This article first appeared in The Edge Malaysia Weekly on March 17, 2025 - March 23, 2025

WERE it not for the sanitiser dispensers and occasional faded signage mandating the wearing of masks at all times in some buildings, one would hardly remember the Covid-19 outbreak about five years ago that led to a global pandemic.

Life seems to have picked up from where it took a hard stop in 2020, with employers now requiring staff to return to the office, shopping malls packed with shoppers and popular holiday destinations often fully booked.

Not only has the economy returned to normalcy, new areas of growth have been identified. In the last few years, Malaysia has become increasingly popular with foreign investors, many of whom consider the country ideal for data centres.

Investments in 2024 by multinational corporations, including Microsoft, Google and Oracle Corp, have boosted the narrative.

At the same time, Malaysia has worked hard at climbing up the electrical and electronics (E&E) supply chain value add, recently announcing a deal that it hopes will help it attain a breakthrough. More specifically, it will pay semiconductor design firm Arm Holdings plc RM1.11 billion over 10 years in exchange for intellectual property (IP) licences and compute subsystems (CSS).

“The economic narrative for Malaysia has generally been positive in terms of the gross domestic product (GDP) numbers, growth drivers, investments and trade improvements. Going by the latest economic collaborations, Malaysia has made steady progress to diversify and reinvent itself for the next phase of growth,” notes UOB Malaysia senior economist Julia Goh.

In terms of GDP growth, most of the major economic sectors are now back to pre-pandemic levels. Manufacturing was the fastest to rebound to pre-pandemic growth rates as the sector benefited from glove makers churning out tens of millions of gloves desperately needed during the pandemic and the tech up cycle in 2021.

That said, the quarterly year-on-year growth data for manufacturing has been choppy. After contracting 18.6% in 2Q2020, it rebounded over the next few quarters to hit a high of 26.7% in 2Q2021, before contracting 0.9% y-o-y in 3Q2021. In 4Q2024, the sector registered 4.4% y-o-y growth.

Services, the largest economic sector in Malaysia which contributes slightly more than half to the national GDP, took slightly longer to return to pre-pandemic levels. It was only in 1Q2022 when things started to pick up again and by 4Q2024, the sector had booked 5.5% y-o-y growth.

By and large, it appears that the economy has recovered from the pandemic.

“Headline GDP growth, the unemployment rate, headline and core inflation, and foreign investment applications show a complete recovery from the pandemic. Growth in sectors such as manufacturing, E&E, construction and certain key services such as wholesale and retail trade have also broadly recovered,” says OCBC senior Asean economist Lavanya Venkateswaran.

However, others observe that several sectors are still feeling the lingering effects of the pandemic, one of them being tourism.

“Tourist arrivals in 2024 amounted to 25 million compared with 26.2 million in 2019, but the latest signs indicate that 2025 could see a healthy improvement aided by the visa-free programmes,” says CGS International Securities economist Ahmad Nazmi Idrus.

Another area Goh observes is consumption growth, which has yet to revert to pre-pandemic levels, despite the unemployment rate (3.1% in January) dipping to levels lower than in 2019.

Private consumption grew 5.1% y-o-y in 2024 following a quarterly growth of between 4.7% and 6% y-o-y. For most quarters between 2016 and 2019, private consumption growth came in between 6% and 8.4% y-o-y, while unemployment averaged 3.4%.

“Consumption trends have evolved since the pandemic, whereby we see a shift to services and value-for-money trades. Given the higher cost of living, spending continues, although on tighter budgets,” says Goh.

“While we saw higher household asset growth in the first half of last year, households are also rebuilding their buffers while others have opted to withdraw some of their EPF savings to pare down debt and interest payments. Therefore, some aspects may still be lagging pre-pandemic levels. But overall, there has been progress to lift the country’s growth potential and rebuild buffers to secure growth stability in the face of multiple external challenges.”

Growing debt levels

But what about debt? To combat the standstill in economic activity brought about by the pandemic, many governments amassed significant debt to prevent economic collapse.

