This article first appeared in The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

DATUK Lim Kian Onn, co-founder and executive chairman of ECM Libra Group Bhd (KL:ECM), has emerged as a white knight for beleaguered Aseana Properties Ltd, a property developer whose listing on the London Stock Exchange (LSE) was pioneered 18 years ago by the Lai family that controlled Ireka Corp Bhd (KL:IREKA) until mid-2021.

Company information from LSE shows that the Malaysian businessman, through his Singapore-based private vehicle Neuchatel Investment Holdings Ltd had, on Feb 26, under a share subscription agreement, subscribed for 68.19 million Aseana shares at US$5.45 million, or eight US cents each, to become the largest shareholder, with a 29.9% stake — just under the 30% mandatory offer threshold.

Aseana owns a portfolio of properties, including The RuMa Hotel and Residences in Kuala Lumpur and Sandakan Harbour Square in Sabah, which comprises Harbour Mall Sandakan and a hotel.

Following the subscription, Legacy Essence Ltd — the investment company of the Lai family — remains one of the largest shareholders of Aseana, although its stake has been pared down to 12.85% from 18.43%. Bloomberg data shows Ireka now owns 20.1% of Aseana shares, down from 23.07%. Hong Kong hedge fund Long Investment Management International Ltd’s stake in Aseana has been reduced to 11.68% from 13.41%, while Swiss investment boutique Progressive Capital Partners Ltd holds a 6.36% stake, from 7.24% previously.

The cash injection will be used to repay outstanding bank facilities to forestall foreclosure proceedings initiated by the receivers and managers of ICSD Ventures Sdn Bhd — a wholly-owned subsidiary of Aseana and owner of Sandakan Harbour Square, which has been placed in receivership — and for working capital requirements.

Lim is no stranger to reviving ailing assets. From 2020 through 2022, Lim was deputy chairman of AirAsia X Bhd (KL:AAX), where he led the then-struggling low-cost, long-haul carrier’s restructuring of RM33.65 billion of its liabilities by paying just 0.5% of debt owed to each of its creditors and terminating all existing contracts.

He currently holds a direct stake of 13.39% in ECM Libra and an indirect stake of 27.22% through Plato Capital Ltd (11.45%), Garynma MY Holdings Ltd (15.49%) and his wife’s shareholding of 0.28%, making him the biggest shareholder. He also serves as executive chairman of ECM Libra’s hospitality arm Ormond Group Sdn Bhd, which operates the Ormond, MoMo’s and Tune hotel brands.

Lim has outlined plans to unlock the full value of Aseana’s assets, according to people familiar with the matter. Aseana’s 2023 annual report shows that the carrying value of inventories for the group was US$118 million as at end-2023.

The sources say Lim is primarily interested in The RuMa Hotel and Residences and Sandakan Harbour Square, whose value is not reflected in Aseana’s stock price, which has slid over the years to an all-time low of eight US cents from its listing price of US$1.

Owing to previous management missteps, Aseana’s valuation has suffered markedly over the past five years, with its shares down 81%. Aseana shares have been trading around the eight US cents mark, valuing the group at US$11.19 million (RM49.55 million).

‘Crown jewels’

Aseana, which was listed on the Main Market of LSE in April 2007, was set up as a property investment fund with the aim of investing in property projects in Malaysia and Vietnam. At the time, Aseana Properties had anticipated that between 30% and 40% of its funds would be allocated to projects in Malaysia, and between 60% and 70% to projects in Vietnam.

As at Dec 31, 2024, the company either owned or held partial interests in three investments in Malaysia, consisting of The RuMa Hotel and Residences, Sandakan Harbour Square and a 172,900 sq m tract in Tuaran, Sabah.

