(Photo by Low Yen Yeing/The Edge)

This article first appeared in The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

ANALYSTS largely believe that CIMB Group Holdings Bhd’s (KL:CIMB) Forward30 (F30) strategic plan — which aims to boost return on equity (ROE) to 12%-13% by 2027, from 11.2% in 2024, and ultimately position CIMB among Asean’s top quartile by 2030 — is not beyond reach, given its strong regional presence, solid capital position and clear focus on growth.

Yet, beneath the optimism, the six-year plan may also see hurdles in the form of execution risks, economic headwinds and the ever-present challenge of maintaining cost discipline.

Affin Hwang Investment Bank analyst Tan Ei Leen sees the plan as crucial for CIMB in future-proofing its position and driving its sustainable growth, but she cautions that headwinds remain.

“At this juncture, we have not factored in the potential for CIMB to scale or optimise its capital in our model as there are other factors like rising geopolitical risks, which could derail many of our assumptions,” Tan tells The Edge. Affin Hwang nevertheless has a “buy” call with a RM9 target price on CIMB.

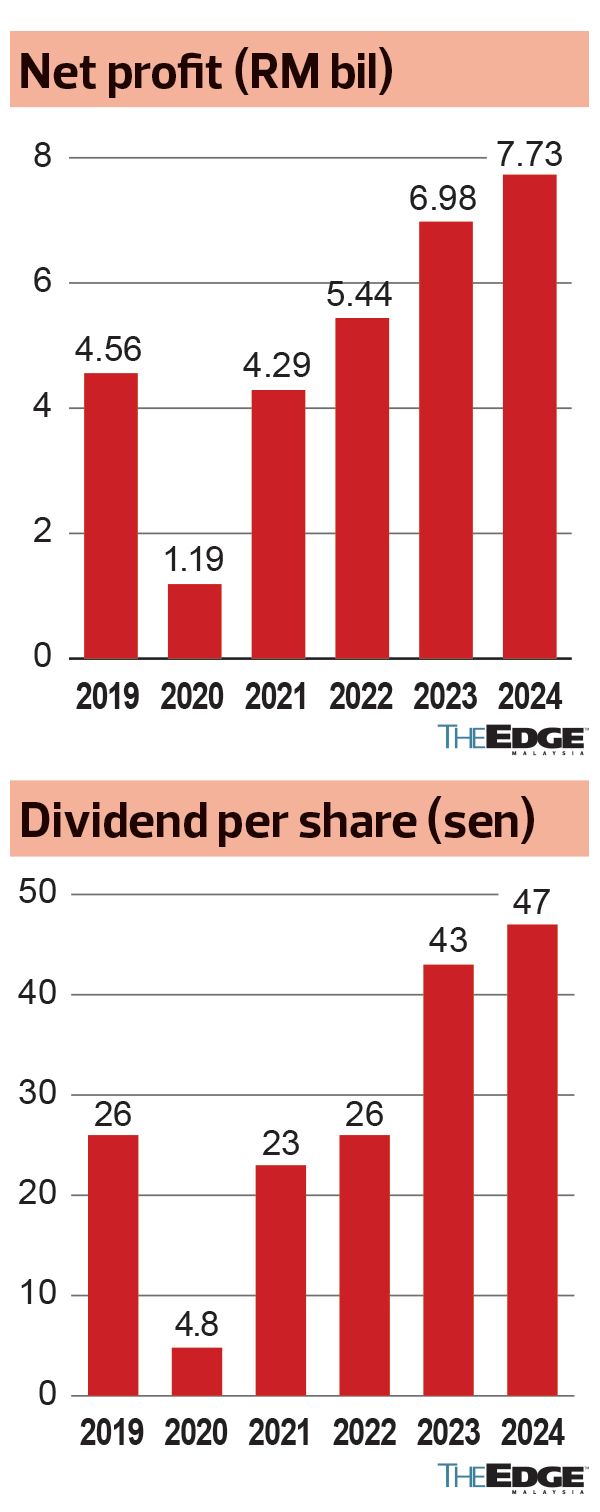

The F30 targets CIMB aims to achieve by 2030 are: (i) to increase the CASA (current account saving account) ratio to 45% (from 43.1% in 2024) so as to lower funding costs by 10 to 20 basis points; (ii) raise non-interest income contribution to 33%-34% (from 31% in 2024) through enhanced cross-selling, wealth management and wholesale banking; (iii) lower the cost-to-income ratio to the low 40% range (from 46.7% in 2024), as well as optimise the common equity tier 1 (CET1) ratio to 13%-14% (versus 14.6% in 2024).

Nomura Research says that on the whole, it is “positive” on CIMB’s F30 plan.

