Jamalludin: There are some long-term contracts, but their tenures are not encouraging. For banks to give out loans for new builds, they want to see at least seven- to 10-year contracts.

This article first appeared in The Edge Malaysia Weekly on March 10, 2025 - March 16, 2025

THE local offshore support vessel (OSV) sector may experience a shortage of vessels in the coming years owing to insufficient new builds and an ageing fleet, says a recent industry report. At the same time, industry players attribute the lack of long-term contracts as a major factor discouraging new builds.

According to the Petronas Activity Outlook 2025-2027 (PAO), the ageing vessels currently servicing production are “a concern” should there be an insufficient number of new builds coming into the market in the next three years. “Based on a supply and demand analysis of OSVs in Malaysia, there will be a critical shortage of anchor handling tug supply (AHTS) vessels below 80 tonnes beyond 2030, unless owners acquire new vessels,” it says.

Malaysia OSV Owners’ Association (Mosva) president Jamalludin Obeng says the lack of long-term contracts in the OSV sector is one of the factors discouraging new builds.

“There are some long-term contracts, but their tenures are not encouraging. For banks to give out loans for new builds, they want to see at least seven- to 10-year contracts,” he tells The Edge.

“At the moment, some long-term contracts exist, such as three-year-plus-three-year agreements, totalling six years. However, since the contract is not fully firm for six years, banks may only recognise it as a three-year term. You know they want security, right?”

Jamalludin says the industry has been in talks with clients for longer contracts as the industry would need at least two to three years to plan for new builds, especially since there are not many yards available to build vessels in the country.

“In Malaysia, only a limited number of proven yards have the capability to handle bigger OSVs, with some yards focusing more on offshore structures or Heavy Topside (HTS) projects. For such specialised work, companies often turn to facilities in Batam, Indonesia, Singapore and China. The situation in Malaysia is that the fleets are ageing, with the average fleet at 13.2 years,” he adds.

“It will take about two to three years to introduce a new fleet, and longer if it includes the planning and financing. It is worth noting that there had been no new build orders for new assets since 2019 until one was announced a few months ago. None of the major players has announced fleet expansion plans.

“Almost all the development and oil and gas (O&G) activities are offshore [but] you need vessels to operate, do maintenance and support offshore development and drilling. The industry is at a crossroads — we recognise the need for new builds, but we lack the financial means to proceed.”

OSV sector to remain robust

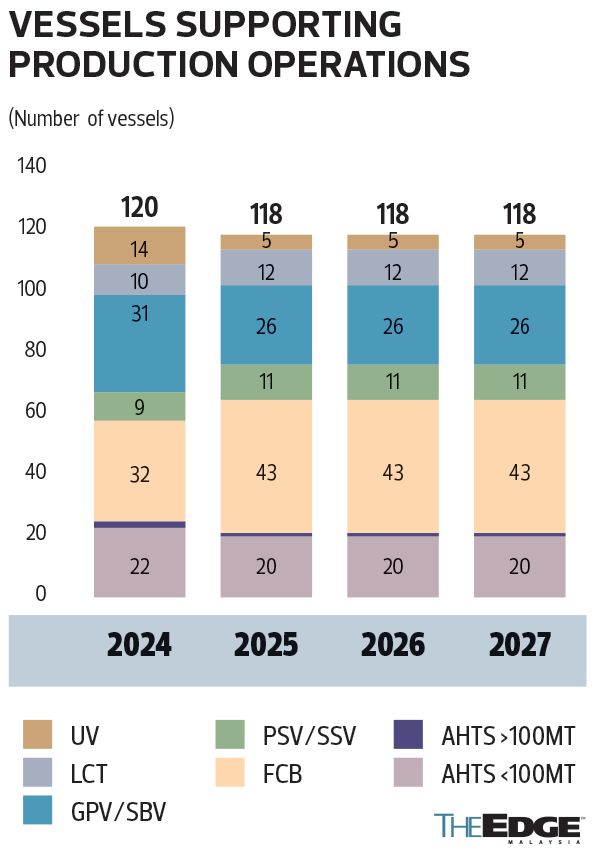

According to the PAO, the O&G sector will require 118 vessels a year to support activities between 2025 and 2027.