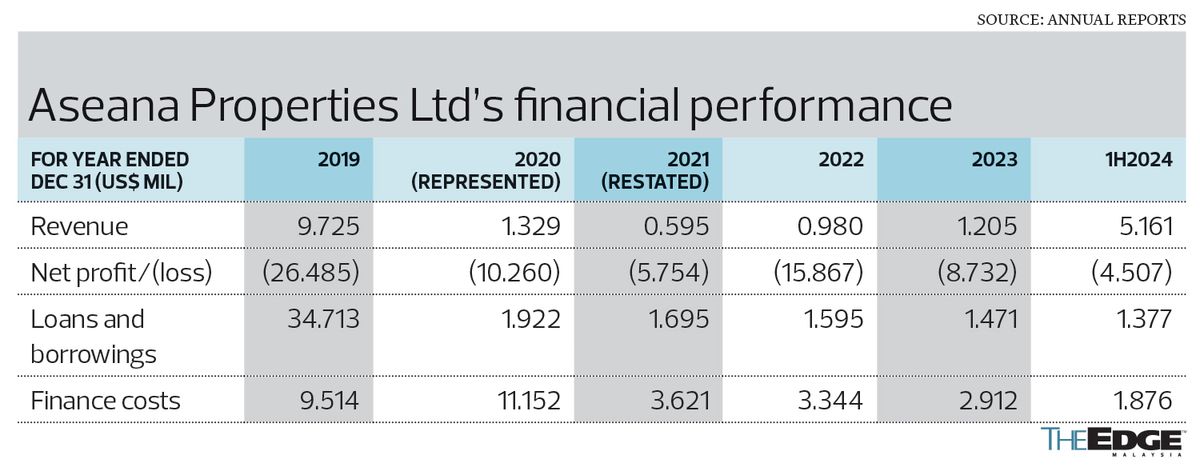

Aseana has been loss-making since the financial year ended Dec 31, 2017 (FY2017). In FY2023, the company narrowed its net loss to US$8.7 million, from US$15.9 million in FY2022. In the first half of 2024, it recorded a smaller net loss of US$4.5 million compared with US$5.9 million in 1HFY2023.

Industry sources say a mismatch between assets and liabilities is partly to blame for its financial problems.

“The whole capital structure of Aseana is wrong. It has good assets but its operating cash flow is used to repay debts. Its long-term development assets were funded by short-term notes at exorbitant interest rates ranging from 12% to 15%,” one source points out, adding that the new shareholder’s immediate plan is to look at refinancing the company’s existing loans at a reduced interest rate.

For the first six months ended June 30, 2024 (1HFY2024), Aseana’s finance costs declined to US$1.88 million, compared with US$2.91 million in FY2023; its total borrowings stood at US$1.38 million as at end-June 2024.

People close to the company also say Aseana has suffered from lack of focus since the passing of Datuk Lai Voon Hon — former chairman and group managing director of Ireka, who was the promoter and prime mover of Aseana — as well as the removal of the Lai family from the running of the company.

“Activist shareholders from London and Switzerland who had no understanding of hospitality or operational aspects of business took over the running of the company and appointed ill-equipped directors to oversee its operations. And these directors did not act in the best interest of the company,” says a source.

Last December, Aseana and its subsidiary Urban DNA Sdn Bhd (UDSB) filed a lawsuit against four former directors — Helen Wong Siu Ming, Nicholas John Paris, Tan Hock Chye and Thomas Patrick Holland — as well as Holland’s wife, Jenny Lee Gyn Li, and RSMC Investment Inc at the Kuala Lumpur High Court over claims of financial misconduct and breach of law. Wong also sits on the board of Singapore-listed CapitaLand Investment Ltd as non-executive independent director.

According to the plaintiffs, in February 2024, Paris and Tan authorised loans amounting to US$1 million with a 15% interest rate from Wong, Lee and RSMC, which exceeds the legal limit set by the Moneylenders Act 1951. Wong, Tan and Holland also authorised the use of more than 30 units in The RuMa Hotel owned by UDSB as security for the loans.

The plaintiffs further contended that the charged properties, valued at US$6.56 million, were disproportionate to the US$1 million loan principal, and that the sale of these properties could jeopardise Aseana’s majority control in The RuMa Hotel, negatively impacting its financial standing and ability to sell the hotel as a controlling bloc. The legal proceedings also included an application to prevent Wong, Lee and RSMC from enforcing charges over the properties in question, with a temporary undertaking halting any foreclosure proceedings until the injunction application was resolved.

“Poor operating performance has further exacerbated Aseana’s struggles, with the closure of the Sandakan hotel, formerly Four Points by Sheraton Sandakan, in 2020 amid the Covid-19 pandemic. No attempt was made to revive the hotel despite a significantly improved market. Instead, its former directors attempted a distressed sale with an incentive structure for themselves,” says a source.

