from high-net-worth individuals and expatriates, while Bangsar remains a magnet for young professionals and expatriates who enjoy a dynamic and social environment,” Fong says.

A recent completion in KLCC during the quarter under review is OCR Group Bhd’s (KL:OCR) Isola KLCC condominium project on Jalan Yap Kwan Seng. The project comprises 140 units priced at RM1,500 psf.

In Bangsar, there are several high-rise residential projects under construction, including Bangsar Hill Park by Bangsar Hill Park Development Sdn Bhd. The development’s first tower, Talisa, was launched in early 2024 at a starting price of RM893 psf.

The Lantern Bangsar by CDC Asset Management Malaysia Sdn Bhd (the Malaysian arm of Taiwan-based Continental Development Corp) is another ongoing project in the area. It was launched in 2023 and comprises 180 serviced residences priced at RM1,400 psf.

Fong says KL will continue to be a key development hotspot, with developers still actively acquiring land. He highlights several significant land transactions during the quarter, including the acquisition of a 17.58-acre freehold parcel in Taman Taynton by Sunway Bhd’s (KL:SUNWAY) subsidiary Sunway Melawati Sdn Bhd for RM320 million.

“The land is adjacent to Sunway Alishan and will be developed into a mixed-use project with a gross development value (GDV) of RM3.2 billion, comprising serviced apartments and a wellness focused retail podium,” he says.

Another parcel, measuring 13 acres located near the Taman Pertama MRT station in Cheras, KL, was acquired by Radium Development Bhd (KL:RADIUM) for RM458 million during the quarter. The leasehold parcel, Fong notes, will be for a mixed-use development.

The quarter also saw KLCC (Holdings) Sdn Bhd acquiring 486 acres from Bandar Malaysia Sdn Bhd and Bandar Malaysia Land Sdn Bhd. “The site was previously planned for the Bandar Malaysia township,” he says.

Citing Napic’s Property Market Report 2024, Fong highlights that 3,079 high-rise residential units (including serviced apartments and SoHos) priced above RM1 million were transacted in 2024, up 31% from 2,351 transactions in 2023 and representing the highest growth in transaction volume among other property price brackets in KL.

“The government’s intention to make Kuala Lumpur a regional hub for multinational corporations will continue to drive demand for high-rise residential units in KL, especially in the high-end segments,” he says.

High-rise properties in Selangor see steady growth

The sampled three-bedroom, high-rise units in Selangor showed steady growth in both price and rent, reflecting sustained demand, says Fong. “Petaling Jaya and Shah Alam saw moderate price increases while rental rates grew slightly, maintaining stable rental yields.”

In Bandar Sunway, the average transaction price fell 0.6% y-o-y to RM860,000 but average rents were maintained at RM3,500 per month, yielding a 4.9% annual return.

Subang Jaya recorded a slight price increase of 0.1% y-o-y, bringing the average price to RM761,000 in 4Q2024. Average rents rose 3.4% y-o-y to RM3,000 per month, resulting in an annual yield of 4.7%.

Petaling Jaya experienced a more notable 2.8% price increase, with average prices rising to RM1.06 million, from RM1.03 million. Average rents also increased 1.5% y-o-y to RM3,450 per month, yielding a 3.9% return annually.

Shah Alam saw a 2.1% y-o-y price increase, with average prices rising to RM761,000, from RM745,000. Average rents remained unchanged at RM2,700 per month, providing a rental yield of 4.3%.

New projects launched in Selangor during the quarter include Nara by OSK Property Holdings Bhd, the property arm of OSK Holdings Bhd (KL:OSK). The serviced apartment project is part of the developer’s 27.77-acre Shorea Park development in Puchong. Nara offers 709 serviced apartments, with built-ups ranging from 560 to 1,055 sq ft at a starting price of RM250,000.

Berjaya Hartanah Bhd, a wholly-owned subsidiary of Berjaya Land Bhd (KL:BJLAND), has launched Oaka Residences in Bukit Jalil. The project offers 350 serviced apartments ranging from 882 to 1,509 sq ft at a starting price of RM880 psf.