IMF Global Debt Monitor statistics show that public debt amounted to 100.4% of GDP in 2020, a drastic rise from 84.9% the previous year. By 2023, the world’s public debt had lowered slightly to 94% of GDP, or US$98 trillion.

Malaysia was no different. It eased its fiscal rules and revised the long self-imposed debt ceiling of 55% of GDP to 65% as the country took on additional debt for various stimulus programmes to rejuvenate the economy.

In total, stimulus measures during the pandemic years amounted to a whopping RM530 billion, with direct fiscal injections from the government making up RM83 billion of the total.

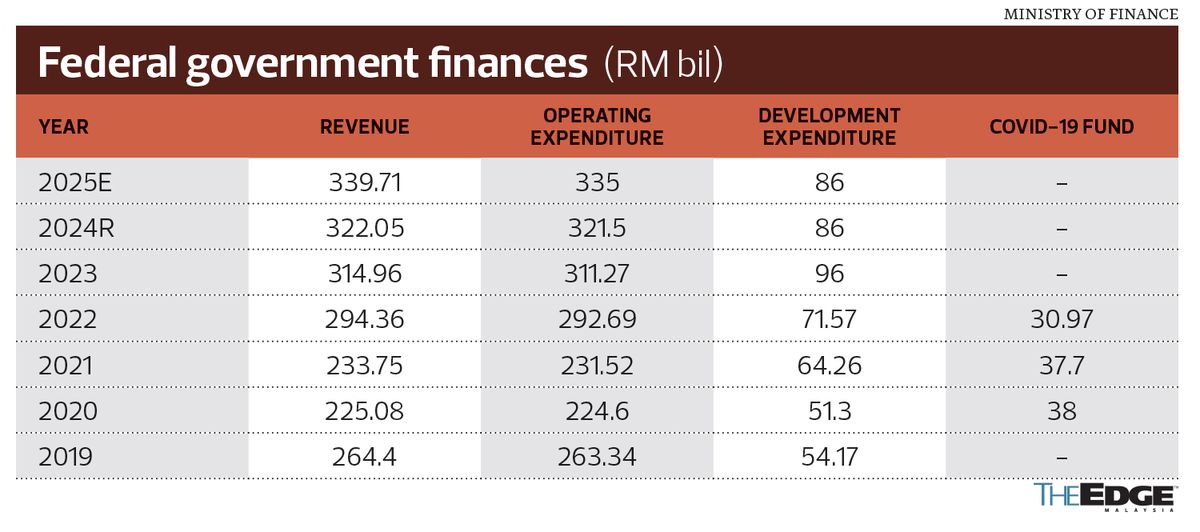

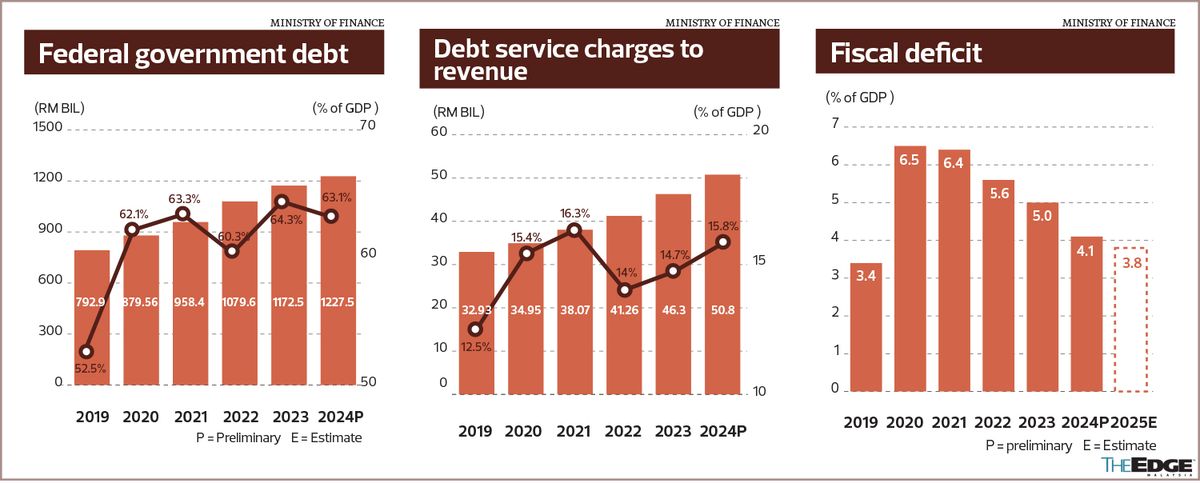

Total federal government debt climbed from RM792.9 billion (52.5% of GDP) in 2019 to RM879.56 billion (62.1%) in 2020, and inched up further to RM958.4 billion (63.3%) in 2021.

Federal government debt breached the RM1 trillion mark in 2022 and has continued to inch up in the following years. As a percentage of GDP, debt hit a high of 64.3% in 2023. By end-June 2024, the latest data available, it stood at RM1.22 trillion, or 63.1% of GDP.

Unfortunately, a substantial amount is spent servicing the huge debt. The preliminary numbers for 2024 showed that the debt service charges (DSC) amounted to RM50.8 billion, which is 15.8% of revenue. The DSC climbed from RM32.93 billion (12.5% of revenue) in 2019 to RM50.8 billion in 2024.

As expected, the fiscal deficit widened from 3.4% of GDP in 2019 to 6.5% in 2020. The deficit amounted to 6.4% in 2021 — the highest since 2009 — before narrowing to 4.1% in 2024. The target now is to lower it to 3.8% this year.

Weighed against the GDP, the government debt appears to be consolidating and its fiscal position improving.

To give credit where it is due, the government did enact the Fiscal Responsibility Act, with the target of reducing the fiscal deficit to 3% of GDP and keeping federal government debt below 60% of GDP in the medium term.

Nazmi, who opines that the fiscal deficit and debt-to-GDP is still elevated, believes that improvements will only come in several years as the government is not willing to cut down on spending drastically. However, he stresses that this exposes the country to risks in a potential recession or slowdown as Malaysia’s fiscal strength is far from optimal.