“That said, in the near term, the key challenge which the bank is facing is the deteriorating Indonesia banking-sector liquidity squeeze, Thailand asset quality/subpar return profile, along with broader geopolitical uncertainties. We think CIMB’s group ROE target of 11%-11.5% in the first year of F30, while seemingly flattish versus FY2024’s 11.2% achievement, is conservative precisely to take into account Indonesia’s macro concerns,” its banking analyst Tushar Mohata says in a March 5 report.

The 2030 targets are, however, “reasonable and achievable”, given the long time horizon, he opines.

“That said, we think the group has to shift gears again to grow the commercial business, after scaling it down during Forward23+ [the previous five-year strategic plan], which might take some time, given the other competing banks’ focus on this segment too. Note that almost one-third of senior management’s total compensation is linked to delivering ROE targets, with the remaining split equally between fixed pay and balanced-scorecard performance,” he says.

MIDF head of research Imran Yassin Md Yusof believes it is not a “big task” for CIMB to achieve an ROE — a key measure of profitability — of at least 12% in the mid-term, given that its current ROE is not far off, at 11.2%.

MIDF, which has a “buy” call and RM9.15 target price on the stock, favours CIMB’s ambition to maintain a 55% dividend payout ratio under F30, which is seen as a positive signal for investors as the bank balances profitability with shareholder returns.

“Investors should take it as good news. Achieving this ROE but then still maintaining [the dividend payout] without sacrificing the rewards to shareholders is pretty important, and this is done by optimising the CET1 ratio,” Imran says.

AskEdge data show that CIMB offers a trailing 12-month dividend yield of 7% based on last Thursday’s closing price of RM7.50. (Note that AskEdge’s dividend yield only takes into account dividends that have gone ex.)The banking group, the country’s second largest by assets, declared a total dividend per share of 47 sen for the financial year ended Dec 31, 2024 (FY2024) — its highest annual payout ever.

CGS International, meanwhile, believes that CIMB will find it a challenging task to lower its cost-to-income ratio to the low 40% range over the next six years.

“The bank would have to continue to incur additional costs for business growth while total operating revenue growth would be at single rates per annum in the next six years. To achieve this, CIMB would have to exercise significant cost discipline and utilise technology (including artificial intelligence) to reduce some of its costs, in our view,” CGS said in its note following the F30 strategy presentation.

Under the F30 strategy, CIMB intends to reallocate capital towards high-return businesses in commercial and wealth banking, particularly in Indonesia and Singapore, while focusing on cost optimisation in Thailand — and this is where CIMB may face execution risks, particularly in Indonesia.

“CIMB Niaga (a 92.5%-owned Indonesian subsidiary of CIMB) would be my main concern, as we do believe Malaysia operations to be relatively resilient, whereas Indonesia is juggling with funding cost pressures,” Kenanga Research banking analyst Clement Chua says.

Bloomberg data show that 16 analysts have a “buy” call on CIMB’s stock and five have a “hold” recommendation. There are no “sell” calls. The 12-month average target price is RM8.87, which suggests an upside potential of 18% from its closing price of RM7.52 last Friday. At that price, CIMB has a market value of RM80.7 billion.

The counter, however, has dropped 8.3% so far this year.

“All in all, we are of the view that CIMB is in a sweet spot to capture the promising growth of Asean’s future on the back of the young and affluent population, rising intra-Asean trade and economic integration, and sustainable influx of foreign direct investments (FDIs). CIMB continues to offer an attractive value proposition as a proxy to Malaysia’s rising dominance in Asean as a hub for FDIs and data centres,” Affin Hwang says in a March 5 report.

“The recent selldown on CIMB is unjustified in our view as the market may be concerned about underlying risks, given management’s conservative guidance on its 2025 ROE target of 11%-11.5% as well as credit/market risks of operating in Indonesia due to the tightening in system liquidity,” it adds.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- The bigger picture behind Tabung Haji’s dividend announcement

- Bukit Aman calls up corporate figures to assist in investigations on MBI's money trail — sources

- Nvidia AI chip fraud case under probe, Miti continues to cooperate with investigation team, says Zafrul

- Velesto, Astro, Binastra, MCE Holdings, Axiata, Cape EMS, Malton, Press Metal, Capital A, KNM, Ge-Shen, Tex Cycle, K Seng Seng

- Anwar gives Zafrul green light to helm Badminton Association of Malaysia

- Russia, Ukraine agree to sea, energy truce; Washington seeks easing of sanctions

- Asian stocks edge up as traders seek new direction

- China's CATL Hong Kong listing approved, could raise at least US$5b — Reuters

- Oil gains as industry report points to big drop in US stockpiles

- EU trade chief meets with Trump officials to try to head off 'harmful' tariffs