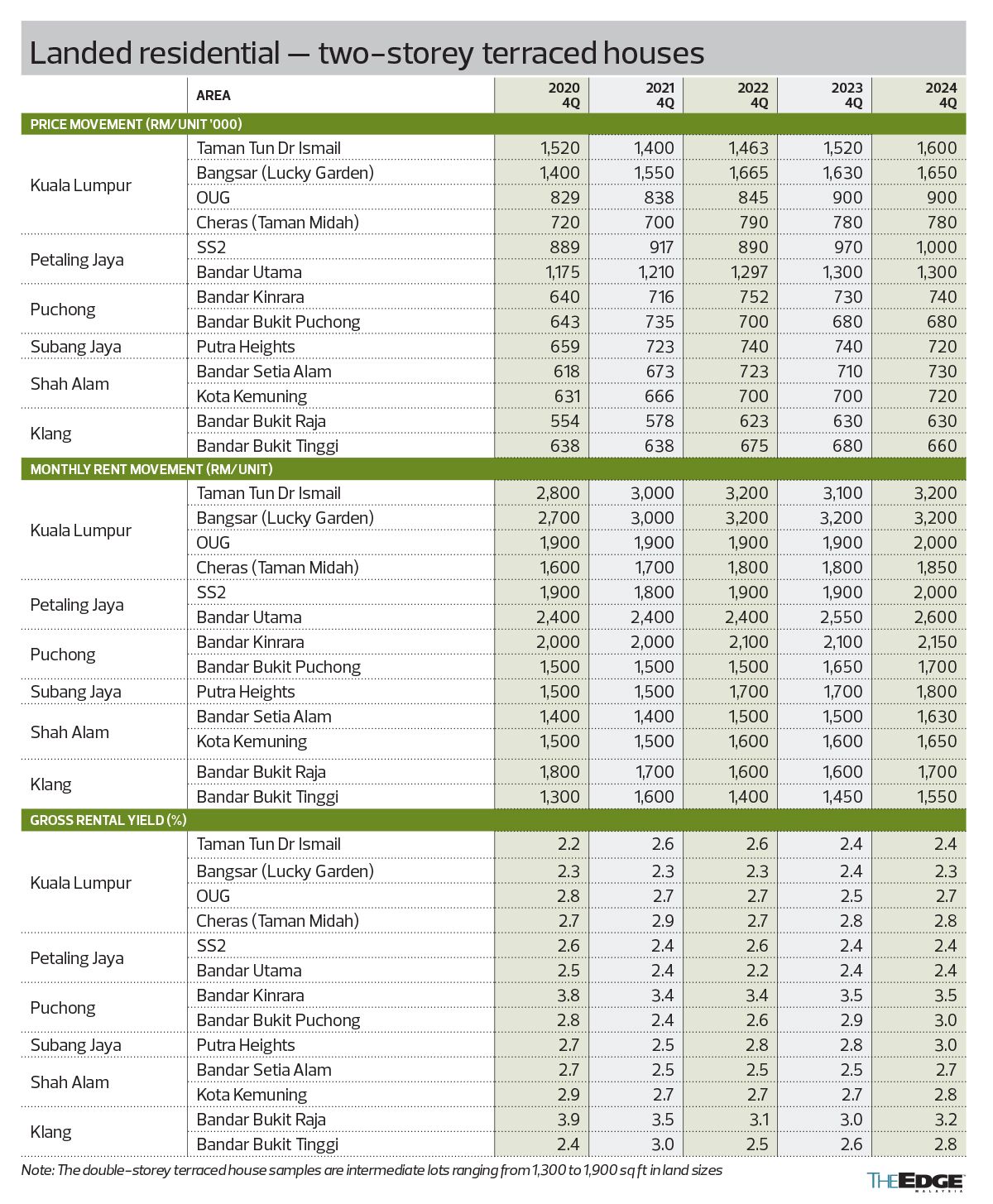

Mixed performance in 2-storey terraced houses

The 2-storey terraced house segment in KL and Selangor saw a mixed performance in 4Q2024, says Fong. “While certain areas such as Putra Heights and Bandar Bukit Tinggi experienced price declines, other locations — including Taman Tun Dr Ismail (TTDI), Lucky Garden in Bangsar and SS2 in Petaling Jaya — saw prices appreciate.”

In Kuala Lumpur, the 2-storey terraced houses sampled in key areas such as TTDI and Bangsar demonstrated positive or stable price trends.