Currently, the vessels of Mosva members come to 267, of which 15% are not in operation. Some of the vessels are more than 15 years old.

“The 118 vessels requirement mentioned in the PAO is to support the current production operation. That does not include drilling and maintenance,” says Jamalludin, who expects the situation to remain tight in the coming years given the increasing maintenance activities.

“For the next three years, there is no reason for a slowdown in terms of demand for OSVs, as there are 400 offshore platforms that need to be operated and maintained, as well as OSVs to support the jack-ups and tender-assist drilling rigs (TADR),” he observes, adding that he expects charter rates to remain stable during the period, in line with the global trend in O&G activities.

In a Feb 26 report, Kenanga Research recommended that investors prioritise upstream maintenance-related counters such as OSV players and service providers that focus on hook-up and commissioning (HUC) and maintenance, construction and modification (MCM).

It said Petroliam Nasional Bhd (Petronas) spending was expected to lean heavily towards maintenance. “Upstream activities remain largely intact, with selective year-on-year (y-o-y) growth in HUC and MCM driving another strong year for maintenance players like Dayang Enterprise Holdings Bhd (KL:DAYANG).

“OSV demand may moderate downwards slightly but remains supported by a declining fleet supply. Drilling and EPCC players may see reduced activity in 2025, but a stronger 2026 is possible if Petronas’ plans remain on track.”

Record earnings by OSV players

Over the past month, the local stock market has been in a slump amid a slew of US tariff headlines threatening imports from many countries, including the O&G sector.

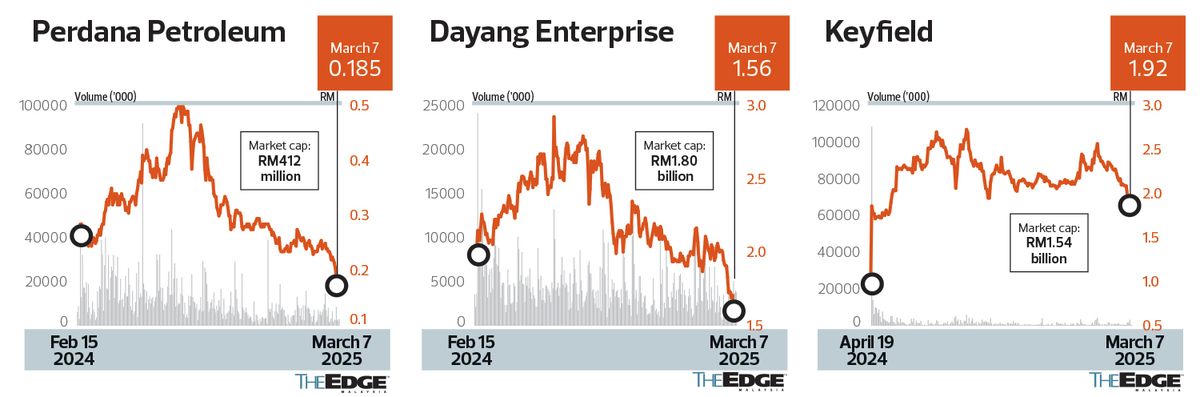

Drilling down into the industry, one of the most badly hit sectors in terms of share price performance has been OSV, despite some companies posting record profits. For instance, Perdana Petroleum Bhd’s (KL:PERDANA) share price has fallen almost 30% y-o-y to 18 sen, giving the company a market capitalisation of RM403.42 million, despite posting its strongest net profit in 18 years in the financial year ended Dec 31, 2024 (FY2024).

On a y-o-y basis, Perdana’s latest earnings improved 228.79% to RM146.03 million from RM44.415 million, owing to a larger number of vessels in operation and higher charter and utilisation rate of 70%, from 58% previously. Revenue rose 40.2% to RM440.12 million from RM313.91 million in FY2023. Back-of-the-envelope calculations indicate that the company’s net profit margin stood at 33.2%.