“While I understand the difficulty of being too fiscally restrictive, I also want to add that the government’s fiscal planning must take into account future recessions. Since 2000, our fiscal position has never really improved to ‘narrower than 3% fiscal deficit’ because of recessions or other reasons. For the government to really ensure it can remain comfortable, it must aim for fiscal metrics well above those thresholds, and I think the government is not doing that,” he observes.

It is worth noting that the government’s limited fiscal space during the pandemic led it to draw down RM5 billion from the country’s National Trust Fund to purchase vaccines even though the objective of the fund is to ensure the optimisation of the country’s non-renewable natural resources as a more sustainable source of revenue for future generations. Every year, Petroliam Nasional Bhd (Petronas) contributes a certain amount to the fund.

As at Dec 31, 2020, the trust fund totalled RM19.5 billion, of which RM10.4 billion consisted of contributions from Petronas and RM9.1 billion from investment returns. The RM5 billion was taken out of the portion from investment returns, while Petronas’ contributions remained untouched.

Do we have a bigger war chest today?

Fast forward to Aug 8, 2024. The Ministry of Finance (MoF) stated in a press release that the National Trust Fund stood at RM20 billion — effectively implying that the RM5 billion withdrawn for vaccines had been replenished.

MoF also said in the statement that the fund would be strengthened as an intergenerational wealth fund for Malaysia with new sources of contributions, revised utilisation guidelines and strengthened investment mandates to ensure sustainability and retention of wealth for future generations of Malaysians.

Beginning in 2024, the government undertook measures to deepen its coffers by enhancing the revenue net. It widened the service tax scope and increased the rate to 8% from 6%. It also introduced a capital gains tax on the net gain from the disposal of shares in unlisted companies.

The implementation of e-invoicing began on Aug 1, 2024, and is being rolled out in phases. E-invoicing is expected to make tax revenue collection more efficient and potentially bring to the surface part of the shadow economy. Some in the industry have commented that when fully implemented, e-invoicing could be as efficient, if not better, as a tool than the goods and services tax regime for tax revenue collection purposes.