TTDI saw average prices rise 5.3% y-o-y to RM1.6 million, while average rents rose 3.2% y-o-y to RM3,200 per month, yielding an annual return of 2.4%.

Lucky Garden in Bangsar saw a modest increase in average prices of 1.2% y-o-y to RM1.65 million, while average rents remained stable at RM3,200 per month, maintaining a rental yield of 2.3%.

Average prices in OUG held steady at RM900,000 but rents grew 5.3% y-o-y to RM2,000 per month, with a rental yield of 2.7%.

In Taman Midah, Cheras, average prices held steady at an average of RM780,000 while rents rose 2.8% y-o-y to RM1,850 per month, yielding 2.8% annually.

In Selangor, Petaling Jaya’s SS2 saw a price increase of 3.1% y-o-y in average prices to RM1 million, while rental rates rose 5.3% y-o-y to RM2,000 per month, yielding an annual return of 2.4%. Bandar Utama’s average transacted price remained at RM1.3 million y-o-y, with rents increasing to RM2,600 per month, resulting in a 2.4% rental yield.

In Puchong, the two-storey terraced house market saw stable performance with positive market sentiment, notes Fong. The average transacted price in Bandar Kinrara increased 1.4% y-o-y to RM740,000, while average rents grew 2.4% y-o-y to RM2,150 per month, yielding 3.5% annually. Bandar Bukit Puchong saw no change in average prices y-o-y, while rents rose by 3% to RM1,700 per month, providing a 3% annual yield.

In Putra Heights, Subang Jaya, average prices declined 2.7% y-o-y to RM720,000 while rents increased to RM1,800 per month, resulting in a 3% yield.

Shah Alam’s terraced house market remained strong, says Fong, with Bandar Setia Alam’s average price rising 2.8% y-o-y to RM730,000, and rents rising 8.7% to RM1,630 per month, yielding 2.7% annually. Kota Kemuning recorded a 2.9% y-o-y price increase to RM720,000 and rents rose to RM1,650 per month, providing a 2.8% yield annually.

In Klang, average prices in Bandar Bukit Raja remained at RM630,000, while rents stood at RM1,700 per month, generating a 3.2% yield annually. Bandar Bukit Tinggi saw average prices decline 2.9% y-o-y to RM660,000 while rents rose to RM1,550 per month, yielding 2.8% annually.

“The completion of LRT3 in 2H2025 is expected to further attract demand for Bandar Bukit Tinggi and its surroundings,” says Fong.

