This article first appeared in The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

THE last five years have seen CIMB Group Holdings Bhd (KL:CIMB) working diligently to improve its return on equity (ROE) — a key measure of profitability — and other important financial metrics that had fallen behind those of its rivals.

This turnaround work, crafted under its Forward23+ (F23+) strategic plan that concluded last year, seems to have paid off for the country’s second, and Asean’s fifth, largest banking group by assets.

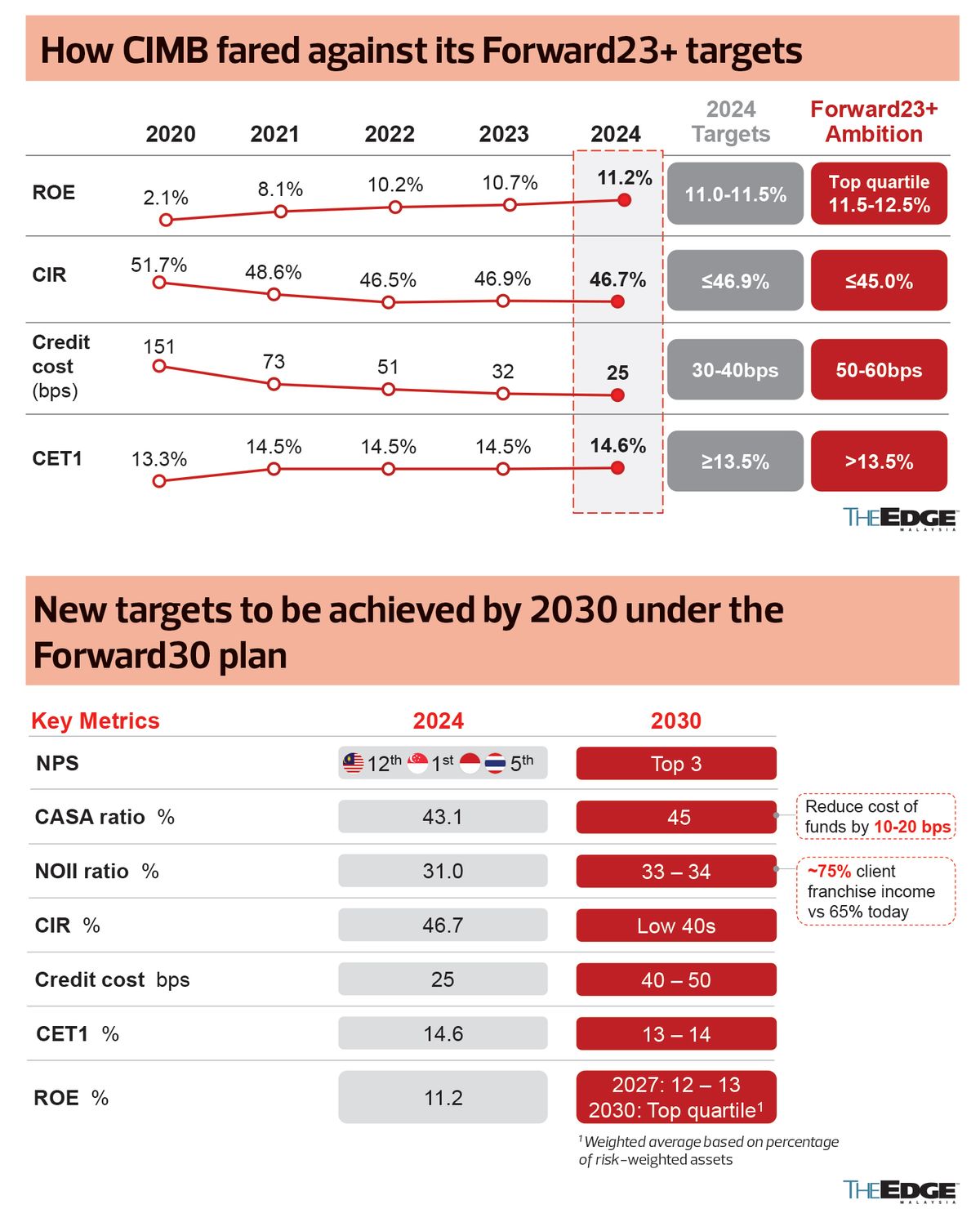

Its ROE, which had sunk to a low of 2.1% in 2020 — the first year of the pandemic — has risen markedly over the years, reaching 11.2% in 2024, among the highest in the industry and within its targeted range of 11% to 11.5%. (Its original target was 11.5% to 12.5%, but this was revised sometime mid-term to take into account the industry’s stiff fight for deposits, which took a toll on banks’ net interest margins.)