On this, the jury is still out.

In May, the scope of the sales tax will be increased to include non-essential and imported goods while the scope of the service tax will be expanded to include commercial service transactions between businesses, such as fee-based financial services. The 2% dividend tax on individuals came into effect on Jan 1, 2025.

Total revenue is expected to increase to RM399.71 billion in 2025 — 5.5% more than the RM322.1 billion in 2024. At RM399.71 billion, it is about 16.3% of the projected GDP. Of the total RM399.71 billion, tax revenue (consisting of direct and indirect taxes) would make up RM259.04 billion, about 12.4% of GDP.

It is worth highlighting that Malaysia’s tax-to-GDP ratio has been hovering at the 12% range for several years now and is below the Asia-Pacific average of 19.3%.

Meanwhile, the government has taken measures to rein in the subsidy bill by raising electricity and water tariffs as well as implementing a targeted diesel subsidy in 2024. Up next is the subsidy rationalisation exercise for RON95 petrol that is anticipated to take place by the middle of this year.

“The upcoming subsidy rationalisation for RON95 will be crucial in achieving a fiscal deficit of 3.8% of GDP for 2025,” Lavanya opines. Goh says it is important to take a gradual approach to allow for improvements, corrections and refinements to avoid any persistent negative effects.

While much more can be done, economists agree that actual reforms are taking place in the country and that Malaysia is moving in the right direction to wean itself off subsidies, widen the revenue base and decrease its debts.

Ultimately, the question is whether Malaysia will be ready to face another unexpected crisis down the road.

Cashless is now king

Cash is no longer king, so to speak. Going cashless is now vogue. The need for physical cash has declined dramatically since the pandemic, with even micro businesses, like your favourite roadside nasi lemak stall, already equipped with their own Quick Response (QR) code.

“I don’t carry a physical wallet anymore. I usually pay for items with my e-wallet or virtual credit card. The e-wallet is a convenient option because of the auto top-up option. [But] these methods are all great until your phone runs out of battery,” jests a working professional in his 30s.

Having said that, there are also those who prefer to hold some physical cash for “emergency situations”.

“Yes, I do have more than RM100 in my wallet at any given time, but I can’t recall the last time I withdrew cash from the ATM,” comments an individual who works in the Klang Valley. “The cash is there for emergencies — for example, when there is no internet connectivity and I can’t pay with my e-wallet or when certain areas still require cash for parking. I pay for my daily expenses with my e-wallet or credit card.”

Without a doubt, Malaysians have eagerly embraced electronic payments since the pandemic hit. The fear of having to handle physical cash during the pandemic and not knowing its provenance — where it had been previously or who had touched it — became a matter of convenience when the pandemic ended.

Business owners seem to prefer it as well. A neighbourhood coffee joint in Kuala Lumpur went cashless as soon as it was allowed to welcome customers again after the mandatory movement controls.

Says the owner of the café: “I don’t have to make runs to the bank to physically bank in the money anymore. It’s also much more convenient for our customers and we don’t have to worry about not having enough change when a customer hands us a big note. The only downside to this is that we get fewer tips these days.”