The company also believes there is significant underperformance of The RuMa Hotel, which is managed by Hong Kong-based Urban Resort Concepts Ltd (URC), a small hotel management group that manages two other hotels in China.

“The RuMa Hotel and Residences has also suffered because of the inability to service mounting debts at very high interest rates over the years, compounded with late payment interest,” the source adds.

In 2019, Aseana secured a medium-term note (MTN) programme not exceeding US$19.07 million to fund The RuMa Hotel and Residences. Some of these MTNs, which were due, are being rolled over every six months.

Transformation long overdue

The transformation at cash-strapped Aseana is long overdue. According to industry sources, the company is considering options to enhance shareholder value, including restructuring its loans to help it ease some of its financial woes, following the injection of equity.

For one, Aseana hopes to refinance a RM60.9 million loan granted by Bank Pembangunan Malaysia Bhd, Malayan Banking Bhd (KL:MAYBANK) and OCBC Bank (Malaysia) Bhd to fund the development of Sandakan Harbour Square.

Aseana’s filings with LSE show that ICSD Ventures had entered into an agreement in June 2023 to sell the Sandakan assets for RM165 million (against a carrying value of RM200 million), the proceeds of which would have been used to repay the outstanding loan. Completion of the transaction was to take place three months later, according to the agreement. However, the deal fell through. As a result, ICSD Ventures was placed in receivership after it defaulted on the final repayment date of Dec 8, 2023. Aseana is working with the lenders to settle the outstanding balance.

“The mall is valuable, clocking an earnings before interest, taxes, depreciation and amortisation (Ebitda) of about RM5 million per year”, according to a source familiar with the matter.

In 1H2024, the occupancy rate at Harbour Mall Sandakan was 93%.

“With a creditable party [like Lim] driving the business, loans can be restructured with significant interest savings. In fact, the banks are finalising the refinancing of the loans,” the source adds.

Industry sources say the group also hopes to reopen the Sandakan hotel and is in talks with three international hotel chains, including Marriott International, to revive its Four Points by Sheraton brand. If successful, it would be the only branded hotel in Sabah’s second-largest town.

“The company is also looking at the possibility of Ormond Group managing the Sandakan hotel under the Four Points by Sheraton brand,” a source says, adding that the company is confident that the Sandakan hotel will be able to achieve Ebitda of RM12 million to RM13 million per year with an international brand.

Aseana also hopes to run The RuMa Hotel better by optimising cost and improving its occupancy and revenue. The hotel recorded a 65% occupancy rate in 1H2024.

“The RuMa Hotel’s management contract with URC ends in 2028. Aseana has been disappointed with the returns of the hotel in the light of significant improvements of the room rates in KL [post-pandemic]. Even though the hotel is highly rated and garners good guest reviews, this is not reflected in the financial returns and the company believes substantial improvements can be made with the hotel’s profitability,” the source says, pointing to RuMa Hotel’s prime location in the KL city centre, which is within walking distance of Pavilion Kuala Lumpur and Suria KLCC.

So far, Aseana has sold 121 units of the 253-room RuMa Hotel. The remaining 132 units account for 60% of the commercial space and give Aseana controlling interest in the hotel.

“That’s why the company filed for an injunction to stop Wong, Lee and RSMC from selling the 30 units in The RuMa Hotel owned by UDSB — to retain control of the asset,” a source explains.

As for RuMa Residences, Aseana has sold 179 of the 199 units.

“Hopefully, once the remaining 20 units are sold, the proceeds will be used to meet its debt obligations and RuMa’s debts will be brought down to a manageable level,” the source adds.

The company is also looking to streamline its portfolio by selling unproductive assets such as a plot of land in Tuaran, industry sources say.

All eyes are now on the restructuring plan for Aseana, which may need to be implemented soon. The company, which has been winding up its assets since May 2015, is required to hold a general meeting for shareholders to vote for or against its discontinuation by end-May this year.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Tan Sri Mohamad Salim appointed as chairman of MACC's Anti-Corruption Advisory Board effective Feb 2 — MACC

- GoTo reiterates no deal in place with any party as it addresses Grab buyout rumours

- Homeland Security slashes personnel in unit leading fight against domestic extremism

- Asian stocks muted, yen softer ahead of BOJ decision

- Shaping future leaders for Malaysia's economic and policy transformation