For perspective, Malayan Banking Bhd’s (KL:MAYBANK) ROE stood at 11.1% in 2024, while Public Bank Bhd’s (KL:PBBANK) was 13.2%.

CIMB’s cost-to-income ratio (CIR) — a measure of efficiency — managed to come down to 46.7% in 2024 from 51.7% in 2020, while its gross impaired loan ratio — an indicator of asset quality — improved significantly to 2.1% from 3.6%.

Notably, its net profit rose to a record high of RM7.73 billion for the financial year ended Dec 31, 2024 (FY2024) — up 10.7% year on year (y-o-y) — and it declared its highest ever annual dividend of 47 sen a share that year, which included a special dividend of seven sen a share for the second straight year.

Now that it is back on a stronger footing, CIMB wants to accelerate its growth, group CEO Novan Amirudin says. CIMB is open to undertaking mergers and acquisitions (M&A) to grow, if a good opportunity arises and it brings value to the group.

“It doesn’t have to be one large M&A. It can be smaller bite-sized opportunities,” Novan tells The Edge in an exclusive interview, his first since taking on the top job on July 1 last year. “We roughly know what is out there [in terms of M&A opportunities]. But, I don’t see anything highly actionable that makes sense for us at the moment.”

He reveals that the group had its eye on Indonesia’s Bank Commonwealth last year, but lost out on that opportunity to OCBC, whose Indonesian arm acquired the lender for IDR2.2 trillion in May.

Recent news reports, including by The Edge, indicate that CIMB is keen on a sizeable stake in Bank Pan Indonesia (Panin Bank) which is reportedly up for sale. Novan, however, declines comment when pressed about Panin Bank.

Novan is an old hand at M&A, having come from an investment banking background. He took up the reins from Datuk Abdul Rahman Ahmad, who left CIMB after four years to take on the role of Permodalan Nasional Bhd president and group chief executive for the second time.

CIMB’s biggest shareholders are Khazanah Nasional Bhd with a 21.54% stake, followed by the Employees Provident Fund with 16.98%, Amanah Saham Nasional Bhd with 9.88% and Retirement Fund Inc (KWAP) with 6.08%.

Transforming under Forward 30

Last Wednesday (March 5), Novan introduced to the investment community CIMB’s new strategic plan, called Forward30 (F30), that will run for the next six years to FY2030.

“I always believe that you have to keep transforming because if you don’t, those around you will, and you will get relegated down. So, while we are happy with what we’ve achieved so far — we hit most of our F23+ targets — we need to embark on the next wave of transformation,” he states.

The F30 plan, designed to accelerate CIMB’s growth, sees it ultimately aiming to achieve a top quartile ROE among regional peers by FY2030. While it did not attach a specific number to its ROE goal, the shorter-term target is to achieve a ROE of 12% to 13% by FY2027.

Its other targets to achieve by FY2030 are: a Top 3 position in net promoter score, which is a gauge of customer service; a CASA (current account and savings account) ratio of 45%; a non-interest income ratio of 33% to 34%; and a CIR in the low 40% range. Meanwhile, credit cost is expected to normalise to about 40 to 50 basis points (bps), from 25bps in 2024.

To achieve these targets, CIMB will focus on: (1) reallocating and optimising its capital and resources to strengthen its overall portfolio, (2) building a leading deposit franchise to reduce its cost of funds by 10bps to 20bps by 2030, (3) doing more cross-selling to generate better returns, and (4) improving its capabilities through a “simpler, better, faster” approach to increase productivity and efficiency.

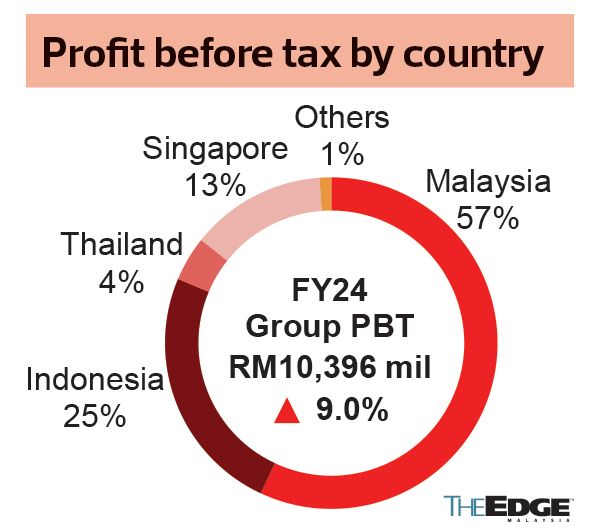

On capital allocation, Novan says CIMB intends to optimise allocation towards its “higher-return versus risk and probability of success” countries — namely Malaysia, Indonesia and Singapore — and businesses such as commercial banking and wealth management.