At the same time, it lowered its debt level to RM16.26 million from RM27.15 million the previous year. Its cash pile rose to RM118.62 million, giving it a net cash position of RM102.36 million.

Perdana’s parent company Dayang also posted a record profit in FY2024, an improvement of 42% to RM311.09 million, from RM218.98 million a year earlier, on the back of a 32% increase in revenue to RM1.47 billion from RM1.11 billion previously. Dayang’s share price has also suffered a battering, down 30% to RM1.57, which values the company at RM1.82 billion. Perdana and Dayang are currently trading at a 12-month trailing historical price-earnings ratio (PER) of 2.82 times and 5.84 times respectively.

Meanwhile, Marine and General Bhd (KL:M&G) recorded an even better first-half performance for its financial year ending April 2025, with its net profit surging 60.3% to RM25.05 million from RM15.63 million a year earlier. Its share price has fared better, having gained 40% y-o-y to 28 sen, which in no small part is due to the recent RM300 million contract it bagged on Feb 14.

Another OSV player Keyfield International Bhd (KL:KEYFIELD) recorded an FY2024 net profit that had more than doubled to RM226.94 million from RM105.48 million in FY2023. Revenue increased 59.6% to RM687.15 million from RM430.45 million in the previous year. Its net profit margin stood at 33%.

However, on a year-to-date basis, Keyfield’s share price has declined 18% to RM1.90, giving the company a market capitalisation of RM1.54 billion. The shares are currently trading at a trailing 12-month PER of 6.7 times, compared with Marine & General’s 3.7 times.

The earnings of Lianson Fleet Group Bhd (KL:LFG) — previously known as Icon Offshore Bhd — surged almost 10 times in FY2024 to RM45.04 million from RM4.86 million a year earlier, driven by higher daily charter rates despite the overall utilisation rate dropping to 69% from 75% in the previous year because of unplanned maintenance activities.

LFG’s share price has gained 61.3% over the past year, but it is likely because of two factors: it has a new shareholder in Yinson Holdings Bhd (KL:YINSON) and a corporate exercise involving RM403.5 million to acquire equity stakes in vessel-operating companies that added 40 more vessels to the group.

Even so, LFG’s share price has been flattish at RM1 since the start of the year. This translates into a market capitalisation of RM620.5 million for the group.

Analysts attribute the negative sentiment on the sector to uncertainties between Petronas and Petroleum Sarawak Bhd (Petros) over a handful of issues, particularly the right to distribute gas in Sarawak.

“We reckon that the continued selldown of local O&G players arising from concerns about the Petronas-Petros saga and geopolitical uncertainties might have been overdone, especially on counters with steady earnings outlook in 2025 such as Dayang,” Hong Leong Investment Bank (HLIB) said in a Feb 26 client note.

HLIB retained its “neutral” stance on the sector, but remained selective in terms of names with a resilient earnings profile and that is less sensitive to Petronas’ upstream capital expenditure programmes. It said even though Petronas had guided for lower exploration and drilling activities in 2025, it expects offshore service contractors (such as MCM-HUC and OSV players) and onshore plant maintenance contractors to continue to enjoy elevated work orders driven by the recently awarded multi-year Pan Malaysia MCM and HUC service contract packages.

“Our checks with OSV players suggest that Malaysian-flagged OSVs remain in severe deficit. This in turn will support the elevated charter rates in 2025, although growth may be marginal or flattish,” it added.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.

- Trump releases JFK assassination documents

- Siemens to cut 8% of jobs at struggling factory automation business

- US stocks hit by tech rout on eve of Federal Reserve decision day

- Asian stocks to track overnight Wall Street decline ahead of Fed decision

- Bangkok Airways seeks 30 new jets as TV series White Lotus boosts tourism

- Malaysia shares dip as investors return from holiday with caution

- Nvidia looks to expand AI reign with new chips, personal supercomputers

- Indonesia’s wild stock moves spark fresh investability concerns

- MORNING CALL: 19/3/25

- Germany's AAA rating could face pressure in longer run without growth boost, Fitch says