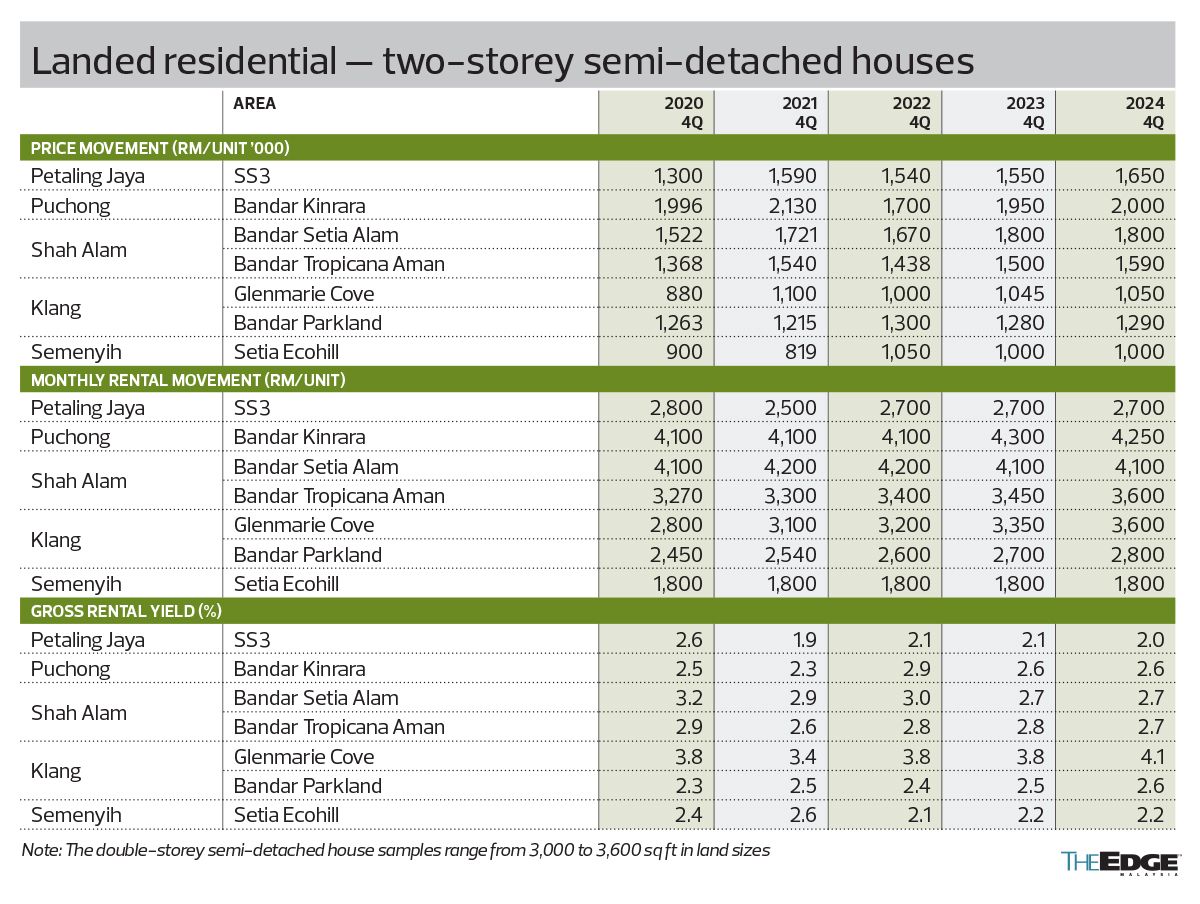

Two-storey semidees enjoy positive performance

The semi-detached housing market in Selangor displayed positive performance during the review quarter, notes Fong.

SS3 in Petaling Jaya saw average prices surge 6.5% y-o-y to RM1.65 million. Rents remained at RM2,700 per month, yielding 2% annually.

In Bandar Kinrara, Puchong, average prices grew 2.6% y-o-y to RM2 million, while monthly rents averaged at RM4,250, offering a 2.6% rental yield.

In Shah Alam, Bandar Setia Alam saw average prices and rents remain unchanged at RM1.8 million and RM4,100 per month, respectively, yielding an annual return of 2.7%. Bandar Tropicana Aman saw a robust 6% y-o-y growth in prices, reaching RM1.59 million, while rents increased 4.3% y-o-y to RM3,600 per month, maintaining a 2.7% yield.

In Klang, average prices at Glenmarie Cove grew 0.5% y-o-y to RM1.05 million, and rents rose 7.5% to RM3,600 per month, delivering a yield of 4.1% annually. Prices in Bandar Parkland grew 0.8% y-o-y to RM1.29 million and monthly rents rose 3.7% y-o-y to RM2,800, resulting in a 2.6% rental yield.

In Semenyih, average prices remained at RM1 million as did monthly rents at RM1,800, yielding 2.2% annually. “Semenyih has seen increased activity for future development. EcoWorld Development Group Bhd (KL:ECOWLD) has reportedly bought ten plots measuring 847.25 acres from Boustead Group for RM742 million for a new RM4.6 billion mixed-use project,” says Fong.

“Despite fluctuations in price trends across different areas, the semi-detached housing market in Selangor has remained generally stable. The strong rental yields in Klang highlight sustained investor interest. At the same time, well-established areas such as Puchong and Tropicana Aman continue to attract homebuyers with consistent price appreciation,” he adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Berkshire dismisses 'false' reports on Buffett comments after Trump shares video

- Trump’s TikTok plan upended by Chinese objections over tariffs — Bloomberg

- LTAT moving forward despite challenges

- China’s rare earths curbs put multiple US industries at risk

- Malaysian Highway Authority: 20km traffic jam on KL-Karak Highway as Raya travellers return

- FMM flags significant challenge for 200 businesses amid 20-day gas disruption after Putra Heights fire

- Melaka to host Visit Malaysia 2026 launching ceremony, says Anwar

- From Ray-Bans to wigs, US buyers may see unexpected price hikes

- Second batch of Putra Heights fire victims get temporary vehicles

- My Say: Taking inspiration from bacterium: the devolution of power