“Today, 54% of our capital is in Malaysia and we get back 57% in earnings, and the ROE is about 11%. In Indonesia, we have 19% of our capital there, but we get back 25% in earnings and ROE is about 14.6%. At the other extreme is Thailand, where we have 12% of our capital but are only getting back 4% in earnings, and the ROE is about 5.9%.

“When we re-evaluate our portfolio, we find this is not optimal. We need to reallocate our capital to areas that bring in better returns versus risk, with higher probability of success,” he adds.

Thailand, with its sluggish economic growth and political uncertainties, has been a challenging market for the group for some years now. Be that as it may, there are no plans to exit the country, Novan says.

CIMB wants to reshape its consumer banking business there and is considering options.

“We need to study Thailand. It’s a 2% GDP (gross domestic product) market and it’s been challenging, but it remains an important market for us. We want to be very niche in the areas we are strong at there, which is wholesale banking, wealth,” he says.

In Malaysia, CIMB plans to accelerate growth in commercial banking — under which its small and medium enterprise business falls — while maintaining the pace of its consumer and wholesale banking businesses.

As for Singapore, where it currently has only one branch, it aims to be the top challenger bank, focusing on growing its Asean corporate network and wealth management business.

“There were two branches before, now it’s just one, but that one branch brings in 13% of our [pre-tax] profit,” he remarks.

Shariah spin-off in Indonesia

It will be interesting to watch CIMB’s developments in Indonesia over the next few years. Apart from potential M&A moves there, its Indonesian subsidiary — Bank CIMB Niaga — is expected to spin off its Islamic banking business next year.

“By law, we need to get the spin-off done by [the end of] next year, but we are planning for it already,” Novan shares.

He sees this as a huge opportunity for CIMB to truly solidify its position as the second largest Islamic bank there after Bank Syariah Indonesia (BSI). Though Indonesia is the world’s most populous Muslim nation, only 8% of the country’s banking assets is Islamic compared with over 40% in Malaysia.

“There is a lot of upside, so I’m quite excited about this opportunity. Yes, BSI is the No 1 player, but there will be people who will want to diversify their funds. Not everyone will want to keep all their funds in one bank. That is where we come in,” he says.

Indonesia mandates a spin-off — basically, a separation — of shariah business units exceeding IDR50 trillion (RM13.57 million) in assets or holding more than half of the parent bank’s assets. These units have to be converted into separate banks or transferred to other banks by the end of 2026.

BSI was created in 2021 from the merger of the Islamic banking units of three state-owned lenders, including Bank Mandiri.

In Indonesia, CIMB is aiming to be the most profitable bank in the so-called KBMI 3 category, which groups together lenders with a core capital of between IDR14 trillion and IDR70 trillion.

Bank CIMB Niaga is understood to be the sixth largest by assets there, with total assets of IDR360.2 trillion as at the end of 2024.

Despite the strong prospects in Indonesia, it is expected to be a tough market for banks given the tighter liquidity there.

Analysts say CIMB’s net interest margin at the group level may continue to come down this year, albeit by not more than 5bps because of funding cost pressures from its overseas markets, especially Indonesia.

Rising challenges

With growing geopolitical tensions and economic uncertainties globally, it remains to be seen if CIMB can deliver on its F30 targets as intended. Acknowledging that it will be challenging, Novan nevertheless points out that F30 was designed to navigate a complex and uncertain world.

“It is all down to execution. To me, that’s the key,” he says.

As at March 7, most analysts had a “buy” call on CIMB. The share price, which has more than doubled over the last five years, hitting a high of RM8.44 on Sept 20 last year, closed at RM7.52 last Friday, valuing CIMB at RM80.71 billion.

“Even though we find a lot of strategies and focus areas are similar to those of its rivals, we reckon execution is key and to back this up, CIMB has shown its capabilities to deliver results over the past four years. Also, the bank still has a lot of levers to pull to help achieve its shorter-term ROE target of 12% to 13% in 2027,” says Hong leong Investment Bank Research in a March 5 report.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Who paid the highest dividends in FY2024?

- Türkiye's market rout worsens amid protests, worst stock slump since 2008

- Dow transports index slump poses trouble spot as investors seek stocks stability

- Trump to strip legal status from 532,000 migrants living in US

- Canada aims for free internal trade that can offset any US tariffs, PM Carney says

- Frontiers of Growth: Emerging Economies Must Get Rich Before They Get Old

- Trump to strip legal status from 532,000 migrants living in US

- Canada aims for free internal trade that can offset any US tariffs, PM Carney says

- Japan, China, South Korea meet at geopolitical 'turning point in history'

- Malaysia Airlines resumes London flights after Heathrow power outage