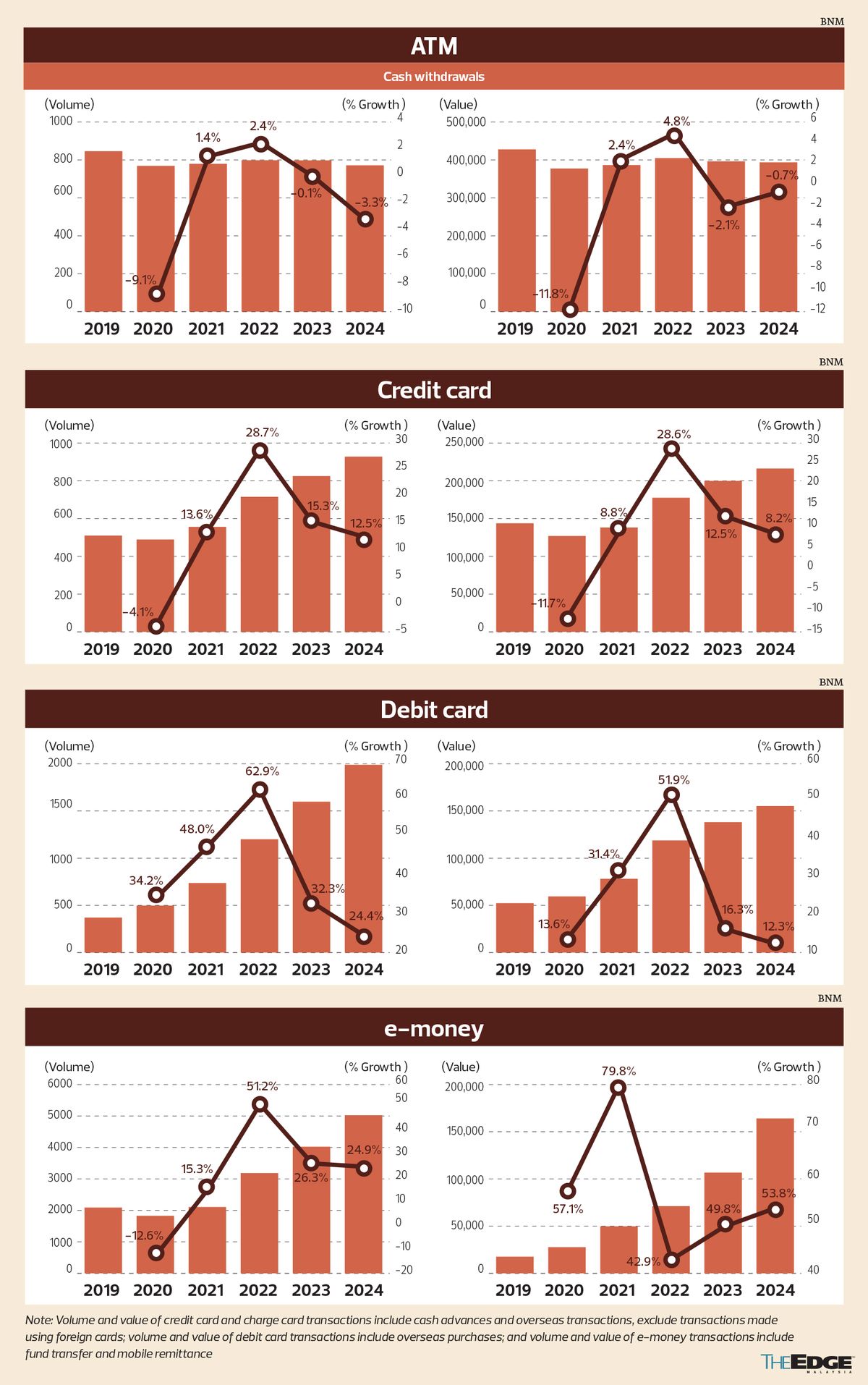

According to Bank Negara Malaysia data, the use of e-money as a form of payment instrument in both volume and value increased from 2019 to 2024. The volume of e-money, which includes fund transfer and mobile remittance, stood at 2.09 billion transactions in 2019, with the total value at RM17.63 billion. By 2024, the number of e-money transactions had increased to 5.02 billion and total value had jumped to RM164.09 billion.

Transaction volume and value for both credit and debit cards have also grown over the same period, although debit card transactions grew faster than credit cards.

In terms of transaction volume, debit cards have outpaced credit cards, as the former jumped from 371 million transactions in 2019 to 1.99 billion in 2024. Credit cards gained from 510.1 million transactions in 2019 to 928.1 million in 2024.

Nevertheless, credit card transaction value remains substantially higher than debit cards. In 2024, the transaction value of credit cards amounted to RM216.24 billion compared to RM155.22 billion for debit cards.

