This article first appeared in Capital, The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

Banking

POSITIVE

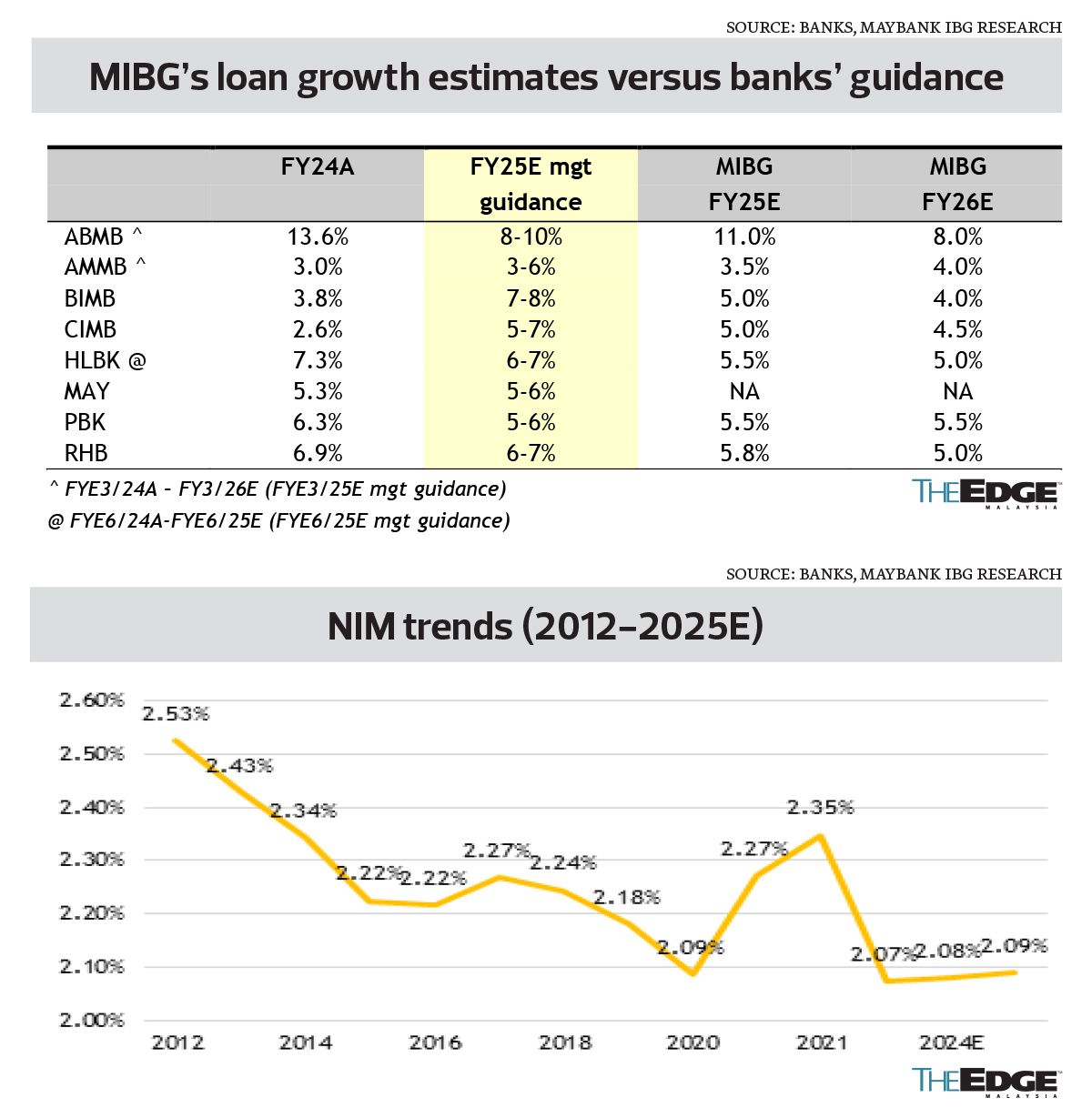

MAYBANK IB RESEARCH (March 4): Banks ended 2024 on a decent note, with all banks under our coverage meeting expectations and AMMB Holdings Bhd (KL:AMBANK) coming in marginally above — there were no disappointments. Cumulative operating income rose 8% y-o-y in 2024, with decent gross loans expansion of 5.5%, stable margins and robust non-interest income (NOII) growth of 16%, led by investment and foreign exchange gains. The JAWS ratio (income growth rate versus expenses growth rate) was mildly positive and operating profit rose 8% y-o-y. Credit cost was lower amid a fairly benign credit environment and cumulative core net profit rose 10% y-o-y. Against the ROE targets set during the year, most banks met expectations. AMMB and Hong Leong Bank Bhd (KL:HLBANK) were close, while Bank Islam Malaysia Bhd (KL:BIMB) was slightly behind at 7.6% versus its ROE target of 8%.

We forecast a cumulative operating profit growth of 5.3% for 2025E and 2026E respectively. This is premised on domestic loan growth of 5.5%, stable net interest margins and an aggregate cost-to-income ratio of 44.7% in 2025E. We project cumulative net profit growth of 5.7% and 5.5% in 2025E and 2026E respectively. We forecast stable ROEs at 10.6%/10.6% in 2025/2026 against 10.5% in 2024.

We expect 2025 to be a stable year for banks, and project operating profit growth of 5.3% and net profit growth of 5.7%. ROEs are expected to average 10.6% and dividend yields currently average about 5.2%. This quarter, we upgraded RHB to a “buy” and downgraded Alliance Bank Malaysia Bhd (KL:ABMB) to a “hold”.

Our top three picks would be Public Bank Bhd (KL:PBBANK), AMMB and CIMB Group Holdings Bhd (KL:CIMB). Public Bank’s RM1.3 billion management overlays should keep credit costs low, LPI Capital Bhd (KL:LPI) will enhance non-interest income and we think that concerns over a share overhang are overblown. AMMB’s focus on proactive funding cost management and business banking operations should contribute to growth momentum, as it strives for higher dividend payouts. CIMB’s operations in Indonesia and Singapore are strong contributors, while a turnaround of CIMB Thai would enhance earnings.

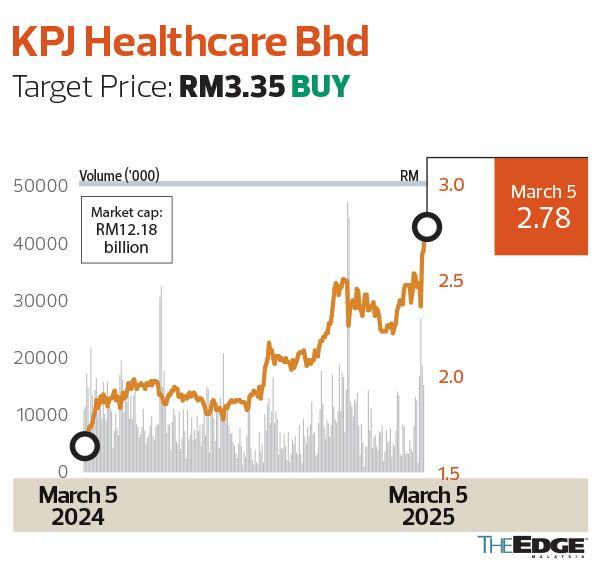

KPJ Healthcare Bhd

Target Price: RM3.35 BUY

CGS INTERNATIONAL (March 3): KPJ Healthcare Bhd (KL:KPJ) saw record quarterly revenue of RM1.05 billion in 4Q24, driven by a 5% y-o-y rise in inpatient volume on the back of a 6% rise in bed capacity throughout FY24. Core net profit for 4Q24 hit a record RM116.3 million, supported by its rollout of centralised procurement for key equipment such as medical devices, pharmaceuticals as well as medical consumables. As a result, KPJ saw its 4Q24 gross profit margin and operating profit margin reach a record 47% and 20% respectively.

KPJ is optimistic about its growth plans. Its 60-bed KPJ Kuala Selangor hospital is set to open by end-1Q25F. The group aims to boost its bed capacity from 4,800 operating beds as at end-FY24 by 50% at end-FY29F through brownfield expansion on top of an additional expansion of 800 beds in its current hospitals. KPJ’s planned expansion should see its capital expenditure remain elevated at RM350 million a year until FY27F.

We raise our FY25/26 EPS forecast by 3.6%/8.7% as we think KPJ will continue to enjoy improved margins, and introduce our FY27 estimates. Our target price is lifted to RM3.35, now pegged to FY26F EV/Ebitda of 13 times, in line with regional hospital players. We continue to like KPJ for its clear profit growth trajectory over FY25/26.