At the same time, Bank Negara payment data also recorded that ATM cash withdrawals were lower in 2024 compared with 2019, when the number of cash withdrawals stood at 845.9 million, with RM427.78 billion in withdrawals. By 2024, the number had declined to 771.5 million transactions, with RM393.55 billion in withdrawals.

TnG Digital Sdn Bhd, one of the leading players in the e-wallet space in Malaysia through TNG eWallet, says it has seen consistent growth in transaction volume and value over the last seven years, driven by increasing consumer adoption and widespread merchant acceptance as a form of payment across various sectors. It adds that what has helped with the adoption growth of e-wallets are the government’s e-Subsidy initiatives. TnG Digital says that in the most recent eMadani programme, 85% of eligible Malaysians chose to claim their e-Subsidy through the TNG eWallet.

Currently, TNG eWallet has close to 23 million verified users, where nearly half of them are active users who transact on a monthly basis.

ShopeePay, which launched its e-wallet towards the latter half of 2019, has certainly seen a steady pace of adoption and user rate since it started operations.

“Through the MCO period (1Q2020 to 4Q2021), we saw a strong and continuous growth in our e-wallet, ShopeePay, specifically in usage and adoption. In 2020, we began to see upsurges of new user activation and transactions, with 2020 recording a 240% increase in the number of active users from 2019. This trend continued as Malaysians remained indoors for an extended period, as 2021 recorded an additional 83% growth in the number of active users from 2020,” a spokesperson from ShopeePay tells The Edge.

The spokesperson also says the integration of ShopeePay with the Shopee e-commerce platform resulted in a decline in “cash on delivery” payments for parcel deliveries, which were available on the e-commerce platform and, in turn, a climb in ShopeePay payments.

ShopeePay’s spokesperson also points out that the uptake in its e-wallet was not limited to the urban and the young; its data shows those in less urban areas and the older generation embracing e-wallets as well.

“Twenty-five per cent of new ShopeePay users from 2020 to 2021 hailed from the northern states of Kedah, Kelantan, Terengganu, Perlis and about 20% of the new users were from East Malaysia. In the same period, we also observed that 32% of new ShopeePay adopters were aged 41 to 65+,” he says, adding that the introduction of the DuitNow QR system helped to further propel use of its e-wallet.

After the pandemic, the spokesperson says, the company is recording “healthy and steady” growth in the use of ShopeePay and its SPayLater (buy now, pay later scheme), as consumers have grown accustomed to integrating e-payments and other digital financial services into daily life.

Competition is intense in the e-payment space, often leaving consumers spoilt for choice and gravitating to the providers that offer the best deals. Yet, TnG Digital believes the e-payment space still holds immense growth potential.

A TnG Digital spokesperson says: “According to Bank Negara payment statistics, e-money transactions currently account for about 30% of total payments, indicating significant room for expansion as cashless adoption deepens. As consumer behaviours evolve, digitalisation progresses and financial inclusivity efforts strengthen, e-wallets and digital payments will continue to play a pivotal role in shaping Malaysia’s payment landscape. Looking ahead, sustained growth will depend on continuous innovation, enhanced security and seamless user experience to build trust and drive further adoption.”

As for existing e-payment users who have gone cashless, it would be hard for them to imagine returning to physical cash anytime soon.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- World Economic Forum highlights EPF as model for sustainable retirement reform

- Li Ka-shing's CK Hutchison mulls global telco assets spin-off, eyes London listing, Reuters reports

- U Mobile secures MCMC award, gears up for nationwide 5G roll-out

- Indonesians feeling market gloom ahead of major holiday

- Seeking opportunities in a risk-off market

- Trump pressing advisers for tariff escalation ahead of April 2, Washington Post reports

- Myanmar's quake toll passes 1,000 as extent of devastation emerges

- MetMalaysia can issue quake warnings within eight minutes, says DG

- Li Ka-shing's CK Hutchison mulls global telco assets spin-off, eyes London listing, Reuters reports

- Vance accuses Denmark of not keeping Greenland safe from Russia, China