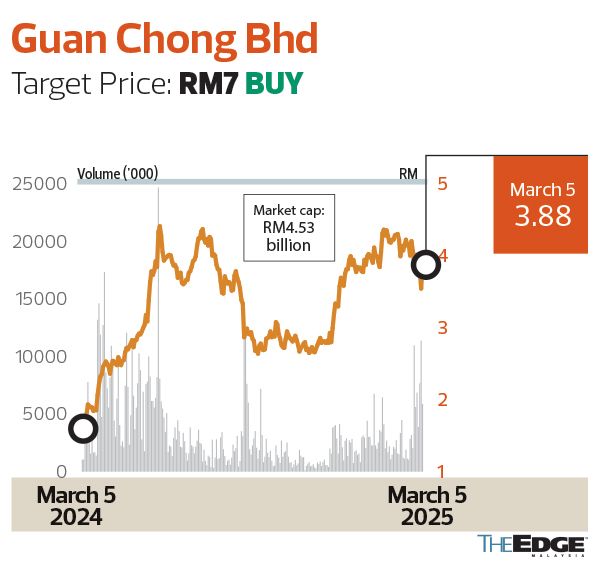

Guan Chong Bhd

Target Price: RM7 BUY

RHB RESEARCH (March 3): Guan Chong Bhd (KL:GCB) has sweetened its historical high full-year results with a proposed bonus issue of four bonus shares for three existing shares and one bonus warrant for four existing shares. We view this move positively as it is set to enhance liquidity, create shareholder value and demonstrate proactive capital structure management.

The proposed free warrant is estimated to yield at least 5% to 6%, based on the current share price at a 1-for-4 ratio. The free warrants could raise up to RM470 million in three years, assuming full conversion at the strike price of RM1.60 (ex) or RM3.73 (cum).

Management guided that the combined ratios sold in FY25 will be higher than the ratios realised in FY24, given the sharp rise in cocoa butter ratio since 2Q24, which has continued into FY25 amid a supply-demand mismatch and a sharp rise in working capital and hedging costs for the grinders. FY24 core earnings more than quadrupled y-o-y to RM455 million, buoyed by higher ASPs (average selling prices), volumes and favourable hedging positions, which more than offset the elevated costs for beans and working capital.

We highlight the potential earnings upside risks stemming from a stronger combined ratios/Ebitda margin from our current conservative assumption of less than RM4,000 per tonne. We keep our forecasts and target price of RM7 unchanged, pegged to FY26F PER of 15 times — on a par with the Consumer Product Index.

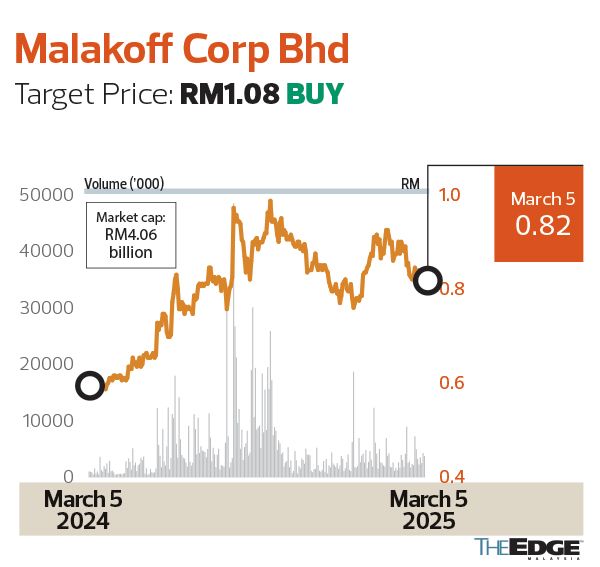

Malakoff Corp Bhd

Target Price: RM1.08 BUY

TA SECURITIES (March 3): Malakoff Corp Bhd (KL:MALAKOF) has completed the acquisition of a 49% stake in E-Idaman Sdn Bhd. Based on previous announcements, Malakoff had offered RM133.2 million to the vendor — Metacorp Bhd — for the 49% stake.

E-Idaman is principally involved in project management, consultancy and contracting services in the field of solid waste management. Its wholly-owned subsidiary Environment Idaman Sdn Bhd provides solid waste collection and public cleansing management services for Kedah and Perlis under a 22-year concession. The concession started on Sept 19, 2011, and will expire in September 2033.

The acquisition will expand Malakoff’s geographical footprint in waste management to the northern region, beyond the group’s current exposure in Kuala Lumpur, Putrajaya and Pahang, via Alam Flora. The acquisition will also immediately increase its waste management capacity by an estimated 700 tonnes per day (TPD), bringing its total effective waste volume from 5,615 TPD to 6,315 TPD (+12%). Additionally, the move is a continuation of the company’s transformation with portfolio diversification that integrates environmental services to achieve a zero-waste circular economy and supports its long-term target of managing 10,000 TPD by 2031.

We raise our net profit forecasts for FY25-27 by 3% to 4% to factor in earnings accretion from the acquisition of the 49% stake in E-Idaman. Our SOP-derived target price is revised higher from RM1.06 previously.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Tan Sri Mohamad Salim appointed as chairman of MACC's Anti-Corruption Advisory Board effective Feb 2 — MACC

- GoTo reiterates no deal in place with any party as it addresses Grab buyout rumours

- Homeland Security slashes personnel in unit leading fight against domestic extremism

- Asian stocks muted, yen softer ahead of BOJ decision

- Shaping future leaders for Malaysia's economic and policy transformation